Pan-United Corporation Ltd (P52.SI): Concrete Is the Business. The System Around It Might Be the Moat.

There is also a durability argument that I keep returning to. Concrete has not fundamentally changed in a hundred years. You can make it greener, stronger, lighter, smarter to deliver. But the thing itself, a material that hardens into infrastructure, is not going away.

The One-Liner

Pan-United is Singapore's largest ready-mix concrete supplier. The more interesting question is whether it has quietly built something harder to replicate than concrete itself.

I came across Pan-United while working through the AI infrastructure theme. The underlying question I had was which businesses sit underneath the AI buildout rather than inside it. The obvious answer is semiconductors, power, cooling. The less obvious answer is what goes into the ground first.

Every data centre, every hyperscale facility, every server hall starts with a foundation. Concrete foundations. In Singapore, a city-state currently approving hundreds of megawatts of new AI-ready data centre capacity and simultaneously running the largest infrastructure pipeline in its history (Changi T5, Tuas Port, Cross Island Line, North-South Corridor) the demand for concrete is not a question. The question is who supplies it, and whether that position is defensible.

I have not independently verified whether Pan-United is a direct supplier to Singapore's data centre construction pipeline. That sits on my list for the First Principles Analysis. But it almost does not matter for the initial framing. The point is simpler: Singapore will need concrete for the next twenty years. The question is whether Pan-United's position in that pipeline is structural or just large.

There is also a durability argument that I keep returning to. Concrete has not fundamentally changed in a hundred years. You can make it greener, stronger, lighter, smarter to deliver. But the thing itself, a material that hardens into infrastructure, is not going away. The ten-year question for most technology businesses is whether they still exist. For a concrete company with Singapore's infrastructure pipeline, the ten-year question is simply whether they still have the contracts. That is a different and in some ways more comfortable risk profile to underwrite.

That is what brought me here. The business, as it turns out, is more interesting than the entry point suggested.

Brief Introduction

Concrete is not supposed to be a good business.

The material is heavy, perishable, and time-sensitive. It cannot be stockpiled. A truckload that arrives late can become waste. The raw materials (cement, aggregates, water) are commodities. Labour is expensive. Fuel is volatile. The end customer, the construction sector, is notoriously cyclical. Margins, historically, have been thin.

Pan-United's roots trace to 1958, when founder Ng Kar Cheong borrowed S$3,000 to seed a shipchandling business in Singapore.1 The company pivoted into construction materials as the city-state industrialised, eventually listing on the SGX Mainboard in December 1993.2 For much of its history, the business looked like the industry it served: adequate returns, cyclical revenues, no particular reason to pay attention.

The recent numbers break that pattern.

