Haidilao (6862.HK): Is Service the Moat, or the Cost?

Haidilao's service quality did not emerge from a training manual. It was built through a specific mechanism: a master-apprentice incentive structure where store managers are compensated not just on their own store's performance, but on the performance of managers they trained

A traditional face-changing performance in one of Haidilao's hotpot restaurants.

The One-Liner

Haidilao built a restaurant operating system around one idea: that service, delivered consistently at scale, creates its own economics. The question is whether that system still compounds when expansion slows.

A note before this brief

Everyone is looking at AI right now. The questions are real and the stakes are significant. But one discipline of good research is knowing when to look away from the crowded field.

My instinct when narrowing down candidates is not just to find good metrics. Good metrics are the baseline, not the edge. The question is where genuine analytical gaps exist: businesses that are visible, covered, even well-known, but where the right question is not being asked clearly.

That led me to the food sector. Restaurants are everywhere. The stocks are listed. But the analytical attention is elsewhere.

The specific trigger was unexpected. I was watching a documentary on Singapore's Good Class Bungalows and one name appeared that I recognised: Zhang Yong, founder of Haidilao, now a naturalised Singaporean citizen.1 He purchased a S$27 million bungalow on Gallop Road in 2016, known as The Winged House.2 A man who started with a handful of hotpot tables in Sichuan and built one of China's largest restaurant chains. That story, and the business behind it, deserved a closer look.

This is that look.

I have dined at Haidilao a few times. What stayed with me was not the hotpot itself. It was the surrounding architecture of the experience. While waiting for a table, I noticed people queuing for a complimentary manicure. Free snacks arrived without asking. There was a designated play area for children, staffed and stocked with toys, so parents could actually sit and wait without managing restless kids.3 Inside, everything felt considered: the setting, the presentation of the food, the attentiveness of the staff. At some point during the meal, someone performed a noodle dance at the table. Staff smiled consistently and moved through the space as though the entire room was their personal responsibility.

All of that, though, was before COVID.

I do not know what the experience is like now. What I do know is that the queue at VivoCity on weekends suggests the brand still pulls. Whether the service that built that queue is still what it was is a different question entirely.

Haidilao is not under-covered. The common read is a recovery thesis: table turnover improving, franchise optionality building, China consumer sentiment normalising. That framing may be correct. But it is not the right first question. The right first question is what kind of business Haidilao actually is, and whether the thing that made it famous still creates the economics.

What This Business Actually Is

Zhang Yong founded Haidilao in 1994 from a four-table store in Sichuan.4 The concept was not differentiated hotpot. It was not cheaper hotpot. It was the same hotpot, served better, every time, at every table. That discipline of execution, not product, became the brand.

