Trip.com Group Limited (TCOM): Is Travel Still the Product, or Is the Platform the Asset?

The business itself made intuitive sense. Travel is not a fad. People still want to move, explore, visit family, take holidays, and experience places beyond where they live. The form of travel may change. The human desire behind it is unlikely to disappear.

The One-Liner

Trip.com looks cyclical on the surface because travel demand moves with the economy. The more important question is whether the platform underneath has become structurally stronger than the cycle it sits inside.

The market still frames it as a China travel recovery stock. The business may already be something else.

As I sat thinking about the next business to analyse, a commercial flashed across the screen.

It opened with Jackie Chan on a studio set. Then the tagline appeared: "Let's get real!" The backdrop fell away. Behind it, a bustling, colourful scene in China. He was already there, surrounded by people in traditional costumes, completely in the middle of it. The studio had been the illusion. It was a Trip.com advertisement.

I knew the name, but I was less familiar with it compared to other travel platforms. I had not thought deeply about where it came from, or how it had grown from Ctrip into a larger travel ecosystem spanning domestic China, outbound travel, and international expansion.

The business itself made intuitive sense. Travel is not a fad. People still want to move, explore, visit family, take holidays, and experience places beyond where they live. The form of travel may change. The human desire behind it is unlikely to disappear.

The brand kept appearing. Print ads in Singapore. On a recent trip to Bali, the Trip.com name was there too. A platform I had mostly treated as background was showing up in places I actually travelled to.

That alone is not a thesis. Advertising does not make a business attractive. But it raised a question already suggested by the numbers. Was Trip.com still just a China travel recovery stock, or was the market underpricing a broader Asia-based travel platform?

Is travel still the product, or is the platform the asset?

What This Business Actually Is

Trip.com Group Limited is a global online travel agency (OTA), dual-listed on Nasdaq (TCOM) and the Hong Kong Stock Exchange (9961), with a market capitalisation of approximately US$28.4 billion as of June 2026.1 It offers accommodation reservations, transportation ticketing, packaged tours, and corporate travel management under a portfolio of brands: Ctrip and Qunar serve the domestic Chinese market, Trip.com serves international travellers, and Skyscanner operates as a global metasearch tool for flights and price comparison.2

It was founded in Shanghai in 1999, listed on Nasdaq in December 2003, and dual-listed in Hong Kong in 2021. The business predates the mass smartphone era in China. It grew by assembling the widest catalogue of hotels, flights, and travel products from thousands of separate suppliers into a single platform, then converting that depth into habitual use across the full spectrum of Chinese travellers.