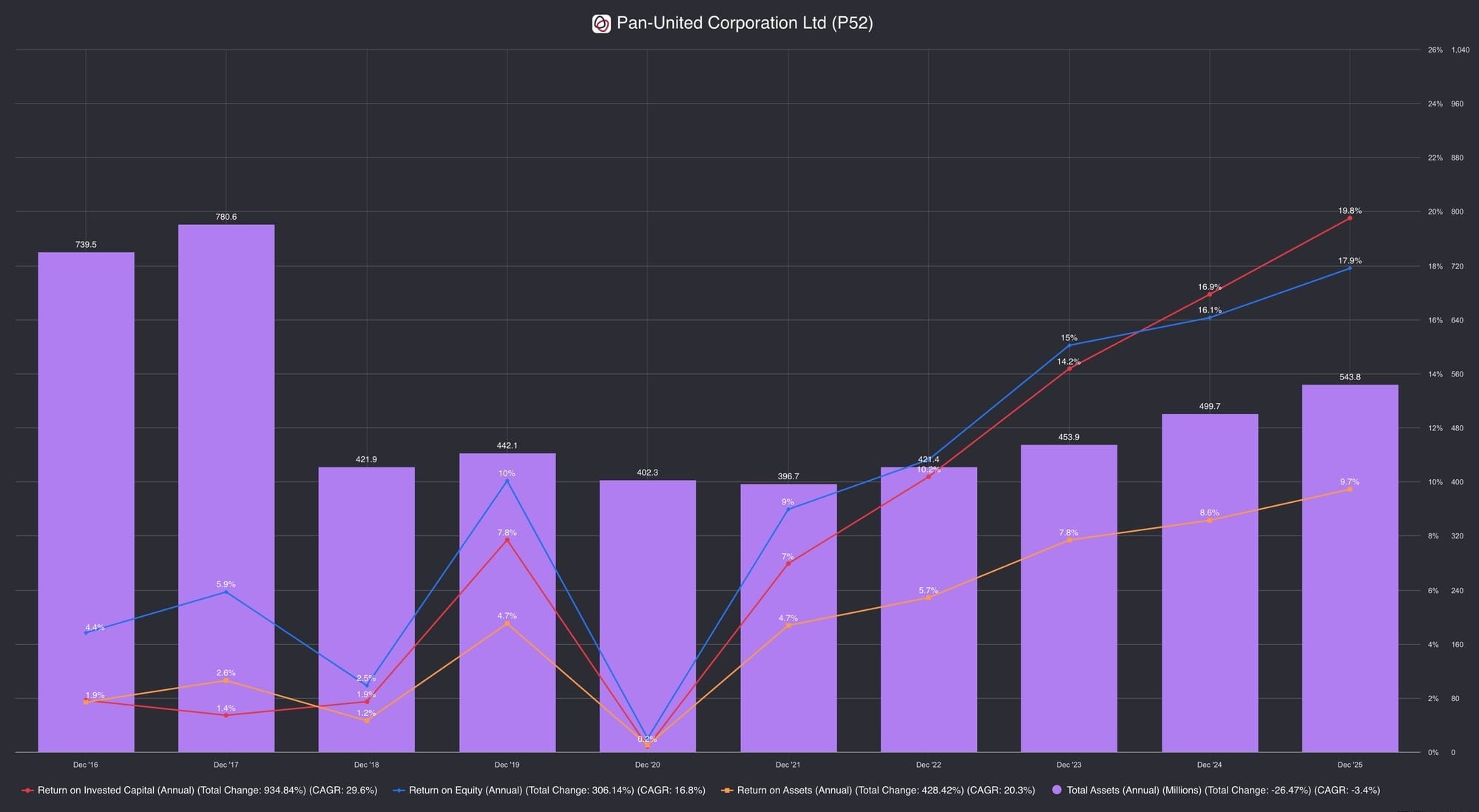

In FY2025, Pan-United reported revenue of S$898.4 million, EBITDA of S$99.1 million, and PATMI of S$50.7 million.3 Revenue grew 11% year-on-year, EBITDA rose 32%, and PATMI climbed 24%.4 Return on shareholders' funds reached 18.3% on an average-equity basis.5 The balance sheet carries no net debt. EBITDA/Interest coverage stands at approximately 26.8x.6 The five-year share price return from June 2021 to June 2026 is approximately 373%.7

The question this brief tries to answer is simple. Is the improvement real and structural? Or is Pan-United a good concrete company in a good construction market, with numbers that will revert when the cycle turns?

What This Business Actually Is

Pan-United Corporation Ltd (SGX: P52) is, by revenue, almost entirely a concrete and cement business. In FY2025, the Concrete & Cement segment contributed S$889.8 million of S$898.4 million in group revenue, approximately 99%.8 The Trading & Others segment, which includes petroleum products and general trading, is operationally secondary and analytically less important for the thesis.

The core operation is ready-mix concrete supply. Pan-United operates batching plants across Singapore, produces concrete to order, and delivers it by transit mixer truck to construction sites across the island. It also manufactures and trades cement, operates cement silos, and produces ground granulated blast furnace slag (GGBS) at a slag grinding plant in Malaysia operated through associate Meridian Maplestar Sdn Bhd.9

This vertical integration matters. GGBS is a steel production by-product used as a supplementary cementitious material in place of Ordinary Portland Cement. It is one of the primary inputs in Pan-United's low-carbon concrete products. Controlling GGBS production provides direct influence over the cost and composition of the most differentiated part of the portfolio.