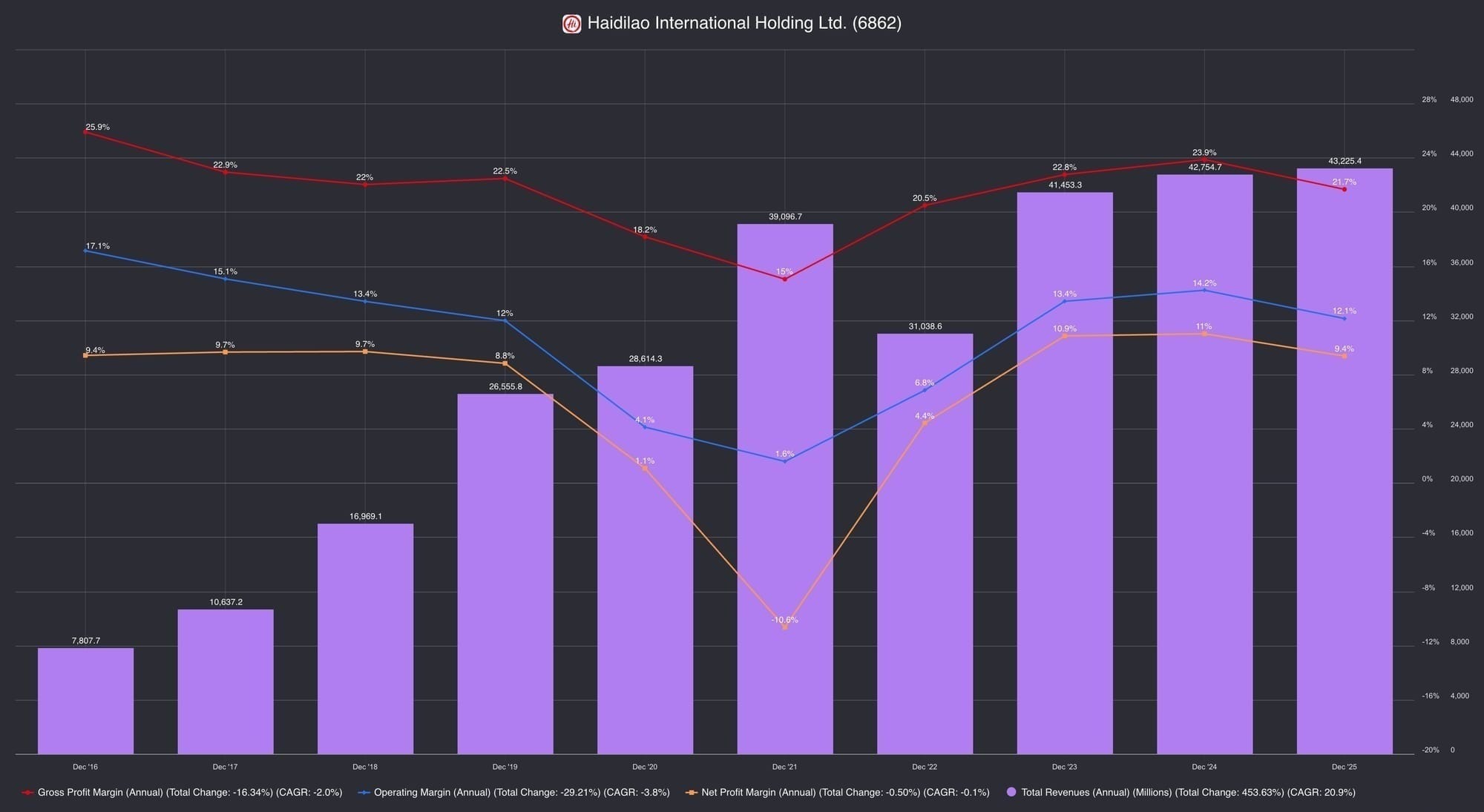

Thirty years later, Haidilao operates 1,304 company-owned and 79 franchised restaurants across Greater China.5 Group revenue exceeded RMB 43 billion in FY2025. It remains one of China’s largest and most recognisable hotpot chains, with over 200 million registered members and an average guest spend of RMB 97.7, at the expensive end of the casual dining spectrum, in an environment where Chinese consumers have been aggressively trading down.6

Revenue in FY2025 broke into three streams: core dine-in at RMB 39 billion, delivery at RMB 2.66 billion (up 112% year-on-year), and a portfolio of twenty sub-brands under the Red Pomegranate Plan at RMB 1.52 billion. 8 Total group revenue grew 1.1%. Look at what drove that.

In early 2024, management opened the brand to selective franchising for the first time in its thirty-year history. By end of FY2025, 79 franchise locations were operating.5 The question that framing raises but does not answer: is franchising a genuine second-growth mechanism, or a capital-light acknowledgment that the self-operated model has reached its ceiling? That is the next layer of work.

Gross, operating, and net margins have compressed steadily since 2016. Revenue has grown. The economics of delivering that growth have not kept pace.

Why the Business Exists

Casual dining in China has historically been one of the most fragmented and operationally unstable sectors in the economy. Before standardised national chains, dining out was plagued by three chronic consumer problems: inconsistent food safety, unpredictable quality across locations, and transactional, indifferent service.

Haidilao exists because it solved all three at scale. The supply chain does the first two. Yihai International handles soup bases and seasonings. Shuhai manages cold-chain logistics and centralised prep. Both entities are connected to Zhang Yong's network. Together, they give Haidilao more supply chain control than most restaurant operators at any scale can replicate.7 Ingredients arrive to spec, every time, at every location. The customer never wonders whether the broth is safe.