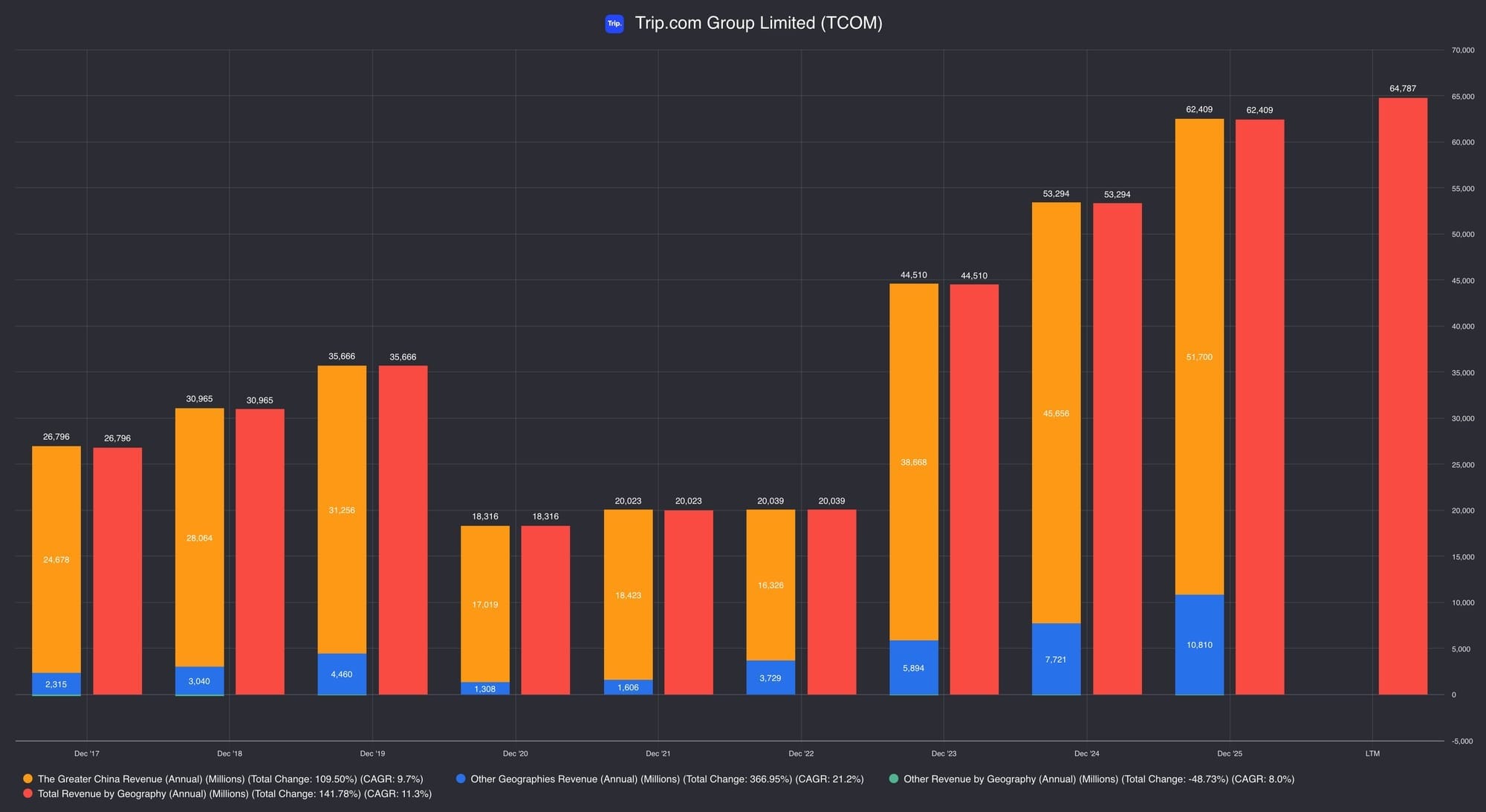

The structural feature that separates Trip.com from most OTA peers is its depth at the premium end of the hotel market. The platform holds an estimated 50% or more of the high-star hotel booking market in China by gross transaction value, where the take-rate is 9-10% versus 5-6% for budget-tier properties.3 That is not a product feature. It is an economic position built over two decades of relationship density. The international platform is growing fast, with gross bookings up approximately 65% year-over-year in Q1 2026, but Greater China still contributed roughly 83% of FY2025 revenue.4 This is a China cash engine with an international build underway.

Why This Business Exists

Trip.com was founded in Shanghai in 1999 as Ctrip. China had rising travel demand before it had a modern travel-booking infrastructure. Hotels, flights, and rail were fragmented across thousands of separate suppliers with no digital layer connecting them to travellers. Only about 10-15% of the population held a passport.5 Most Chinese people had never travelled internationally. There were earlier platforms such as Booking.com and Expedia, but they were never built for China to begin with. The founders, returnees from Western technology and finance who had seen what the internet was doing to travel distribution in the US and Europe, built the aggregation platform for that specific market from the ground up.

The aggregation it has built becomes increasingly difficult for competitors to displace. More inventory (hotels, flights, and packaged tours) attracts more travellers. More travellers attract more supply partners who want to list and access the high-intent audience. The high-intent audience justifies higher take-rates on premium properties. Higher take-rates fund the product development, loyalty programme, and marketing that bring new users in. Each side of the market reinforces the other, and the gap between Trip.com and its nearest domestic competitor in high-star hotel bookings is structural rather than marginal.

The international Trip.com platform adds a further dimension: the company is using the Ctrip/Qunar domestic franchise as its balance sheet and profitability engine to fund expansion into global markets. Whether that expansion produces durable international economics, or merely replicates the domestic position at inferior margins, is the central open question.

So, is Trip.com simply benefiting from travel demand, or is it increasingly becoming the infrastructure through which the demand flows?

The evidence on inventory depth, loyalty mechanics, and ecosystem positioning suggests the platform is closer to organising than participating. Whether it gets valued that way depends on whether the market eventually agrees.

How It Succeeds

Trip.com's moat has three sources: inventory depth on the supply side, loyalty and fulfilment on the demand side, and ecosystem cross-holdings that extend its reach beyond its own platform. None of these is a product feature. What makes them durable is that they reinforce each other. Inventory attracts travellers. Travellers deepen loyalty. Scale and loyalty justify the ecosystem holdings. The holdings feed more inventory and demand back into the system. It is a loop, not a checklist.