Pan-United also operates ready-mix concrete businesses in Malaysia (Fortis Star) and Vietnam (FiCO Pan-United). Both have introduced carbon mineralised concrete technology in their respective markets, each as the first ready-mix company in its country to do so.10 These operations remain small relative to Singapore but serve as the deployment platforms for Pan-United's technology expansion beyond the island.

The business is not primarily defined by geography. It is defined by its relationship with Singapore's built environment: the island's infrastructure programme, public housing pipeline, commercial development cycle, and increasingly, its carbon transition mandate.

Why This Business Exists

Ready-mix concrete is a local market by physical necessity. Concrete begins setting within approximately 90 to 120 minutes of batching.11 Every plant can only serve sites within a viable delivery radius. Market share does not travel. It must be built, plant by plant, in specific locations.

Pan-United is Singapore's largest provider of ready-mix concrete.12 That position is the product of decades of capital investment in plant capacity, geographic coverage, and operational reliability. In a market where the physical footprint is the franchise, scale and delivery reliability create structural advantages that smaller competitors cannot easily overcome regardless of price.

Singapore's construction demand provides the underlying support. Construction contracts awarded in Singapore for 2025 were estimated at S$50.5 billion by the Building and Construction Authority. The BCA expects demand in 2026 to be maintained at between S$47 billion and S$53 billion.13 Beyond 2026, the BCA projects average annual construction demand of between S$39 billion and S$46 billion from 2027 to 2030, underpinned by long-term projects including Changi Airport Terminal 5, MRT line extensions, the Tuas Port development, the North-South Corridor, the Cross Island Line, and public housing.14

For major public infrastructure, public housing, and large private-sector developments, supply certainty matters more than marginal price differences. Pan-United, as the scale player with a broad plant network and long project track record, benefits disproportionately from this dynamic.

Scale and demand visibility explain why Pan-United is large. They do not explain why it is profitable. That gap is what the next section is about.

How It Succeeds

The System Around Concrete

Pan-United's strategic self-description has evolved considerably over the past decade. The company no longer calls itself a ready-mix concrete supplier. It describes itself as a global leader in low-carbon concrete technologies, transforming into a technology company with concrete as its core business.15 The honest question is whether that repositioning reflects substance or aspiration.

By “system,” I mean the combination of physical plant network, low-carbon formulation capability, digital dispatch and quality control, and verified carbon documentation that makes Pan-United more than a generic concrete supplier.

The evidence suggests more substance than a casual reading would imply. Three things stand out.

Carbon mineralisation and PanU CMC+

Pan-United was the first company in Asia to adopt carbon mineralisation technology in 2018, using a licensed process (commercialised globally by Canadian firm CarbonCure Technologies) that captures industrial CO2 and permanently embeds it into concrete during batching.16 Pan-United's application of this technology, branded PanU CMC+, uses less cement, achieves higher compressive strength, and carries a measurably lower embodied carbon footprint than standard ready-mix. The underlying IP belongs to CarbonCure; the advantage Pan-United has built is in deploying it at greater scale, earlier, and with deeper product integration than any other Asian operator. Notable projects supplied with PanU CMC+ include the Tuas Port development, the North-South Corridor, the Cross Island Line, Shaw Tower (the first new commercial building targeting BCA Green Mark Platinum Super Low Energy certification under 2021 criteria), The Skywaters at 8 Shenton Way, and a range of public housing developments.17

This matters for two reasons. First, Singapore's regulatory direction is toward mandatory embodied carbon disclosure and green building standards. Pan-United's low-carbon capability, delivered at scale, is becoming a qualification requirement for major public and private contracts, not a premium option. Second, low-carbon solutions now account for over 60% of Pan-United's concrete portfolio, with more than 50% of Singapore sales volume already carrying a low-carbon designation.18 This is no longer a niche.