The format solves a structural problem most restaurant chains cannot. Hotpot requires no skilled back-of-house chef: the customer cooks the food at the table. This removes the single largest source of quality inconsistency in the restaurant category. The kitchen is a prep and supply function, not a production one. One fewer variable, held constant, across 1,300 locations.

The third problem: indifferent service, is what Haidilao made its identity. Not by training staff harder than competitors, but by building a system that made attentiveness financially rewarding at the store level. The business exists because it turned service from a hospitality value into an operating mechanism. That is unusual. And it explains why customers who have eaten there once tend to come back.

How It Succeeds

Haidilao's service quality did not emerge from a training manual. It was built through a specific mechanism: a master-apprentice incentive structure where store managers are compensated not just on their own store's performance, but on the performance of managers they trained and mentored into opening their own stores.9 The royalty flows down the lineage. A great manager is financially rewarded every time someone they mentored succeeds.

This is an unusual design. It creates ownership-level accountability at the store floor, not just at the corporate level. It explains how service standards propagated across hundreds of locations without a bureaucratic enforcement layer. The culture spread because people were directly paid for spreading it correctly.

But this mechanism has a condition. It requires expansion. New stores, new apprentices, new royalty events. In a growing network, the incentive structure fires continuously. In a mature or contracting one, the lineage stops extending. What remains is culture. Culture without the incentive engine that produced it becomes something different. Maintenance, not compounding.

The FY2025 network tells that story. Self-operated store count fell from 1,355 to 1,304.10 Total table turnover dropped from 4.1x per day in FY2024 to 3.9x in FY2025. Revenue from self-operated Haidilao brand locations fell 7.1%, from RMB 40.4 billion to RMB 37.5 billion. Total restaurant operations including sub-brands and franchises declined 4.5%. The gap between the two numbers tells you where the core pressure sits.11

Then there is this: management attributed H1 2025's underperformance directly to "subpar customer service, which negatively affected repeat visits."12

That is the mechanism confirming itself in reverse. When service quality slipped, traffic fell. The service culture created the economics. When it weakened, the economics followed.

Both things are now visible simultaneously: service quality drives the business, and service quality is under pressure. The question is not whether this relationship is real. It is whether it can be maintained without the conditions that produced it.

Staff costs ran at 32.6% of revenue in FY2025. Raw materials and consumables at 40.5%.13 Those two lines absorb roughly 73% of revenue before rent, utilities, or anything else. That is the price of the service model, stated plainly. And when delivery growth saved headline revenue in the second half, it came at the cost of core operating profit: the mix shift toward lower-margin formats compressed the margins the business has been trying to defend.14

The moat is not absent. It is expensive.