Inventory Depth at the Premium End

Trip.com's high-star hotel inventory is the hardest part of the moat to replicate. The company has spent twenty-five years building relationships with international hotel chains and domestic premium properties, negotiating rate parity or exclusive agreements, and maintaining the data infrastructure, review systems, and customer support that high-end travellers expect. This inventory is not available on a standardised API. It is the product of accumulated relationship density.

Meituan can list more total rooms, but it cannot replicate the average daily rate, the take-rate, or the customer profile at the top of the market. In 2019, Trip.com's domestic accommodation revenue was RMB 10.5 billion versus Meituan's estimated RMB 5.5 billion, despite Meituan booking more total room nights.6 The gap is explained by Trip.com's concentration in high-star bookings, where each transaction is worth more. That gap persists today, and the catalogue has grown: 1.7 million global listings as of December 2025, up from 1.4 million in 2019.7

The Loyalty Engine and Platform Habit

Deep inventory is what brings travellers in. Loyalty is what keeps them. Chinese travellers who book frequently accumulate points, unlock service tiers, and rely on the platform's post-booking support: last-minute itinerary changes, flight delay assistance, concierge services for high-tier members. This creates switching friction that has nothing to do with price. A Gold or Diamond member of five years is not going to migrate to a platform with inferior support to save a marginal percentage on a room.

The fulfilment infrastructure behind that loyalty is physical as well as digital. As of the end of 2025, Trip.com operated 26 customer service centres globally, supporting bookings across languages, time zones, and currencies.8 In travel, the booking is only the start of the service relationship. The product is delivered later, often by a third-party supplier, sometimes in a foreign country. A platform that can resolve problems after payment earns a kind of trust that pre-booking price comparison cannot replicate.

The mobile app now drives 70% of total orders on the international platform, and likely more on domestic.9 App-native engagement is stickier than mobile web: faster booking, seamless loyalty integration, and notifications that bring repeat purchase intent without a new search. This sits on top of the inventory advantage. Deep supply gives the traveller a reason to come. Loyalty and fulfilment give them a reason to stay.

Ecosystem Cross-Holdings

The scale built by the first two advantages is what makes the third possible. Trip.com holds ownership interests in competing platforms across its market. The most material is Tongcheng Travel Holdings (SEHK: 0780), where Trip.com holds approximately 20.86% and a board seat through Jianzhang Liang's continued directorship.11 The relationship is not merely financial. Tongcheng receives hotel booking inventory directly from Trip.com's database, and in FY2025 paid approximately RMB 3.21 billion in commissions and service fees back into the Trip.com ecosystem.12 The arrangement allows Tongcheng to access Trip.com's inventory while giving Trip.com another channel through which to monetise travel demand. In 2025, Trip.com also sold a large part of its MakeMyTrip stake back to MakeMyTrip for approximately US$3.0 billion, recording a gain of RMB 15.2 billion, while remaining the largest minority shareholder of the Indian platform.13 The effect is that Trip.com participates in travel demand well beyond its own app, and captures economics from the competitors closest to it.

The three advantages are not independent. They are a single system. Inventory depth attracts travellers. Travellers deepen loyalty. Loyalty and scale strengthen the ecosystem holdings, and those holdings feed more supply and demand back into the platform. Each turn of the loop widens the gap against any competitor trying to replicate one part in isolation. The moat is real. The open question is not whether it exists today, but how the platform’s economic role changes as AI reshapes how travellers search, decide, and transact.

The Stewards

Trip.com was co-founded by James Liang (Jianzhang Liang), Neil Shen (Nanpeng Shen), Min Fan, and Qi Ji in 1999. As of February 2026, Min Fan and Qi Ji resigned from their positions as director and president, and as director respectively, marking the departure of two of the four original founders.14 Operating leadership now sits with Jane Sun as Chief Executive Officer and James Liang as Executive Chairman.

Insider ownership deserves a closer look than the headline number suggests. All directors and officers combined hold approximately 9.4% of shares outstanding, with co-founder James Liang personally holding approximately 6.5%.15 That is meaningful founder alignment, substantially higher than what a simple summary of the five named insiders implies. One-share-one-vote structure, no dual-class arrangement. The board added two independent directors in February 2026: May Yihong Wu and Iris Yang Xiao, both with relevant financial and audit committee experience across listed Chinese and regional businesses.16

A shareholder fact worth naming separately: Baidu holds approximately 7.3% of Trip.com, a position that originated from the 2015 Qunar share exchange.17 Baidu is not a passive financial investor. Its stake reflects deep platform integration: Trip.com is embedded within Baidu's search and maps ecosystem, which provides a customer acquisition channel that competitors cannot easily replicate. That relationship is a structural distribution advantage. It also means Trip.com's largest non-institutional shareholder is a major Chinese technology platform with its own strategic interests. The alignment is mostly but not perfectly symmetrical with minority shareholders.