The operational technology layer

Pan-United has invested over a decade in two proprietary AI-driven systems, with technology investments and process re-engineering traced back to 2014.19

AiR Digital, operated through the subsidiary AiR Digital Solutions Pte Ltd, is an end-to-end operations management platform handling demand forecasting, truck assignment, material replenishment, digital ordering, and delivery coordination. It powers Pan-United's Command Centre and has been commercialised externally, with over 20 customers now across Southeast Asia, North Asia, and Australasia.20 AiR Digital debuted its AI-enabled solutions in the United States at the World of Concrete trade show in January 2026.21 The Skywaters project required a continuous raft foundation pour: Pan-United delivered one truckload of concrete every two minutes for 35 consecutive hours. The 10,250 cubic metre pour was also the first in Singapore to use Grade 105 Super High-Strength Concrete. 22

AiM is a real-time in-transit concrete management system, the first completed project under the BCA's BETA Catalyst initiative, that integrates batching plant operations with mixer trucks, monitors slump quality during transit, and reduces on-site quality check requirements and material wastage. As of FY2025, AiM is deployed across 100% of eligible mixer trucks.23

Environmental Product Declarations at scale

Pan-United is the first concrete company in Asia to provide on-demand EPDs for every product in its portfolio.24 An EPD is a third-party-verified embodied carbon disclosure across a product's full lifecycle. For developers and contractors working toward green building certifications or whole-life carbon targets, the ability to specify Pan-United concrete and receive a verified EPD at the design stage is a material procurement advantage. It creates customer stickiness without requiring a contract clause to enforce. It is embedded in the design workflow itself.

The cumulative picture is of a business that has used a physically captive market position as the foundation for layering in capabilities that are genuinely harder to replicate: a licensed but deeply integrated low-carbon concrete technology platform, an AI-driven operations stack built over a decade, and a sustainability transparency infrastructure aligned with the direction of regulatory travel.

Pan-United may not have a moat in concrete. It may have a moat in the system around concrete.

What the Engine Shows

The financial profile over the past decade shows a business in structural improvement, not just cyclical lift.

Gross profit margin expanded from approximately 16.7% in FY2016 to 23.8% in FY2025.25 Operating margin followed: from roughly 2.2% in FY2016 to 7.7% in FY2025.26 Return on invested capital moved from approximately 1.9% in FY2016 to 19.8% in FY2025.27 The same revenue base now generates substantially more earnings and substantially better returns on capital.

Cash generation has kept pace. Operating cash flow was S$80 million in FY2025.28 Free cash flow has remained consistently positive over the period. Debt-to-equity stands at approximately 0.2x and interest coverage at 26.8x.29 The FY2025 total dividend was 4.5 Singapore cents per share, comprising an interim of 1.0 cent paid in September 2025 and a proposed final of 3.5 cents, compared to 3.0 cents total in FY2024.30

Revenue growth is more modest. The 10-year CAGR is approximately 4.3%, with a severe pandemic trough in FY2020 (S$406.2 million, down from S$769.5 million in FY2019) when construction sites across Singapore closed.31 FY2025 revenue of S$898.4 million has now surpassed the pre-pandemic peak. The key difference is not the revenue level. It is what Pan-United earns on that revenue.

That combination of stable top-line growth with structurally higher margin conversion is the financial signature of a business that has genuinely improved its operating model, not simply benefited from external conditions.

The Stewards

Pan-United has been controlled by the Ng family since its founding. The family's combined stake through Han Whatt Ng, Bee Kiok Ng, and Bee Bee Ng is approximately 64% of shares outstanding.32

The long-horizon ownership is visible in the business decisions. The R&D investment in PanU CMC+, the decade-long development of AiR Digital, and the sustained reinvestment in plant and logistics capability are not decisions a short-cycle management team makes. Founding-generation equity creates genuine alignment between the business's long-term health and the controlling shareholders' financial interests.

May Ng Bee Bee serves as Executive Chairman, having been CEO from 2011 to 2024 before transitioning to the Chair role. Ken Loh Kah Soon, elevated from Chief Operating Officer, is now CEO.33 The COO-to-CEO succession within the same operating team signals continuity. The test is whether this structure supports the pace required to extend the technology platform and international operations.

The public float of approximately 25% is a legitimate risk consideration for prospective investors.34 Lower liquidity can amplify price volatility in either direction. Minority shareholders have limited practical influence over governance at a company with a 64% concentrated family stake.

