Zijin Mining Group (2899.HK): Finding Advantage in Difficult Ground

At the surface level, Zijin exists to resolve a physical supply deficit. Decarbonisation, electric vehicles, solar and wind, transmission grids, and the computing infrastructure behind AI all require more copper at a time when the global mining sector has been starved of new supply.

The One-Liner

Zijin is a mining company at its core. Mining sounds simple because the basic idea is easy to understand. The company digs the earth, extracts minerals, and sells what it produces.

In practice, the easy deposits are gone, and what remains is harder to work with. The ore is often lower grade. The jurisdictions are often less stable. The assets are often in places other companies prefer not to touch.

That difficulty is where Zijin’s earnings come from. Its business model is doing the difficult work that other companies choose not to do. That same business model is also the risk.

Copper first caught my attention because prices were moving.

But I did not want to stop at the surface-level conclusion that higher copper prices made copper miners interesting. There had to be something beneath the surface. The better question was why copper was moving in the first place.

AI infrastructure was part of the answer. Data centres need copper. So do the power plants behind them. So does the grid capacity needed to support them.

But limiting copper to AI and data centres is like limiting water to drinking only. It matters for AI. But AI is not the whole story. The frame is too narrow.

Copper is a basic input for the wider electrical system. Homes need it. Offices need it. EV motors need it. Solar farms need it. Wind turbines need it. So do circuit boards, charging stations, substations, factory motors, lifts, air-conditioning systems, and the cables connecting all of them.

Unless something displaces copper as the default conductor, copper is less an AI story than an infrastructure story. AI is the latest and loudest layer on top of a much older demand base.

That was why I put Zijin aside at first. Before picking a company inside the copper layer, I wanted to understand the wider system. That became my earlier piece on the AI infrastructure stack.

When I came back to copper after that, Zijin was the producer that stood out. Not because it was a clean copper pure-play. It was not.

It also mined gold.

Copper gave Zijin exposure to the physical buildout of electrification. Gold gave it something different: exposure to a monetary asset that tends to matter more when confidence in paper assets, currencies, or financial systems weakens. Copper and gold are not the same bet. One is tied to industrial demand. The other is tied to scarcity, distrust, and long-cycle store-of-value behaviour.

Together, they made Zijin more interesting than a simple copper miner.

What stood out next was the financial profile. Margins had widened across a decade. Returns on capital were moving beyond what I expected from a normal resource extractor. The balance sheet was improving even as output kept growing. This did not look like a simple commodity story.

This is when I stopped asking if copper was going up, and started asking why Zijin earned like this.

This brief takes that idea seriously across three layers: the ore, the jurisdictions, and the capital.

What This Business Actually Is

Zijin Mining Group is a vertically integrated mineral resources company, dual-listed in Shanghai (601899) and Hong Kong (2899), with a market capitalisation of roughly HK$1.01 trillion.1 It explores, mines, processes, smelts, refines, and sells base and precious metals. It is China’s largest gold producer and ranks among the top five copper miners globally.2

The company began in 1986 as a small county-level exploration outfit in Shanghang, Longyan, in Fujian province. Its signature early asset, the Zijinshan copper-gold mine, was considered marginal and uneconomic at inception because of its low grades and complex metallurgy.3 The company survived by learning to extract value from ore that others had written off. That constraint became the operating philosophy, and Shanghang is still where the headquarters and its largest shareholder sit today. Historically the business was a gold company, and gold has not faded into a side business. Gold and copper together generated 77% of revenue in the first half of 2025, and their gross-profit contributions are now close to even: 38.6% from gold and 38.5% from copper, up from a wider gap in 2024.4 Difficult ore was the first ground Zijin learned to work, and the instinct to go where the rock is hard never left.

One structural feature separates Zijin from most Western houses. It owns and operates its own smelting and refining capacity rather than outsourcing it. When third-party treatment and refining charges spike because global smelting capacity is tight, captive smelting protects the consolidated margin instead of leaking it to a processor.5

The geographic footprint is genuinely global. Zijin describes more than 30 large-scale mining operations and projects across 19 countries and five continents.6 The portfolio mixes outright control with minority and attributable interests, and that distinction matters. How much of a mine’s output and cash actually reaches Zijin’s shareholders depends on whether the company owns the asset, controls it, or simply holds a stake in it.

The copper base is anchored by Kamoa-Kakula in the DRC, Julong in Tibet, Čukaru Peki in Serbia, Kolwezi in the DRC, and the original Zijinshan in Fujian.7 The gold portfolio now largely sits under the separately listed Zijin Gold International, with assets across four continents.8 Zinc, lead, and lithium add further optionality, with the lithium ambition centred on the Tres Quebradas brine project in Argentina.9

The business is not a single-mine or single-metal story. It is a global resource-development system, and the ownership mix behind each asset matters as much as the asset itself.

Why This Business Exists

At the surface level, Zijin exists to resolve a physical supply deficit. Decarbonisation, electric vehicles, solar and wind, transmission grids, and the computing infrastructure behind AI all require more copper at a time when the global mining sector has been starved of new supply.10 For industrial manufacturers and smelters, Zijin is a reliable, high-volume supplier of copper in both unrefined (concentrate) and refined (cathode) form. If its largest assets disappeared, well over a million tonnes of annual copper would vanish from global supply.11

That is the commercial purpose. The deeper one is sovereign. China consumes close to half the world’s refined copper and controls only a fraction of the mine supply. By acquiring overseas reserves and bringing them into production quickly, Zijin functions as a direct link between Chinese industrial demand and physical raw material, insulating that demand from potential supply disruption.12

Gold answers a different question, and Zijin exists to answer that one too. At the surface level, Zijin supplies bullion and concentrate at scale. That gold moves into the hands of jewellers, refiners, and private buyers who want the physical, allocated metal itself.Their demand holds steady regardless of where the price sits in its cycle.