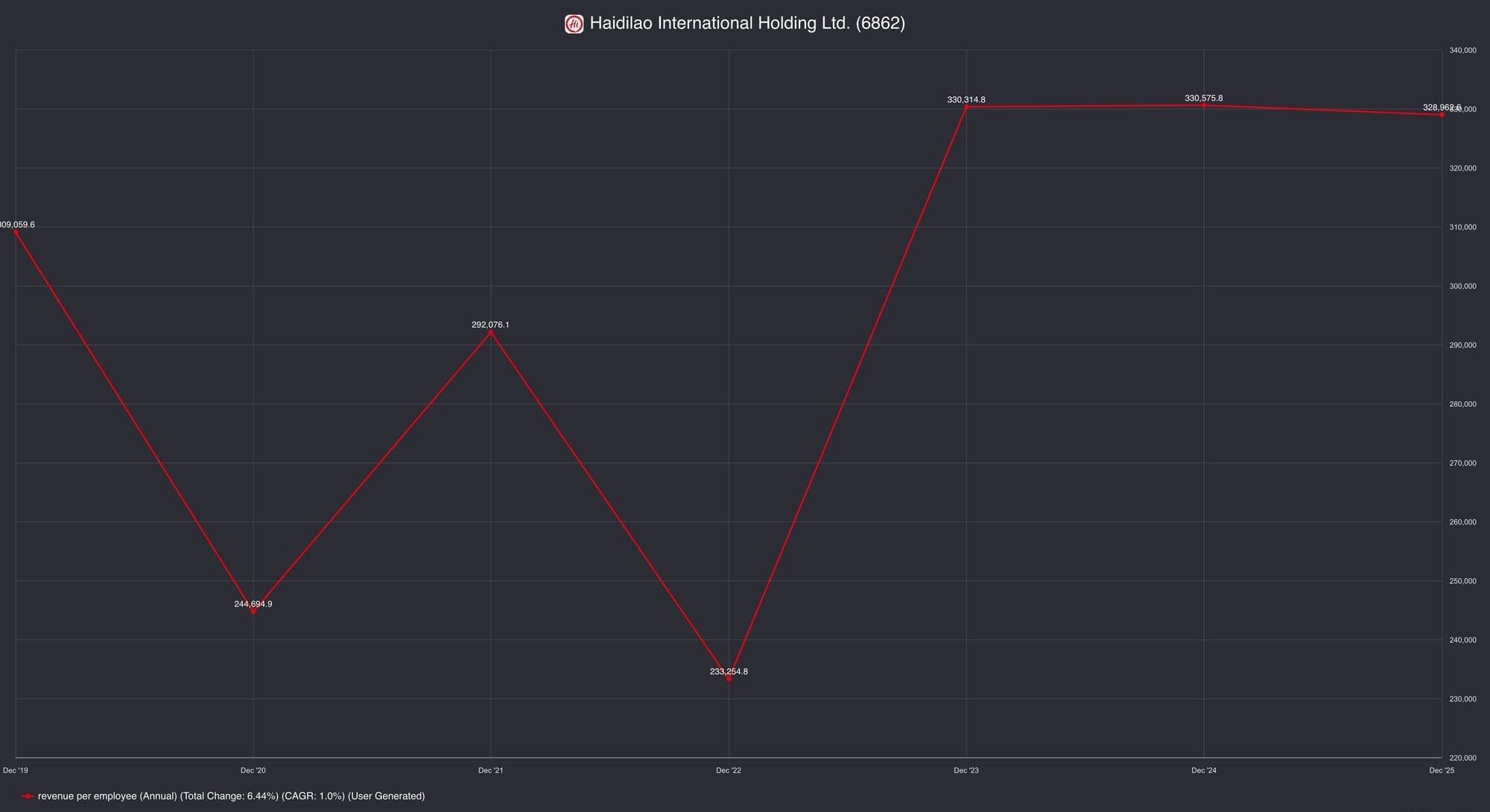

Six years of revenue growth. Output per employee has stayed flat. The service model scales in headcount, not in productivity.

Takeaway The engine was built for expansion. Expansion has slowed. The service is perhaps slipping, while the next phase of growth has yet to arrive. Haidilao's identity is now under pressure.

The Stewards

Zhang Yong stepped back as CEO in 2022, handing the role to Yang Lijuan (known as June Yang), the executive who steered the post-pandemic restructuring. In mid-2024, Yang Lijuan transitioned to lead Super Hi International and Gou Yiqun, a first-generation manager with a financial and supply chain background, assumed the CEO role at Haidilao.15 By January 2026, Gou Yiqun had resigned and Zhang Yong returned to the front lines as CEO, taking on both Chairman and CEO roles concurrently to address operational pressures. That is three CEOs in four years. The operating culture was built across three decades of founder-led expansion. Whether it holds through this level of leadership turnover is an open question.

Founder insiders control 68.63% of the issued shares.16 Alignment with business outcomes is about as direct as it gets in a listed company. In April 2026, the company announced plans to buy back at least HK$100 million in shares. A directional signal, though not a large one relative to market cap.

One structural fact requires clear-eyed acknowledgment: the Haidilao trademark is not owned by the listed entity. It is licensed from Sichuan Haidilao, a private company owned by Zhang Yong personally. The current agreement is perpetual and royalty-free.17 That arrangement has held. Whether it always will remains an open question.

And a single data point worth sitting with. Yang Lijuan now leads Haidilao's Pomegranate Plan alongside Zhang Yong, having returned from Super Hi in April 2026. Super Hi itself now operates 126 restaurants across 14 countries under new CEO Li Yu, a veteran with over 18 years of experience across Asia. Revenue grew 8% year-on-year to US$840.8 million in FY2025. The business turned profitable, reporting net income of US$36.3 million. ROIC reached positive 9.18%.18

The brand travels. Whether the operating system travels with it is still being answered.