Capital allocation has been disciplined in one important sense: Trip.com has largely stayed within its core business. The acquisitions of Skyscanner, eLong, Qunar, and MakeMyTrip stakes were all tightly adjacent to the travel marketplace, each contributing either inventory reach or a new customer entry point.18 The 2025 MakeMyTrip partial disposal was a value-unlocking transaction that returned approximately US$3.0 billion to Trip.com while maintaining the strategic relationship.19 In August 2025, the board authorised a new share repurchase programme of up to US$5 billion in ordinary shares and ADSs, which is meaningful relative to the company's market capitalisation.20 That is capital being returned to shareholders rather than deployed into unrelated diversification. It is the right signal.

The governance concern to name directly is regulatory. Trip.com has a pattern of pushing against regulatory boundaries until compelled to stop: hidden service bundling in 2017, a string of competition and pricing investigations across 2025, and most significantly, a formal investigation by the State Administration for Market Regulation (SAMR) in January 2026 into whether the company has abused a dominant market position under the PRC Anti-Monopoly Law.21 A fine comparable to what Alibaba (RMB 18.2 billion) or Meituan (RMB 3.4 billion) received is manageable against Trip.com's cash position.22 The more serious potential outcome is structural: forced changes to business practices in the domestic hotel segment, which is the highest-margin part of the platform.

The stewards are capable and strategically disciplined. The regulatory record is not clean, and the density of incidents over the past nine months is a qualitative deterioration from what was described in the previous annual cycle.

Where the Moat Is Being Tested

Does Trip.com Keep the Customer Relationship, or Become the Booking Pipe?

The standard framing of AI risk for Trip.com is that an AI assistant could replace the platform's search and recommendation function. That risk is real, but it is probably the less important version.

The harder question is transaction execution.

Agentic AI may eventually hold traveller preferences, search inventory, complete bookings, and manage changes without the traveller entering Trip.com’s interface. If that happens, the economic risk changes structurally.

Trip.com may remain part of the booking infrastructure, but its role could shift from platform to pipe. Inventory would still move through the system. The customer relationship may not.

Pricing power, loyalty economics, and commission capture could then shift toward the agent controlling demand, rather than the platform fulfilling the transaction.

This connects directly to the financials. Trip.com's 80%-plus gross margin depends on owning the customer relationship. If agentic AI moves that relationship upstream, margin stability becomes harder to sustain. The counterpoint: travel is not just search, it is fulfilment. An AI agent still needs supplier integrations, payment rails, customer service, and cross-border execution. Trip.com has those capabilities. The open question is not whether Trip.com survives agentic AI. It is who captures the margin: the agent that controls demand, or the platform that fulfils the transaction.

TripGenie and Trip.Planner are early positioning moves.23 Platform margin versus pipe margin is the financial test that matters. Whether those investments represent a genuine pivot toward owning the agentic interface, or an incremental bet that does not fundamentally change the platform's economic position, remains to be seen.

The Regulatory Overhang

Trip.com has a pattern of regulatory friction: a 2017 hidden-bundling violation, a string of competition and pricing investigations across 2025, and a formal SAMR investigation in January 2026 into potential abuse of market dominance.24 The company's own Q1 2026 disclosure widened the characterisation to cover competition law, consumer protection, "and other areas."25 The most visible near-term risk is a fine, although business-practice remedies may matter more economically. At up to 10% of FY2025 revenue, the maximum exposure is approximately RMB 6.2 billion: large, but manageable against the RMB 104 billion cash and liquid asset base.26

The more serious risk is structural: forced changes to domestic hotel booking practices would compress the highest-margin part of the platform. A forced divestiture of Trip.com's Tongcheng stake would sever the inventory relationship that makes that cross-holding economically productive.27 In March 2026, a US securities class action was also filed, adding cross-border litigation to the overhang.28

Q2 2026 Guidance: A Meaningful Deceleration

The most significant new data point from the Q1 2026 earnings release is the Q2 2026 guidance. The company guided Q2 2026 net revenue growth at approximately 3-8% year-over-year, compared with 17% growth in Q1 2026. Management attributed this to "direct and indirect impacts from macro headwinds such as elevated energy pricing and geopolitical volatility, alongside operational adjustments the Company implemented to align with evolving industry standards and compliance frameworks."29

That phrase "operational adjustments to align with evolving industry standards and compliance frameworks" is doing considerable work. It is a compressed acknowledgement that some portion of the anticipated Q2 deceleration reflects changes the company has made, or is making, in response to the regulatory environment. The precise impact cannot be quantified from the disclosure as written, but the magnitude of the deceleration, from 17% to a midpoint of approximately 5.5%, is not trivially explained by macro headwinds alone.