The deeper purpose is again sovereign, but the logic runs through reserves rather than industrial inputs. China’s central bank has added to its official gold holdings for eighteen consecutive months through April 2026, part of a broader push by China and other reserve-holding nations to diversify away from US dollar and Treasury exposure following the freezing of Russian central bank assets in 2022.13 Gold cannot be frozen, sanctioned, or seized by a foreign government, which makes it a preferred reserve asset precisely when confidence in dollar-denominated holdings weakens.14 As a large domestic gold producer with a captive supply chain from mine to refined bullion, Zijin sits inside that strategic picture, not as the buyer of reserves, but as a domestic source of the metal a sovereign accumulation programme depends on.

This is the fact that the market reads as a governance risk and that the business reads as the source of its cost-of-capital advantage. Both readings are correct. They are the same fact viewed from two sides. The pattern holds for gold as much as it does for copper: a state-linked resource champion, operating in service of two different forms of resource security at once.

The unit economics that make the model work rest on speed. The mining industry has historically needed ten to fifteen years to move a discovery from greenfield to commercial production. Zijin routinely compresses that to two or three years.15 Time is the largest lever on the present value of a mining asset. A company that develops faster than its peers generates higher returns on the same geology, which is why assets that Western majors leave dormant can become profitable in Zijin’s hands.

How It Succeeds

Zijin’s competitive position is easiest to misread if the risks are listed separately from the advantages. In most mining companies, difficult ore, difficult jurisdictions, and difficult capital structures would be treated as problems to discount. In Zijin’s case, they are closer to the operating model. The company succeeds by doing three things repeatedly: making difficult ore economic, acquiring resources in places others avoid, and funding long-cycle development with capital that is willing to tolerate more uncertainty than Western public markets usually allow.

Layer 1: Technical Capability

Zijin uses hydrometallurgical techniques, including bio-leaching, large-scale heap leaching, and pressure oxidation, to extract metal from ore that standard methods cannot process economically.16 Zijin developed this as an operating template. When it acquires a low-grade copper system or a complex gold asset, the bet is not that the commodity price will rise. The bet is that its engineers can recover more metal and make the same rock worth more in Zijin’s hands than it was in someone else’s. Mining involves two things: the machine and the medium. The machine, the processing technique, is Zijin’s edge. The medium, the rock itself, is the constraint. The technique has to keep working orebody after orebody, and the planned move into lithium brine is a new medium entirely, a different chemistry with a different set of problems.17

Layer 2: Geographical Strategy

The world’s easiest mining jurisdictions are crowded, expensive, and slow. Many of the best undeveloped deposits sit in places where the political, fiscal, or social risk is too uncomfortable for Western majors, who operate under stricter capital-discipline frameworks, heavier ESG scrutiny, and shareholders who often prefer buybacks to frontier development.18 Zijin is positioned differently. It moves into the DRC, Serbia, Colombia, Suriname, Central Asia, and Argentina because the risks that repel others are part of the acquisition discount.19 Operating at this scale also spreads fixed cost across millions of tonnes of processed metal, keeping unit costs low enough to preserve cash flow when prices fall.20 The same logic that makes the entry price cheap is what makes the asset risky: a jurisdiction discounted for tax revision, resource nationalism, or sanctions can reprice at any time, and the discount becomes a loss rather than a return.

Layer 3: Capital Structure

Zijin’s state anchor gives it access to patient financing, strategic alignment, and a lower cost of debt than a purely private frontier miner would receive, which in practice is what funds the first two layers. But the same capital structure is the governance question. If national resource-security objectives ever sit ahead of minority shareholder returns, the advantage becomes the risk. The state relationship lowers the cost of capital, but it also raises the cost of trust.

Together, the three layers explain why Zijin’s moat and its discount come from the same place. Each layer is a source of edge and a point of failure at once. The ore may not yield, the jurisdiction may turn, the capital may stop serving minority shareholders first. None of this is incidental to the business. It is the business.

Takeaway Zijin converts difficulty into economics. It works rock others struggle with, enters jurisdictions others avoid, and funds projects with capital others cannot easily access. That is the source of the return, and the reason the market will not value it like a simpler miner.

The Stewards

Zijin was founded by Chen Jinghe. As of 31 December 2025, Chen transitioned to Lifetime Honorary Chairman. Zou Laichang is now Executive Chairman, and Lin Hongfu serves as Vice Chairman and President.21 Several third-party profiles still describe Chen as Executive Chairman, but that is no longer accurate. Chen retains his personal stake of roughly 68.9 million shares, so the founder stays economically aligned, but operating leadership has passed to a professional management team.22

Chen built the culture that made Zijin unusual: technically aggressive, counter-cyclical, willing to work assets others avoid. The question for Zijin is whether professional stewards preserve that appetite, or drift toward the caution that defines Western majors. Zijin has profited from that same caution for years.