Where the Moat Is Being Tested

Chain restaurants account for roughly 20% of total restaurant spending in China, compared to approximately 60% in the United States — a structural gap that represents a long runway for well-capitalised operators.19 But the operating environment is unforgiving in the near term. In Singapore alone, over 3,000 food and beverage establishments closed in 2024, the highest figure in nearly two decades, with an average of 307 closures per month recorded in 2025.20 Rent hikes of 20% to 49% were reported by tenants, and even Michelin-starred restaurants were not spared.

The pressure is not unique to Singapore, but it illustrates the structural reality facing any restaurant operator without genuine pricing power or scale: the cost base moves faster than the revenue line. Haidilao's scale and supply chain give it structural protection most operators lack. But scale is not immunity. The question is whether the brand premium survives a prolonged period of consumer caution.

Haidilao's competitive threat is not primarily from another hotpot chain. It is from the social dining occasion itself being contested.

Korean BBQ has expanded aggressively across Asia and beyond, driven by the global spread of Korean culture and a growing appetite for communal, interactive dining.21 The format competes for the same occasion: a slow, communal, table-side dining experience where the process is part of the pleasure. Themed concepts, omakase counters, and fast-casual formats are further fragmenting the market for the group dining occasion that hotpot once commanded with less competition.

Haidilao's response has been to diversify into sub-brands and delivery rather than defend the core format. Whether that is adaptation or retreat is a question the numbers are beginning to answer.

In short: Haidilao's competition isn't other hotpot chains. It's everything else people could do for the same meal occasion, in a market where the cost of operating is rising faster than what customers are willing to spend.