The Affiliate Loss Signal

Q1 2026 also introduced a new and material line item: equity in loss of affiliates was RMB 1.15 billion in Q1 2026, compared with a loss of RMB 102 million in Q1 2025 and a loss of RMB 28 million in Q4 2025.30 This represents a step-change, and the source is not yet disclosed with specificity in the earnings release.

MakeMyTrip remains the largest investee; Tongcheng is another. A sustained deterioration in affiliate performance would reduce Trip.com's reported earnings even if its own operations continue to grow.

The VIE Structure

Investors in TCOM ADSs or 9961.HK shares own equity in Trip.com Group Limited. That company is incorporated in the Cayman Islands. They do not directly own shares in the private Chinese entities that operate parts of the domestic business. Instead, Trip.com uses contractual arrangements known as variable interest entity structures, or VIEs. These arrangements allow the holding company to consolidate the economics of PRC entities that are restricted from direct foreign ownership under Chinese law.31 This structure is common among Chinese internet companies. It is still a material ownership risk and should be stated clearly.

The contractual arrangements that substitute for direct ownership have not been tested in a Chinese court as a complete structure. The PRC government also retains the authority to change the rules under which they operate.

A platform whose domestic moat sits entirely within VIE-structured entities carries a layer of ownership uncertainty that does not exist for most Western-listed comparables. This does not change the operating economics. It does change the precision with which investors can claim them.

China Tourism Is the Engine

The international platform is the reclassification case, but Greater China is still the economic engine: roughly 83% of FY2025 revenue against 17% from other geographies.32 That split is the most important single fact in this Brief. The thesis depends on whether it shifts.

Greater China at 83% of FY2025 revenue confirms this is still a China cash engine funding an international build. The Other Geographies line (21.2% CAGR since 2017 vs. Greater China at 9.7%) is the reclassification lever. The LTM data point shows international continuing to accelerate into 2026.

China tourism has three parts. Domestic travel provides the base: high volume, but spend per trip is softening. Outbound travel is the higher-value upgrade path, where full-stack platform capability earns more per transaction. Inbound travel is the newest vector, with bookings up approximately 90% year-over-year in Q1 2026 on the back of expanded visa-free policies.33 The key question is not whether Chinese people keep travelling. It is whether that travel comes with higher spend and cross-border complexity, or mostly as lower-cost domestic volume. The first supports platform economics and a re-rating. The second gives revenue but not reclassification.