So far, capital allocation still looks aggressive, not reckless. Zijin Mining Group is the parent of the wider group, not a subsidiary of anyone, and it holds majority or controlling stakes in its operating units. The clearest evidence of how the new stewards use that structure is Zijin Gold International, the gold subsidiary carved out and listed separately on the Hong Kong Main Board in September 2025. ZGI holds the group’s gold assets outside mainland China and raised roughly US$3.2 billion in one of the largest IPOs of the year, with cornerstone investors including GIC, BlackRock, and Schroders.23 The transaction unlocked a valuation the parent structure had been suppressing and funded overseas capex and debt reduction. The trade-off is complexity: parent shareholders must now track where the economics sit between the listed parent and the listed subsidiary.

The second move was consolidation. In March 2026, Zijin took a 25.85% controlling stake in Chifeng Gold through a combined RMB18.258 billion transaction, spanning both onshore A-share and offshore H-share placements.24 This is not a miner simply buying more mines. It is a resource company using structure, capital markets, and state-linked credibility to keep consolidating difficult assets.

That brings the ownership question back to the centre. The largest single shareholder is Minxi Xinghang State-owned Assets Investment Operation, which holds 22.88% (with 208,484,145 shares frozen) and is controlled by the Shanghang County government in Fujian, the company’s home base.25 Total issued shares split between onshore A-shares and offshore H-shares, with one-share-one-vote and no dual-class structure.26 A 22.88% stake is not majority control, but in practice it is a powerful blocking position. Major structural change, board direction, and strategic transactions are unlikely to move against state assent.

The implication cuts both ways. The state anchor gives Zijin patient capital, strategic alignment, and a cost of debt that does not fully price the frontier nature of the assets, which funds the ore and jurisdiction layers described earlier. But the same anchor is the minority-shareholder question. If national resource-security objectives ever rank above pure return on capital, the advantage becomes the risk.

The thing to watch with Zijin's management is not whether they are capable. They clearly are. It is whether they keep using the state-backed capital machine to compound per-share value, or whether the same machine eventually serves objectives minority shareholders cannot control.

Where the Moat Is Being Tested

The risks below are not separate from the business model. They are where that model is tested.

The first test is capital discipline. Patient, state-backed capital is only valuable if it still earns an adequate return. If state priorities push investment into low-return smelting or projects that serve resource security more than shareholder economics, the same capital advantage becomes a minority-shareholder risk.27 The 12.6% of votes cast against the 2026 guarantee and debt-financing mandates at the AGM is a small but real signal that some shareholders are watching this balance.28

The second test is jurisdictional durability. Will the countries that make Zijin's deposits cheap let it keep the economics? Exposure to the DRC, Suriname, Colombia, Serbia, and Central Asia carries permanent risk of tax revision, resource nationalism, and operational disruption.29 A frontier asset can look cheap at entry and expensive later, if the host claims more of the economics once the capital is already sunk.

The third test is funding access: Will capital markets keep funding the model? Zijin operates in difficult places partly because capital is available to do so. But that access is not guaranteed to stay open on the same terms. Regulatory and forced-labour-screening risk under the US Uniform Forced Labor Prevention Act (UFLPA), which presumptively bars US imports tied to Xinjiang sourcing, could raise the cost of capital and complicate refinancing of the company's offshore convertible bonds and commercial loans.30 A miner that funds frontier growth with external capital is exposed to more than the mines it owns. It is exposed to the willingness of capital providers to keep underwriting it.

The fourth test is reinvestment intensity. Can cash flow keep carrying growth? Capex ran at roughly RMB 31 billion in FY2025, directed at Julong, Kamoa-Kakula, and the Argentine lithium projects.31 Cash flow covers it comfortably today, but the model only works while operating cash flow keeps scaling. A sustained downturn in copper or gold prices would test whether the reinvestment is discretionary or load-bearing.

The fifth test is lithium. Does the technical edge transfer to a new medium? Zijin is scaling rapidly into brine assets such as Tres Quebradas in Argentina, with lithium carbonate guidance rising from 25.5 kilotonnes in 2025 toward 270 to 320 kilotonnes by 2028.32 Zijin's edge on copper and gold comes from process power (the engineering skill of extracting more metal, more cheaply, from ore ). That edge has not been tested on brine chemistry, a different technical discipline built around extracting lithium from saltwater rather than rock. And lithium prices are weak right now, which makes any transfer harder to prove. This is adjacency risk dressed up as capability extension.

Read together, these are not threats arriving from outside the business. They are the business model under stress, tested in the same places it is created: capital discipline, jurisdiction, funding access, reinvestment, and technical extension.

What the Engine Shows

The financial profile over the past decade is the strongest part of the case, and it shows structural improvement rather than a cyclical lift. If the three difficulties are the thesis, the engine is the evidence that working them has paid.