Where the Moat Is Being Tested

Pan-United's core risk is not a collapse in concrete demand. Singapore's multi-decade infrastructure pipeline provides a relatively visible demand floor.

The risk that matters most is cyclical durability: can the business sustain its current margins and returns through a construction slowdown?

The history is instructive. In FY2020, revenue fell 47% from the prior year and gross margin compressed to approximately 13%.35 Operating leverage in a high-fixed-cost concrete business works in both directions. The same plant network, truck fleet, and workforce that generates strong returns in an active market becomes a cost drag when utilisation falls.

Underneath the technology narrative sit the fundamental risks of the core business. Margins compress when volume falls and fixed costs do not, when cement or fuel prices spike faster than contracts allow pass-through, when labour costs rise on policy changes, or when a competitor decides to buy market share on price. Pan-United does not control any of these variables. The improved returns of the past five years reflect a period when most of them moved favourably at once. The question is not whether management is capable. It is whether the business model is resilient enough when two or three of those variables move adversely at the same time.

The low-carbon question adds a further layer of complexity. Low-carbon concrete is not yet a mandatory requirement in Singapore. It is an incentive-driven advantage today, rewarded through BCA Green Mark certification tiers and progressively tighter embodied carbon specifications on major public contracts. The regulatory trajectory points clearly toward eventual mandatory thresholds. But the sharper question is not whether Pan-United can supply low-carbon concrete. It clearly can. The question is whether that capability commands a durable price premium, or whether it becomes the new industry baseline that every competitor eventually matches, leaving Pan-United with the capability but not the margin.

Finally, the technology narrative carries its own risk. Pan-United is not a software company. AiR Digital is operated through a subsidiary, AiR Digital Solutions Pte Ltd, and its external revenue is not disclosed as a separate reported line.36 The financial contribution of the technology platform to group returns has not been independently demonstrated in the published numbers. The technology narrative is credible, but its returns contribution has not yet been made explicit.

What I'll Be Looking At

Pan-United in 2026 is a materially better business than it was in 2016. The margins are higher, the returns are higher, the balance sheet is stronger, and the product and technology capabilities are genuinely differentiated. The demand environment is supportive for the medium term.

The question the numbers cannot resolve is whether the improvement is structural or whether the current margin profile reflects a peak that a quieter construction cycle will reveal.

The Ng family's long-horizon ownership, the physical scale of Singapore's largest concrete platform, the first-mover position in carbon mineralisation technology, the AI-driven operations stack, and the alignment with Singapore's green building regulatory direction collectively argue for something more than a commodity business in a good cycle.

But the test has not yet arrived. Pan-United has not yet navigated a meaningful demand downturn with its current technology platform fully deployed. The structural case is compelling as a hypothesis. It has not yet been proven as a fact.

Singapore may also be the special case. The island's regulatory density, sustainability mandates, land constraints, and concentration of high-value infrastructure projects create unusually favourable conditions for Pan-United's model. Vietnam and Malaysia offer growth but may not replicate the same economics. Whether the operating system travels, or whether Singapore is the whole advantage, is a question the international platform has not yet answered.

Pan-United has built a system around concrete, not just a concrete business, and that system may be structurally more defensible and more valuable than the commodity label suggests. But the evidence is not yet conclusive.

The durable pricing advantage could erode if margins normalise as low-carbon concrete becomes the industry standard, suggesting the green capability is a compliance floor that every competitor will eventually match and not a premium Pan-United alone can hold.

The scale advantage could prove fragile if a well-capitalised competitor licenses the same carbon mineralisation technology, builds competing plant capacity, and competes on price.

The technology story could stay just that if AiR Digital's external business remains too small to influence group economics, paying a valuation premium for a narrative rather than a second earnings engine.

And the growth story could hit a ceiling if regional expansion fails to replicate Singapore economics, suggesting the whole advantage is island-specific and structurally capped.

What this brief establishes is that Pan-United has earned the right to be taken seriously. The moat question is genuinely open. The structural improvement is real.

Did Pan-United build a system that outlasts the cycle that revealed it? Or is the margin expansion simply what a good concrete company looks like in a long upcycle?