What the Engine Shows

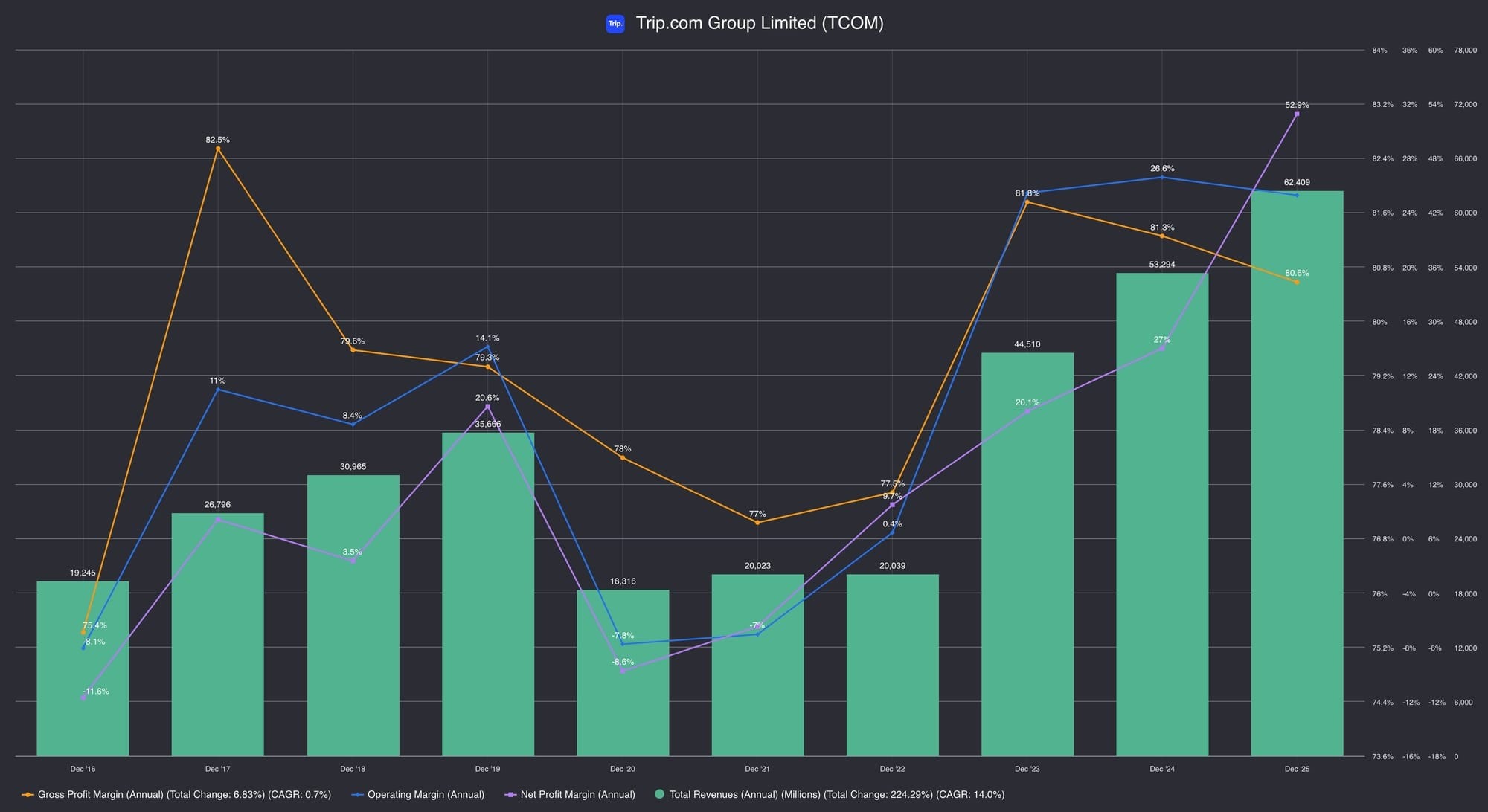

Revenue reached RMB 62.4 billion in 2025, compounding at approximately 14% annually since 2016, and the post-pandemic reset placed the business at a structurally higher base than pre-COVID levels.34 Gross margin has held above 78% throughout, confirming the asset-light commission model.35 Operating margin was 25.3% for full-year 2025, with a long-term target of 25-30%.36