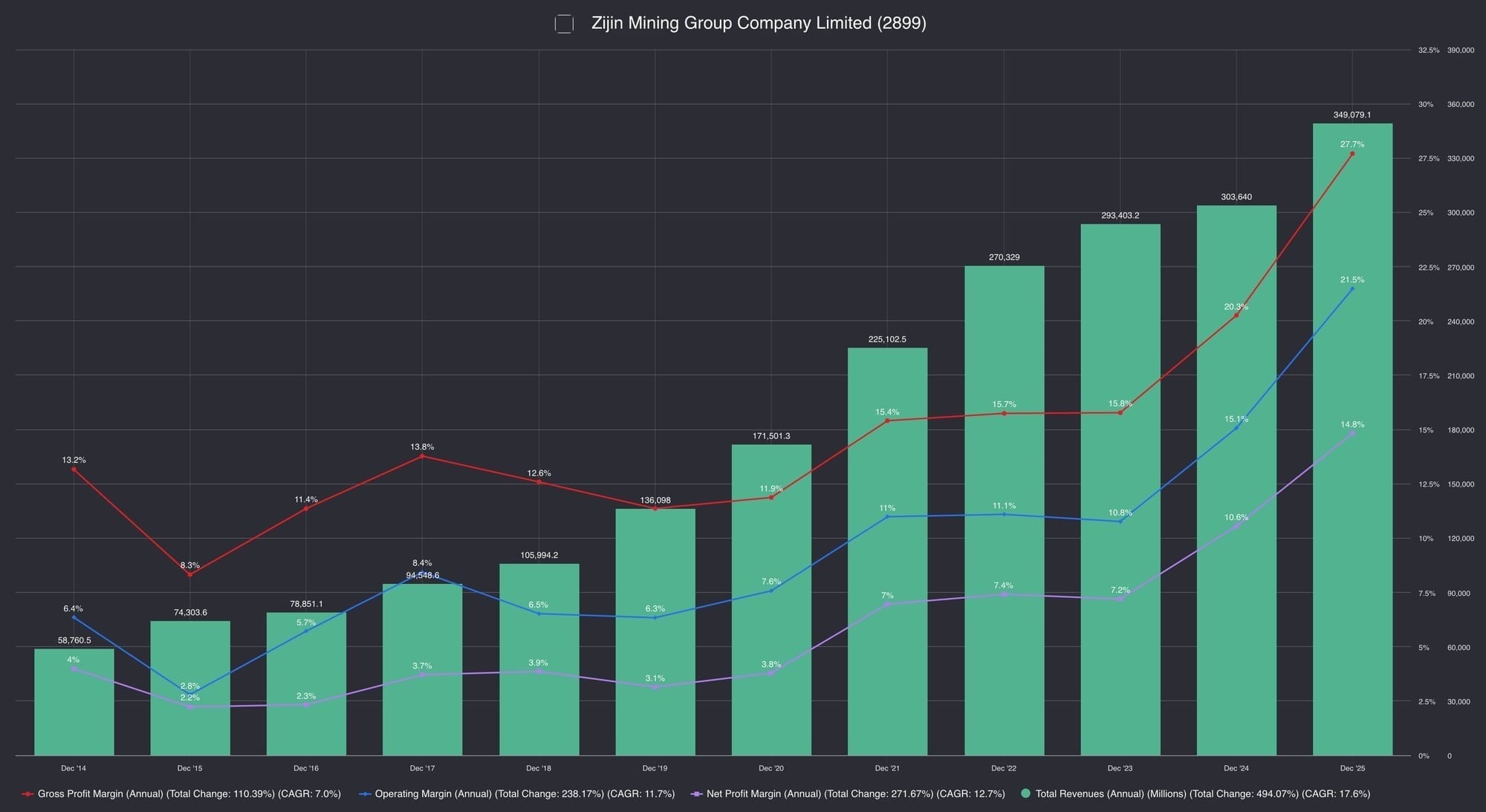

Margins have expanded across the board. Gross margin rose from 11.4% in FY2016 to 27.7% in FY2025, reaching 31.0% on a trailing twelve-month basis. Operating margin climbed from 5.7% to 21.5% over the same period, and to 24.5% trailing. Net margin moved from 2.3% to 14.8%, and to 16.7% trailing.33 This reflects the structural shift toward high-grade mined copper and gold, which together generated 77% of consolidated revenue in H1 2025 and have more than offset cost inflation and grade decline at mature assets.34

Revenue compounded at roughly 18% a year, but the margin lines tell the more important story. Every margin line rose as copper overtook gold as the profit engine. The same revenue base now earns more than twice what it did.