First Principles Analysis coming this July

Footnotes:

Footnotes (36)

Pan-United Corporation Ltd, History, panunited.com.sg/about-us/history/. The foundation traces to a shipchandling business seeded in 1958. The company’s history spans “nearly 70 years.”

Pan-United Corporation Ltd, Annual Report 2025, Corporate Governance Report, p. 26: listed on the Mainboard of SGX-ST on 22 December 1993.

Pan-United Corporation Ltd, Annual Report 2025, Group Financial Summary, p. 2. Revenue S$898,436 thousand; EBITDA S$99,056 thousand; PATMI S$50,714 thousand.

Pan-United Corporation Ltd, Annual Report 2025, Group Financial Summary, p. 2. Revenue +11% YoY; EBITDA +32% YoY; PATMI +24% YoY.

Pan-United Corporation Ltd, Annual Report 2025, Group Financial Summary, p. 2. Return on shareholders’ funds 18.3% (FY2025), calculated on average basis.

Fiscal.ai, Pan-United Corporation Ltd (P52) Price Chart. 5-year return to June 2026: +373%, CAGR approximately 36.4%.

Pan-United Corporation Ltd, Annual Report 2025, Segmental Information, p. 3. Concrete & Cement revenue S$889.81 million of total S$898.44 million.

Pan-United Corporation Ltd, Annual Report 2025, Corporate Structure, p. 8. Fortis Star Sdn Bhd (100% owned) and Meridian Maplestar Sdn Bhd (100% owned, held via Fortis Star) are the Malaysian entities.

The 90 to 120 minute setting window is standard industry practice for ready-mix concrete logistics; cited in industry technical guidelines as the basis for the local delivery model. Pan-United’s AiM system is specifically designed to manage slump quality within this constraint. See Pan-United Sustainability Report 2024, Sustainable Products, p. 13.

Pan-United Corporation Ltd, Sustainability Report 2025, About Us, p. 2: “Singapore’s largest provider of ready-mix concrete.”

Pan-United Corporation Ltd, Annual Report 2025, Performance Review, p. 14. Construction contracts awarded in Singapore for 2025 estimated at S$50.5 billion; BCA expects 2026 demand of S$47–53 billion.

Pan-United Corporation Ltd, Annual Report 2025, Performance Review, p. 15. BCA projects 2027–2030 average construction demand of S$39–46 billion per year.

Pan-United Corporation Ltd, Annual Report 2025, cover and Executive Chairman’s Message, p. 4: “our mission to transform into a technology company.”

Pan-United Corporation Ltd, Sustainability Report 2024, Key Milestones, p. 7: “1st in Asia to adopt CO₂ mineralisation technology” in 2018.

Pan-United Corporation Ltd, Annual Report 2025, Executive Chairman’s Message, p. 5. Shaw Tower described as targeting BCA Green Mark Platinum Super Low Energy certification under 2021 criteria. Pan-United Sustainability Report 2024, GHG Emissions, p. 20 for project list.

Pan-United Corporation Ltd, Sustainability Report 2025, Sustainable Products, p. 15: “over 300 specialised concrete solutions, over 60% of which are low-carbon in content.” Sustainability Report 2024, Executive Chairman’s Message, p. 3: “more than 50% of our total sales volume” in Singapore is low-carbon.

Pan-United Corporation Ltd, Annual Report 2025, Executive Chairman’s Message, p. 6: “Our continuing investments in technology coupled with process re-engineering since 2014.”

Pan-United Corporation Ltd, Annual Report 2025, Executive Chairman’s Message, p. 6: “AiR Digital has, to date, secured over 20 like-minded customers in the ready-mix concrete and logistics space across Southeast Asia, North Asia and Australasia.” Corporate Structure, p. 9: AiR Digital Solutions Pte Ltd is a 100% owned subsidiary.

Pan-United Corporation Ltd, Annual Report 2025, Performance Review, p. 17: “AiR Digital debuted its AI-enabled solutions in the US in January 2026, during the World of Concrete trade show in Las Vegas.”