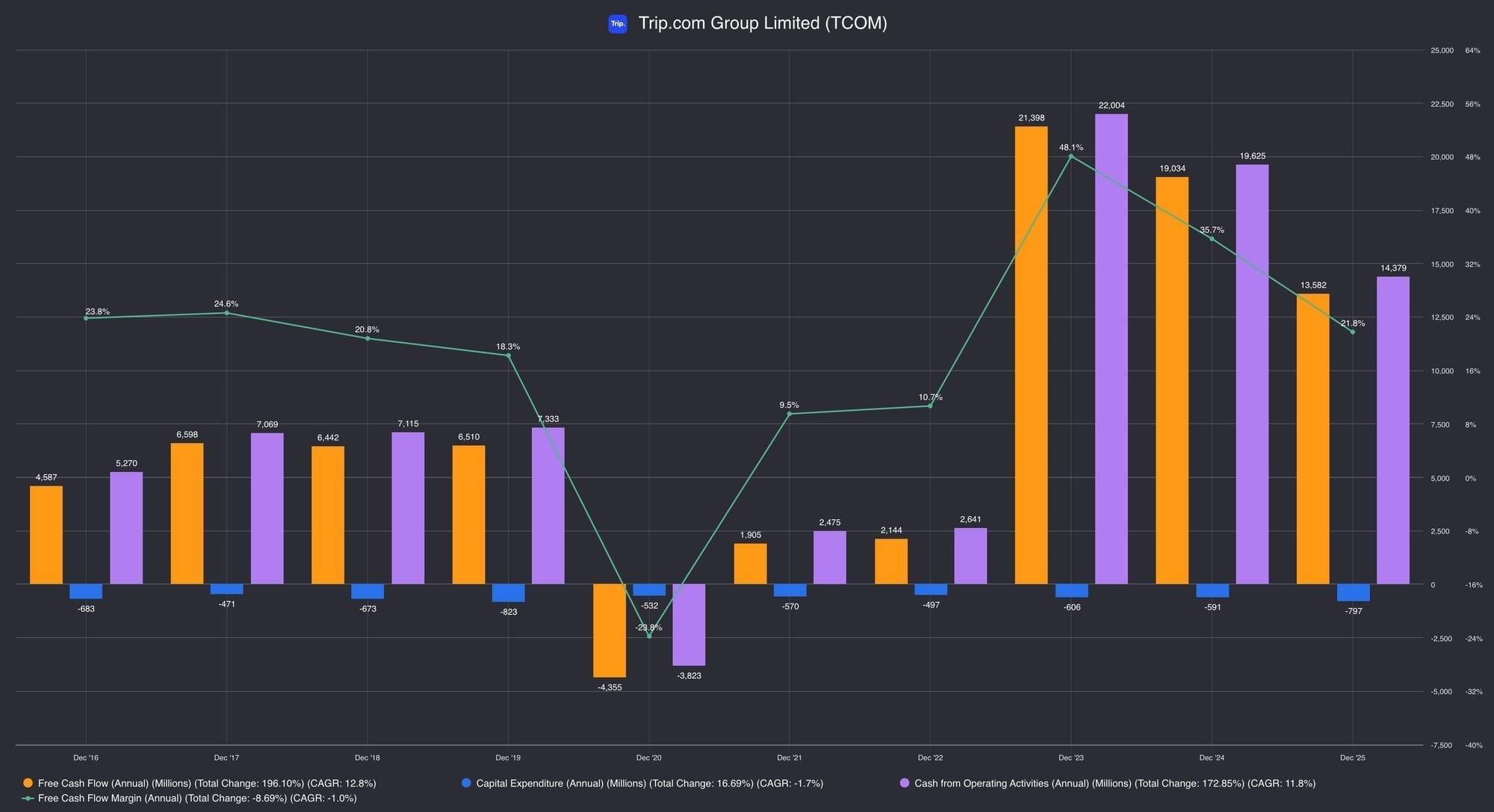

Gross margin has held above 78% throughout, confirming the asset-light commission model. Q1 2026 showed modest compression to 79.5%, the first reading below the recent 80-82% range. Operating margin is the cleaner measure of platform economics. The 2025 net margin spike (approximately 53%) is the MakeMyTrip disposal gain, not a run-rate figure.The pandemic break is visible, as is the post-reopening reset to a structurally higher base. The 2025 net income spike reflects the MakeMyTrip disposal gain, not the operating engine. Read revenue and operating income together; the net income line is distorted.Revenue has moved to a structurally higher base, while operating cash flow has declined from its 2023 peak. The divergence is the clearest financial cost of the current expansion phase.

The balance sheet is strong. Cash and liquid assets totalled RMB 104.0 billion as of March 2026, against total debt of RMB 30.8 billion.38

But operating cash flow declined from RMB 22.0 billion in 2023 to RMB 13.6 billion in 2025, even as revenue grew about 17% over the same period.39 The question is not whether Trip.com can fund its international expansion, but whether that investment eventually restores cash conversion at acceptable margins.

What I'll Be Looking At

Trip.com in mid-2026 is a mature, cash-generative, market-dominant OTA in China with a genuine and accelerating international footprint. The domestic franchise is deeply entrenched. The balance sheet is clean. The business has demonstrated it can survive category disruption, pandemic-level demand collapse, and intense domestic competition across two decades. Those are not small things. The reclassification case is real. So is the discount.40 These are the four questions that determine which one is right.

Reopening vs. normalised growth. How much of the 2023-2025 revenue reset is structural, and how much is catch-up demand that fades?

Operating income vs. investment-driven net income. The 2025 headline figures are inflated by the MakeMyTrip disposal. What does the clean operating picture actually look like?

China exposure vs. international platform expansion. Modelling the overseas platform as a standalone: does the current marketing spend justify the reinvestment?

Platform moat vs. regulatory and agentic disruption. What does the P&L look like if SAMR compresses domestic hotel take-rates? And where does Trip.com sit in the distribution stack as agentic booking takes hold?

Is Trip.com's international reinvestment creating the next platform layer, or masking a maturing China OTA facing regulatory and AI-driven margin compression? The answer determines whether the current discount is an opportunity or a correct assessment.

The evidence suggests that Trip.com has a moat today. Whether that moat is being extended into a new platform layer, or quietly compressed by the forces reshaping how the world books travel, remains to be seen.

First Principles Analysis coming this September

Footnotes:

Footnotes (40)

Morningstar Equity Analyst Report, Trip.com Group Ltd ADR TCOM, as of 18 Jun 2026. Market Cap: USD 28.40 billion.