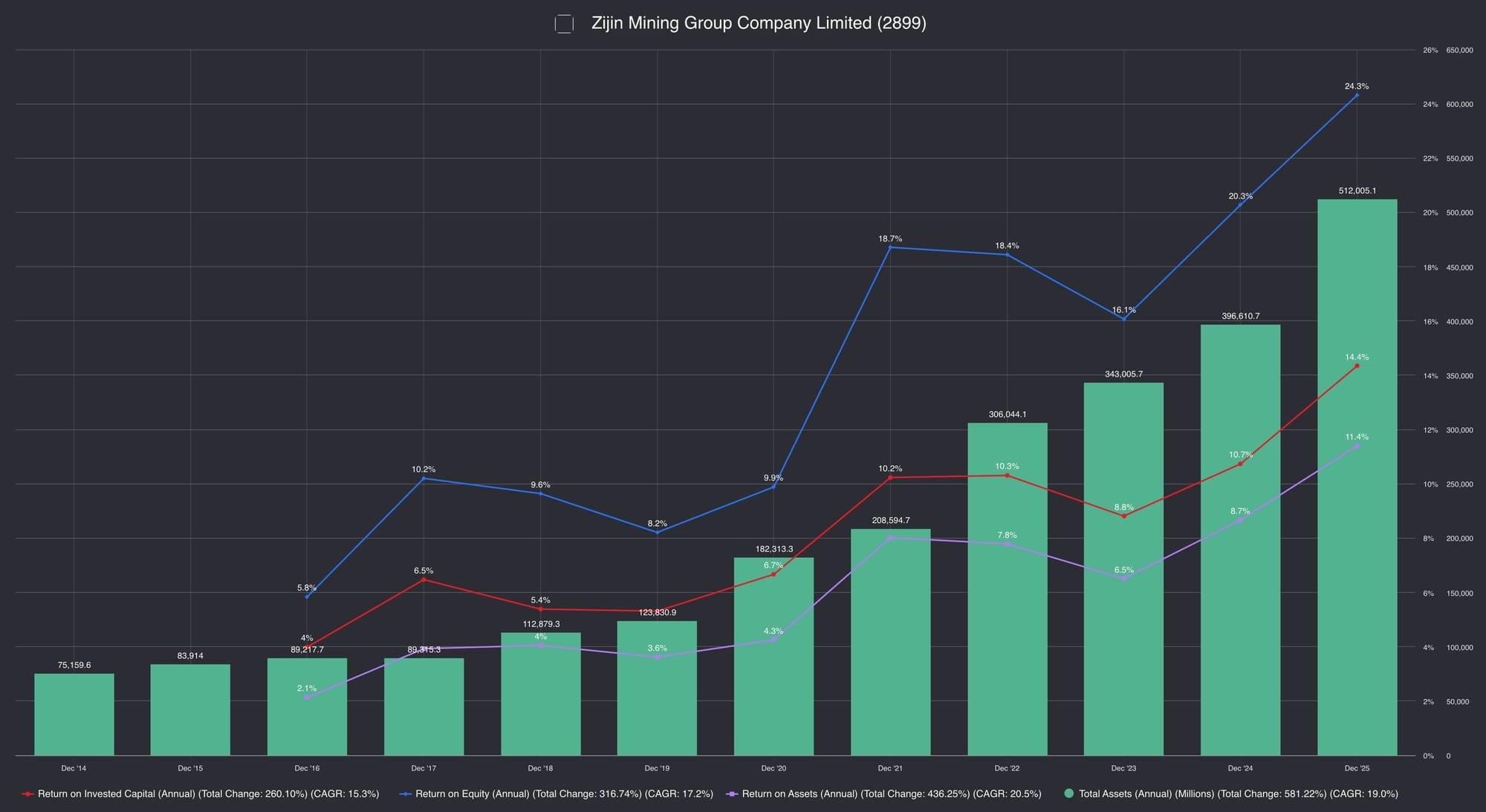

Returns on capital have followed. Return on equity climbed from 9.9% in FY2020 to 24.3% in FY2025, and to 27.5% trailing. Return on invested capital rose from 6.7% to 14.4%, and to 16.5% trailing.35 A ROIC moving through the mid-teens on a capital base this large, in a capital-intensive industry, is the clearest evidence that the M&A strategy is creating economic value above the cost of capital rather than simply buying growth.

Total assets grew more than five-fold over the decade, yet returns on that capital rose rather than diluted. A miner that compounds the asset base and the return on it at the same time is doing something the industry rarely manages.