What the Engine Shows

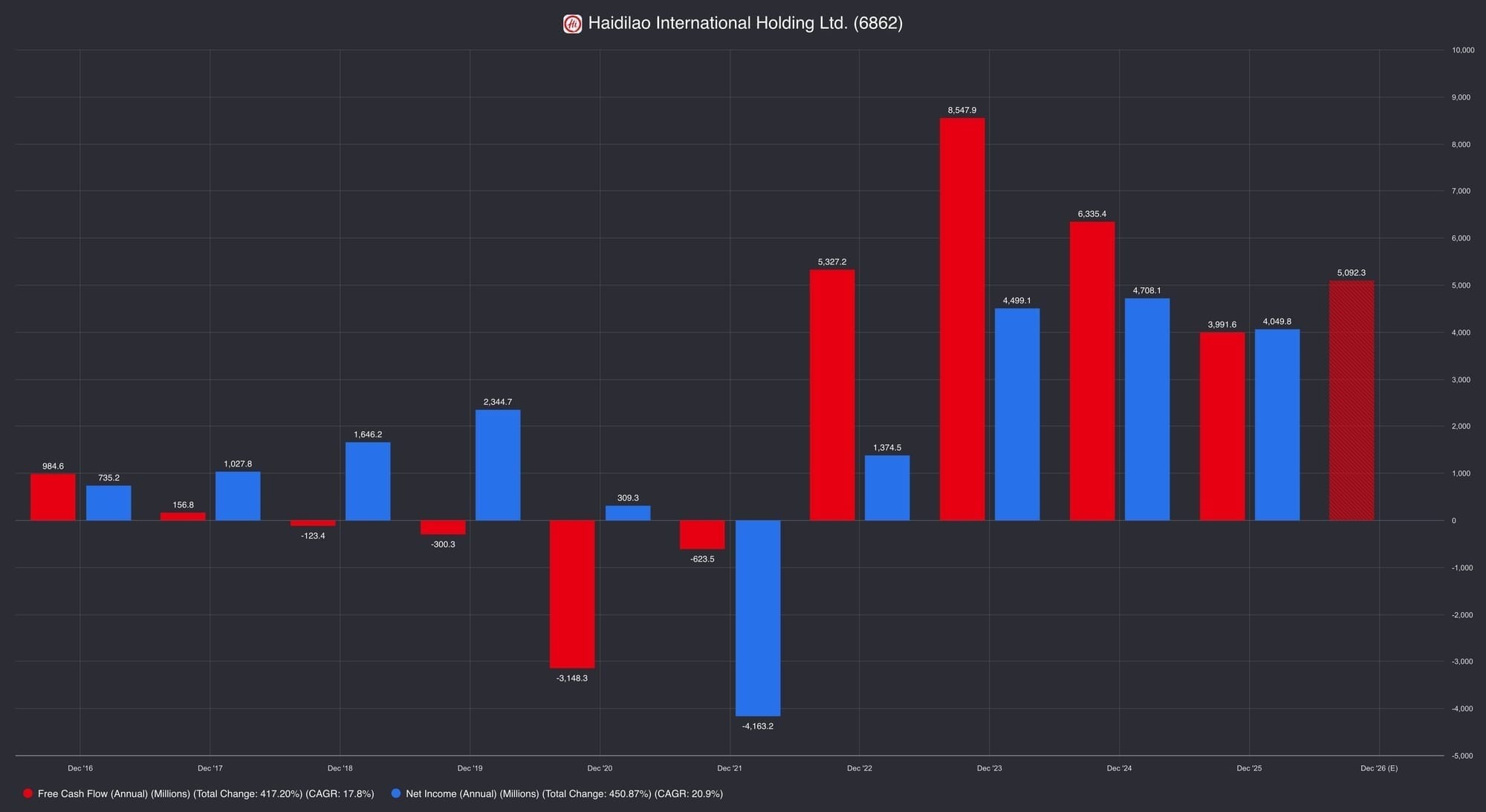

Revenue recovered from the pandemic trough. Free cash flow is real. The balance sheet carries more cash than debt. On those terms, the business looks resilient.

But the recovery is not clean.

Core restaurant revenue fell 7.1% in FY2025 while total group revenue grew 1.1%. The gap was filled by delivery, which more than doubled, and by twenty nascent sub-brands still in early development. Delivery growth in the second half came at the cost of core operating profit: the mix shift toward lower-margin formats compressed the margins the business has been defending.14 Gross margin fell from 23.9% in FY2024 to 21.7% in FY2025.

Operating cash flow is real and has recovered strongly. Free cash flow tells a more nuanced story — capital expenditure is rising again as the business reinvests. Watch the gap.

The headline number suggests stability. The composition of that number raises the harder question: whether the growth replacing the core is accretive to owner economics, or simply volume filling a gap.

One more number worth noting. Haidilao paid out between 87% and 95% of earnings as dividends in FY2024 and FY2025.15 For a business that also claims to be in an expansion phase, that payout ratio is striking. It is either a sign of confidence in cash generation or a sign that management sees limited reinvestment opportunity in the core. That is the unresolved capital allocation question.

What I'll Be Looking At

Haidilao industrialised something no restaurant chain at this scale had reliably done before: attentiveness. The ability to make a customer feel individually seen, consistently, across thousands of daily interactions.

That is not replicable by copying the menu. It required a specific incentive architecture, a specific founder culture, and three decades of organisational compounding.

No economic moat is a defensible verdict. The reasoning is sound: personalised service is costly to standardise, competitors are catching up, and Haidilao itself has been cutting peripheral offerings.22 The question is whether sound reasoning applied to the surface of a business misses what's underneath it.

The FPA works through this: the moat assessment, the full capital returns picture, the franchise and sub-brand optionality, the CEO transition risk, the trademark structure, and the valuation at current price.

Haidilao's moat may not be the service. It may be the system that made service repeatable at scale. The risk is that the system was designed for expansion, and the business has entered a different phase entirely.

For any investment idea I consider seriously, I need to understand both the data and the business as it actually operates today. The data is in this brief. The business, as it stands in 2026, I have yet to verify firsthand.

That means one more visit to Haidilao is required. On company expense, naturally. Strictly for research purposes.

Until then, the FPA waits.

Did Haidilao build something that outlasts

the conditions that created it? Or is it spending more each year to look like it did?

Zhang Yong emigrated to Singapore in 2018 and became a naturalised citizen. Sixth Tone, "Haidilao Founder's Singapore Connection Surprises Chinese," 2019; Forbes Asia, Singapore's Richest, 2019.

SRX Property News, "Well-known HaiDiLao is paying S$27 million for a Good Class Bungalow," 2016. The property on Gallop Road near the Botanic Gardens was designed by K2LD Architects.