Pan-United Corporation Ltd, History, panunited.com.sg/about-us/history/: “Pan-United completes a 10,250m³ mass concrete pour for the 5-metre-thick raft foundation of The Skywaters at 8 Shenton Way. The 35-hour operation delivered a truckload of concrete every two minutes and marks the first project in the country to use Grade 105 Super High-Strength Concrete.”

Pan-United Corporation Ltd, Sustainability Report 2025, Sustainable Products, p. 15: “we achieved our target of full deployment of AiM across our eligible concrete mixer trucks.” Sustainability Report 2024, p. 13: AiM is “the first completed project under the Building and Construction Authority (BCA)’s BETA Catalyst initiative.”

Pan-United Corporation Ltd, Sustainability Report 2025, Sustainable Products, p. 16: “We are the first concrete company in Asia to provide on-demand EPDs across all our specialised concrete products.”

Fiscal.ai, Debt/Equity (Annual): 0.2x; EBITDA/Interest expense: 26.8x, December 2025.

Pan-United Corporation Ltd, Annual Report 2025, Executive Chairman’s Message, p. 5. Total FY2025 cash dividend 4.5 Singapore cents per share (interim 1.0 cent paid September 2025; proposed final 3.5 cents subject to AGM approval), compared to 3.0 cents in FY2024.

Fiscal.ai, Insider Ownership table, March 2026. Han Whatt Ng 23.13%, Bee Kiok Ng 20.47%, Bee Bee Ng 20.41%. Combined approximately 64%.

Pan-United Corporation Ltd, Annual Report 2025, Board of Directors, p. 10. May Ng Bee Bee: Executive Chairman since July 2024, previously CEO from March 2011. Ken Loh Kah Soon: CEO. Pan-United Sustainability Report 2024, Executive Chairman’s Message, p. 4: “Mr Ken Loh has stepped up from his Chief Operating Officer position to become our Chief Executive Officer.”

Public float approximately 25.08% as of 16 March 2026. Calculated as residual of insider ownership disclosed in Fiscal.ai, March 2026.

Fiscal.ai, Total Revenues (Annual): FY2019 S$769.5 million, FY2020 S$406.2 million, decline of approximately 47%. Fiscal.ai, Gross Profit Margin (Annual): FY2020 approximately 13.2%.

Pan-United Corporation Ltd, Annual Report 2025, Corporate Structure, p. 9. AiR Digital Solutions Pte Ltd is reported within the broader group; its revenue is not disclosed as a separate segment line in current financial reporting.

Disclosure: Glavcot Insights and its contributors may hold positions in securities discussed in this article. All content is provided for informational and educational purposes only. Nothing published by Glavcot Insights constitutes investment advice. Readers should conduct their own research and consult qualified financial professionals before making investment decisions.

Glavcot Insights is an independent equity research publication founded by Ryan Gallinera and managed under Glavcot LLP, Singapore.

Where Clarity Meets Conviction

Glavcot Insights is now live. Join the free tier to get new research, updates, and future analysis directly in your inbox. (Check your spam folder if you don't see the confirmation email)

You might also like

Jul 01

Pan-United Corporation Ltd. (P52.SI): First Principles Analysis

If you're coming from the First Principles Brief, you already know what Pan-United does and why the

31 min read

Jun 21

Zijin Mining Group (2899.HK): Finding Advantage in Difficult Ground

At the surface level, Zijin exists to resolve a physical supply deficit. Decarbonisation, electric vehicles, solar and wind, transmission grids, and the computing infrastructure behind AI all require more copper at a time when the global mining sector has been starved of new supply.

22 min read

Jun 16

Pan-United Corporation Ltd.: Snapshot

The Snapshot distills the full First Principles Analysis into a single reference page — the central question the analysis is built

7 min read

May 19

Haidilao (6862.HK): Is Service the Moat, or the Cost?

Haidilao's service quality did not emerge from a training manual. It was built through a specific mechanism: a master-apprentice incentive structure where store managers are compensated not just on their own store's performance, but on the performance of managers they trained

13 min read

Apr 07

Singapore Exchange Limited (S68.SI): The Exchange Is the Infrastructure

The One-Liner

Singapore Exchange does not compete for market share. It is the market. And it collects a toll