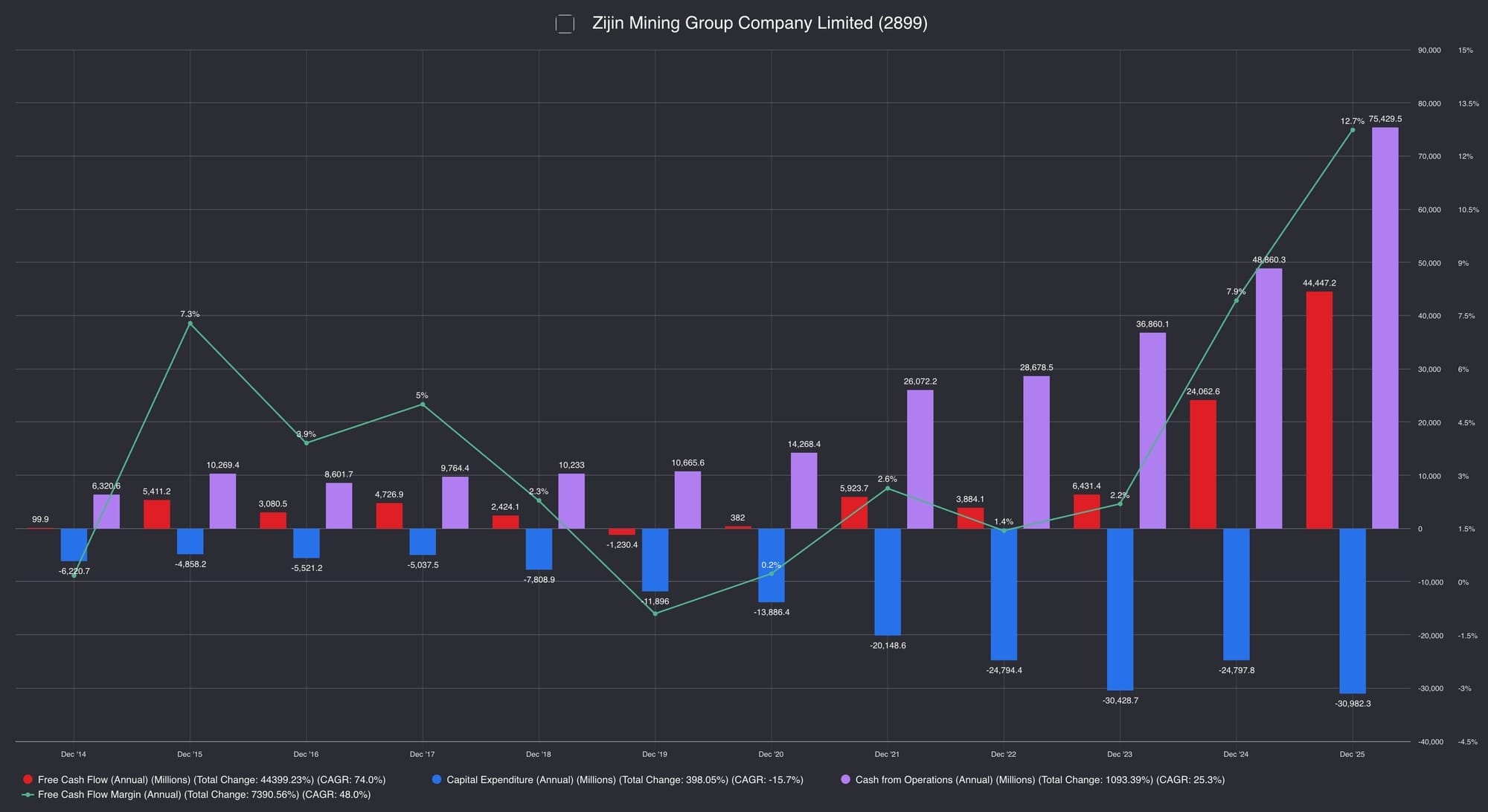

Cash generation has scaled faster than the business. Cash from operations grew from RMB 8.6 billion in FY2016 to RMB 75.4 billion in FY2025, reaching RMB 90.7 billion trailing. Even after capex of around RMB 31 billion, free cash flow surged to RMB 44.4 billion in FY2025 and RMB 59.0 billion trailing, a free cash flow margin of 16% that is genuinely high for an asset-heavy miner.36

Operating cash flow has scaled steeply, and free cash flow turned strongly positive in the last two years. The blue capex bars show why this is also a risk line: the reinvestment runs above RMB 30 billion a year and does not pause. The model works while the orange bars keep outgrowing the blue.

The balance sheet has strengthened through this. The ZGI proceeds and the rising operating cash flow have driven a deleveraging cycle: net debt to EBITDA, around 2.1x in 2024, is tracking below 1.5x, comfortably under management’s internal ceiling of 2.0x.37 Debt-to-equity sits at roughly 0.7x. Interest coverage measured as EBITDA over interest expense climbed from 12.9x at the end of 2024 to 24.5x at the end of 2025, and 29.1x trailing.38 The current ratio improved to 1.14, and 1.30 trailing.

Shareholder returns are present but secondary. The 2025 total dividend was roughly RMB 16.0 billion, including an interim of RMB 5.8 billion and a proposed final of RMB 3.8 per ten shares, for a payout ratio of about 31% and a yield near 1.2%.39 This is a reinvestment-first business. The cash is doing more work in the ground than in shareholders’ pockets, which is consistent with the growth profile but worth naming for any investor expecting income.

The uncomfortable counterpoint is that miners often look most structural near the top of a commodity cycle. The question is whether Zijin's improved returns survive lower copper and gold prices, or whether the operating edge has been amplified by the cycle. Part of that question is separating price from method: how much of this came from higher metal prices, and how much from Zijin's own volume growth, recovery rates, and unit costs.

The engine is excellent on every conventional metric. What the metrics cannot settle is whether Zijin is compounding value per share for minority owners, or simply building a larger resource empire that happens to coincide with a favourable cycle.

What I'll Be Looking At

Zijin in 2026 is a far better business than the discount implies on the surface. Margins, returns, cash generation, and the balance sheet have all moved structurally in the right direction over a decade. The pipeline through 2028 points to more volume in copper, gold, and now lithium. The skill on difficult ore is real and demonstrated.

What the numbers cannot resolve is whether the persistent discount is the market correctly pricing the three difficulties, or misreading the very thing that makes the business work. The difficult ore could stop yielding, or fail to translate to lithium brine. The difficult jurisdictions could turn. The difficult capital could put the state ahead of the minority. Or each could keep doing what it has done for a decade, which is pay.

The First Principles Analysis will critically look into how much of the forward case depends on copper and gold prices, versus Zijin's own volume growth and unit economics. It will go deeper on the questions this Brief has raised: the moat, the stewards, and the engine, working through what the available numbers actually imply, and where the evidence runs out.

The question is not whether Zijin Mining is risky. It clearly is. The better question is whether the risks are external threats to the model, or the very terrain the model was built to navigate.

First Principles Analysis coming this August

Footnotes:

Footnotes (39)

Fiscal.ai, Zijin Mining Group Company Limited Fundamentals, May 2026. Market capitalisation HK$1.01 trillion; dual listing Shanghai Stock Exchange (601899) and Hong Kong Stock Exchange (2899).

Zijin Mining corporate history; analysis of the Zijinshan copper-gold mine origin, drawn from company filings and secondary research, May 2026.

Zijin Mining 2025 interim results: gold and copper combined generated 77% of H1 2025 revenue; gross-profit contribution from mineral gold rose to 38.6% (from 30% in 2024), nearly matching copper's 38.5%. Zijin Mining, "2025 Interim Results," 26 August 2025; MiningComm, "Zijin Mining Reports Record-High Revenue and Net Profit in H1 2025," 10 September 2025.