Haidilao service culture, waiting area amenities, and children's play areas. The Smart Local Singapore, "13 Freebies at Hai Di Lao Singapore," March 2025; Grizzly Bulls, "Zhang Yong Biography," citing company materials.

Morningstar Equity Analyst Report, Haidilao International Holding Ltd (06862), 16 May 2026.

Haidilao FY2025 Annual Results Announcement, HKEX, March 2026.

Fiscal.ai, Haidilao International Holding Ltd (6862) Fundamentals, May 2026.

Haidilao Annual Results, March 2026; Morningstar Equity Analyst Report, 16 May 2026.

Haidilao FY2025 Annual Results Announcement, HKEX, March 2026.

Haidilao FY2025 Annual Results Announcement, HKEX, March 2026.

Haidilao FY2025 Annual Results Announcement, HKEX, March 2026.

Morningstar Analyst Note, Ivan Su, 26 August 2025, citing Haidilao H1 2025 earnings call.

Haidilao FY2025 Annual Results Announcement, HKEX, March 2026.

Morningstar Analyst Note, Ivan Su, 25 March 2026; Fiscal.ai Gross Margin data, FY2024–FY2025.

Morningstar Capital Allocation section, Ivan Su, 23 March 2026; Morningstar Analyst Note, Ivan Su, 25 March 2026. Dividend payout ratio 87%–95% in FY2024 and FY2025.

Fiscal.ai Insider Ownership data, December 2025.

Morningstar Risk and Uncertainty section, Ivan Su, 23 March 2026.

Super Hi International Holding Ltd (9658.HK / NASDAQ: HDL), FY2025 Annual Results; ir.superhiinternational.com. Net profit US$36.3 million; ROIC 9.18%; 126 restaurants across 14 countries as of December 31, 2025. Yang Lijuan returned to Haidilao April 2026; Li Yu appointed CEO of Super Hi. Tiger Brokers, "Haidilao Under Pressure: Zhang Yong Leads Female Generals Back to the Front Lines," 2026.

Morningstar Business Strategy section, Ivan Su, 18 December 2025.

Reuters, citing Singapore government data, April 2026; The Independent Singapore, "307 food establishment closures a month in 2025," April 2026.

Datassential, "Asian Food Trends 2025: The Evolution Toward Culinary Authenticity," September 2025; KED Global, "Korean dining chains sweep across US, boon for K-sauce," August 2025.

Morningstar Economic Moat section, Ivan Su, 23 March 2026.

Disclosure: Glavcot Insights and its contributors may hold positions in securities discussed in this article. All content is provided for informational and educational purposes only. Nothing published by Glavcot Insights constitutes investment advice. Readers should conduct their own research and consult qualified financial professionals before making investment decisions.

Glavcot Insights is an independent equity research publication founded by Ryan Gallinera and managed under Glavcot LLP, Singapore.

Where Clarity Meets Conviction

Glavcot Insights is now live. Join the free tier to get new research, updates, and future analysis directly in your inbox. (Check your spam folder if you don't see the confirmation email)

You might also like

Jun 21

Zijin Mining Group (2899.HK): Finding Advantage in Difficult Ground

At the surface level, Zijin exists to resolve a physical supply deficit. Decarbonisation, electric vehicles, solar and wind, transmission grids, and the computing infrastructure behind AI all require more copper at a time when the global mining sector has been starved of new supply.

22 min read

Jun 11

Haidilao (6862.HK): First Principles Analysis

If you're coming from the First Principles Brief, you already know what Haidilao does and why the business

30 min read

Jun 11

Haidilao International Holding: Snapshot

The Snapshot distills the full First Principles Analysis into a single reference page — the central question the analysis is built

7 min read

Jun 05

Pan-United Corporation Ltd (P52.SI): Concrete Is the Business. The System Around It Might Be the Moat.

There is also a durability argument that I keep returning to. Concrete has not fundamentally changed in a hundred years. You can make it greener, stronger, lighter, smarter to deliver. But the thing itself, a material that hardens into infrastructure, is not going away.

17 min read

Apr 07

Singapore Exchange Limited (S68.SI): The Exchange Is the Infrastructure

The One-Liner

Singapore Exchange does not compete for market share. It is the market. And it collects a toll