Analysis of Zijin's vertical integration in smelting and refining versus Western majors that outsource processing; company operating model, 2026.

Zijin Mining corporate profile, recurring company statement across 2025 to 2026 results announcements: "more than 30 large-scale mining operations and projects across 19 countries on 5 continents." Zijin Mining news releases, zijinmining.com/news, March 2026.

Zijin Mining 2025 Results, Major Copper Mines table, zijinmining.com/investor/2025-newyeji.htm. Julong Copper, Xizang (58.16%, grade 0.29%); Kamoa Copper, DR Congo (44.20% attributable, grade 2.48%, joint venture with Ivanhoe Mines); Serbia Zijin Mining (100%); Serbia Zijin Copper (63%); Kolwezi Copper Mine, DR Congo (67%); Zijinshan Copper-Gold Mine, Fujian (100%); Bisha, Eritrea (55%).

Zijin Mining 2025 Results, Major Gold Mines table. Buriticá, Colombia (58.96%); Rosebel, Suriname (80.75%); Norton Gold Fields, Australia (85%); Aurora, Guyana (85%); La Arena, Peru (100%); Zeravshan, Tajikistan (59.50%); Altynken, Kyrgyzstan (51%); Porgera, PNG (20.83%); domestic Chinese gold including Longnan Zijin, Shanxi Zijin, Xinjiang Zijin Gold, and Hunchun Zijin. Akyem (Ghana): 100% interest acquired from Newmont Corporation for US$1 billion, transaction completed 16 April 2025 (Ghana News Agency, 17 April 2025; The Business & Financial Times, 17 April 2025); the 2025 Results mine table lists Zijin's year-end interest at 85%. Raygorodok (Kazakhstan): 100% acquisition closed 10 October 2025 under Zijin Gold International (Zijin Mining news release, 12 October 2025).

Zijin Mining 2025 Results, Major Zinc and Lead Mines table. Zijin Zinc (100%); Urad Rear Banner Zijin, Inner Mongolia (95%); Longxing, Russia (70%); Bisha, Eritrea (55%). Lithium: Tres Quebradas (3Q) brine project, Argentina; Zijin Mining 2025 Results, Production and Guidance.

Global transition-metals supply deficit framing; copper demand from electrification, EVs, grids, and data-centre infrastructure, May 2026.

Combined annual mined copper from Kamoa-Kakula, Julong, and Čukaru Peki exceeds 1.2 million tonnes; Zijin Mining 2025 Results, copper mine tables.

China's share of global refined copper consumption versus mine supply; resource-security rationale, 2026.

China's central bank recorded its eighteenth consecutive monthly increase in official gold holdings through April 2026, reaching 74.64 million troy ounces, as part of a broader reserve-diversification strategy following the freezing of Russian central bank assets in 2022. South China Morning Post, reporting People's Bank of China data, May 2026; World Gold Council, Central Bank Gold Reserves Survey, 2026.

Gold held domestically is not subject to foreign asset-freeze mechanisms, unlike reserves held in foreign institutions or denominated in foreign currencies. Sanctions and geopolitical risk are cited by central banks as key drivers of gold reserve accumulation, with one in four emerging-market central banks specifically citing sanctions concerns. World Gold Council, Central Bank Gold Reserves Survey 2026; European Central Bank, "Gold demand: the role of the official sector and geopolitics," 2025.

Comparison of Zijin's two-to-three-year development cycle against the ten-to-fifteen-year industry norm; company project record, 2026.

Zijinshan hydrometallurgical processing (bio-leaching, heap leaching, pressure oxidation) and its portability as an operating template; company technical history, 2026.

Zijin Mining 2025 Results, Production and Guidance. Lithium carbonate production began in 2025 (25.5 kt) with guidance rising to 120 kt (2026E) and 270 to 320 kt (2028E), via the Tres Quebradas (3Q) brine project, Argentina. Brine extraction chemistry is distinct from the sulphide and oxide ore processing used in Zijin's copper and gold operations.

Western mining majors' capital-discipline frameworks and aversion to frontier sovereign risk; industry structure analysis, 2026.

Counter-positioning durability under New York, London, and Toronto public-market regimes; author's analysis.

Scale economics in base and precious metals; fixed-cost dilution across processed volume.

Governance transition effective 31 December 2025: Chen Jinghe to Lifetime Honorary Chairman; Zou Laichang to Executive Chairman; Lin Hongfu as Vice Chairman and President. Zijin Mining board disclosures. Chen Jinghe retained holding approximately 68.9 million shares per Fiscal.ai Insider Ownership, Q1 2026.

Zijin Mining Group Co., Ltd., Resolutions Passed at the 2025 Annual General Meeting, HKEX, 5 June 2026; board composition disclosed therein and in the Final Dividend announcement dated 15 May 2026.

Zijin Gold International (ZGI) carve-out and Hong Kong Main Board listing, September 2025; approximately US$3.2 billion raised, shares +68% on debut, cornerstone investors including GIC, BlackRock, and Schroders. Secondary market reporting, 2025 to 2026.

Chifeng Gold transaction, executed 22 March 2026 through two agreements: RMB10.006 billion for the domestic A-share block (241,925,746 shares) and HK$9.386 billion (RMB8.252 billion) for the H-share placement (310,902,731 shares), for total consideration of approximately RMB18.258 billion, resulting in a 25.85% controlling stake (571,661,877 shares) in Chifeng Gold. Funded under separate corporate treasury mandates. Jinkai Investment's US$1.5 billion zero-coupon guaranteed convertible bonds due 2031, also outstanding, were earmarked for the La Arena copper-gold project in Peru, working capital, and general corporate purposes. Also outstanding: US$2.0 billion 1.0% guaranteed convertible bonds due 2029 (Gold Pole Capital Company Limited). HKEX announcements, 2026.

Minxi Xinghang State-owned Assets Investment Operation Co., Ltd. holds 22.88% (6,083,517,704 shares), of which 208,484,145 shares are frozen, controlled by the Shanghang County government, Fujian. Zijin Mining Group Co., Ltd., First Quarterly Report 2026, 21 April 2026.

Zijin Mining Resolutions Passed at the 2025 AGM, HKEX, 5 June 2026: total issued shares 26,590,714,622, comprising 20,601,793,140 A Shares (including 77,474,592 treasury shares) and 5,988,921,482 H Shares; A-shares 77.48%, H-shares 22.52%.

Sovereign-commercial conflict and minority-return subordination risk; author's analysis of state-anchored ownership.

Zijin Mining Resolutions Passed at the 2025 AGM, HKEX, 5 June 2026. Resolution 8 (guarantee plan for 2026) passed with 12.68% against; Resolution 10 (debt financing instruments mandate) passed with 12.63% against.

Geopolitical and resource-nationalism exposure across the DRC, Suriname, Colombia, Serbia, and Central Asia: tax revision, permitting conflict, and operational disruption risk. Secondary research, 2026.

Regulatory and forced-labour-screening risk under the US Uniform Forced Labor Prevention Act (UFLPA), and its potential effect on cost of capital and refinancing of offshore convertible bonds and commercial loans. Secondary research, 2026.

Zijin Mining cash flow data, Fiscal.ai. Capital expenditure approximately RMB 30.98 billion (FY2025) and RMB 31.71 billion trailing, directed to Julong, Kamoa-Kakula, and Argentine lithium projects.

Zijin Mining 2025 Results, Production and Guidance. Lithium carbonate 25.5 kt (2025), guidance 120 kt (2026E), 270 to 320 kt (2028E). Tres Quebradas (3Q) brine project, Argentina.

Fiscal.ai, Margin charts, Zijin Mining (601899). Gross margin 11.4% (Dec 2016) to 27.7% (Dec 2025), 31.0% LTM; operating margin 5.7% to 21.5%, 24.5% LTM; net margin 2.3% to 14.8%, 16.7% LTM.

Zijin Mining 2025 interim results: gold and copper combined generated 77% of H1 2025 revenue; gross-profit contribution from mineral gold rose to 38.6% (from 30% in 2024), nearly matching copper's 38.5%. Zijin Mining, "2025 Interim Results," 26 August 2025; MiningComm, "Zijin Mining Reports Record-High Revenue and Net Profit in H1 2025," 10 September 2025.

Net debt to EBITDA approximately 2.1x (2024), tracking below 1.5x (2025 to 2026), against an internal ceiling of 2.0x; deleveraging supported by ZGI proceeds. Company and ratings commentary, 2025 to 2026.

Zijin Mining 2025 Results, Dividend History; Final Dividend announcement, HKEX, 15 May 2026. 2025 cash dividends approximately RMB 16.0 billion, payout ratio approximately 31%; interim RMB 5.8 billion (H1 2025); proposed final RMB 3.8 per 10 shares. Dividend yield approximately 1.2% per Fiscal.ai.

Disclosure: Glavcot Insights and its contributors may hold positions in securities discussed in this article. All content is provided for informational and educational purposes only. Nothing published by Glavcot Insights constitutes investment advice. Readers should conduct their own research and consult qualified financial professionals before making investment decisions.

Glavcot Insights is an independent equity research publication founded by Ryan Gallinera and managed under Glavcot LLP, Singapore.

Where Clarity Meets Conviction

Glavcot Insights is now live. Join the free tier to get new research, updates, and future analysis directly in your inbox. (Check your spam folder if you don't see the confirmation email)

You might also like

Jun 05

Pan-United Corporation Ltd (P52.SI): Concrete Is the Business. The System Around It Might Be the Moat.

There is also a durability argument that I keep returning to. Concrete has not fundamentally changed in a hundred years. You can make it greener, stronger, lighter, smarter to deliver. But the thing itself, a material that hardens into infrastructure, is not going away.

17 min read

May 19

Haidilao (6862.HK): Is Service the Moat, or the Cost?

Haidilao's service quality did not emerge from a training manual. It was built through a specific mechanism: a master-apprentice incentive structure where store managers are compensated not just on their own store's performance, but on the performance of managers they trained

13 min read

Apr 07

Singapore Exchange Limited (S68.SI): The Exchange Is the Infrastructure

The One-Liner

Singapore Exchange does not compete for market share. It is the market. And it collects a toll

15 min read

Mar 16

Centurion Accommodation REIT (8C8U.SI): The Architecture of Essentiality

The One-Liner

Centurion is a leading specialized accommodation provider that builds and operates mission-critical human infrastructure. It provides

8 min read

Feb 28

NetEase (9999.HK): First Principles Analysis

If you're coming from the First Principles Brief, you already know what NetEase does and why the business