Trip.com Group Limited Annual Report on Form 20-F for fiscal year ended December 31, 2025, filed April 28, 2026 ("20-F"). About Trip.com Group Limited section.

Morningstar Equity Analyst Report, Economic Moat section. Take-rate estimates: high-star 9-10% vs. budget 5-6%. Market share estimate for high-star hotels: approximately 50%-plus GMV share in China.

Q1 2026 Release, Key Highlights. Gross bookings on international platform increased approximately 65% year-over-year in Q1 2026. Fiscal.ai chart data, Revenue by Geography: Greater China FY2025 approximately RMB 51,700 million, representing approximately 83% of total FY2025 revenue of RMB 62,409 million.

20-F. "We commenced our business in June 1999. In March 2000, we established an exempted company with limited liability under the Companies Act in the Cayman Islands, Ctrip.com International, Ltd., as our new holding company...In October 2019, we changed our company name to Trip.com Group Limited." Founding history and name change section. Co-founders James Liang and Neil Shen had backgrounds in US technology (Oracle) and finance (Yale MBA) respectively before returning to China to found Ctrip.

Morningstar Equity Analyst Report, Bulls Say, citing passport penetration of approximately 10-15% of China's population.

20-F, 1.7 million global accommodation listings as of December 31, 2025. Morningstar Equity Analyst Report for 2019 figure of 1.4 million.

20-F. Trip.com Group operated 26 customer service centres globally as of December 31, 2025. Customer service centre disclosure.

Morningstar Equity Analyst Report, Analyst Notes Archive, August 28, 2025. App accounts for 70% of orders on international platform.

20-F, Directors, Senior Management section. Jianzhang Liang has served as director of Tongcheng Travel Holdings Limited since 2016.

Tongcheng Travel Holdings 2025 annual results and Trip.com 20-F related-party transactions. Tongcheng paid approximately RMB 3.21 billion in commissions and service fees to the Trip.com ecosystem in FY2025, arising from hotel booking inventory supplied by Trip.com's database. Source: Bamboo Works analysis citing Tongcheng filings.

20-F. "In June 2025, we entered into a share repurchase agreement...to sell 34,372,221 Class B ordinary shares that we held to MakeMyTrip for an aggregate consideration of approximately US$3.0 billion for cancellation...we recorded a gain from investment of RMB15.2 billion." Trip.com remained the largest minority shareholder of MakeMyTrip following the transaction.

Q4 2025 Release, Board Composition Changes section. Min Fan resigned as director and president; Qi Ji resigned as director.

20-F, Directors, Senior Management and Employees section. All directors and officers as a group hold approximately 63,766,293 shares, representing approximately 9.4% of ordinary shares outstanding. Co-founder James Liang personally holds approximately 6.5%.

Q4 2025 Release, Board Composition Changes section. Appointments of May Yihong Wu and Iris Yang Xiao as independent directors.

Trip.com Group Limited 2025 Form 20-F ("20-F"), Major Shareholders section. Baidu, Inc. holds 45,953,524 shares, representing approximately 7.3% of ordinary shares outstanding. Stake originated from the 2015 Qunar share exchange transaction.

Morningstar Equity Analyst Report, Capital Allocation section.

20-F. MakeMyTrip share repurchase, US$3.0 billion consideration for 34,372,221 Class B shares, closed July 2025.

20-F. "In August 2025, our board of directors authorized a new share repurchase program under which we may repurchase up to an aggregate of US$5 billion of our outstanding ordinary shares and/or ADSs."

20-F, Risk Factors. "In January 2026, we received notice that the SAMR commenced an investigation into whether we have abused or are abusing a dominant market position to engage in monopolistic conduct pursuant to the PRC Anti-Monopoly Law."

Morningstar Equity Analyst Report, Analyst Notes Archive, January 15, 2026. Alibaba fined RMB 18.2 billion; Meituan fined RMB 3.4 billion for comparable practices in 2021.

Morningstar Equity Analyst Report, Analyst Notes Archive, August 28, 2025. "Trip.com has mentioned the potential for AI agents to replace call center representatives in the longer term."

20-F, Risk Factors. "In January 2026, we received notice that the SAMR commenced an investigation into whether we have abused or are abusing a dominant market position to engage in monopolistic conduct pursuant to the PRC Anti-Monopoly Law."

Q1 2026 Release, Recent Development section. "The Company is and has been the subject of investigations or inquiries by national authorities regarding competition law matters, consumer protection issues, and other areas." Contrast with narrower framing in Q4 2025 Release.

PRC Anti-Monopoly Law, Article 57. Maximum penalty for abuse of dominant market position: up to 10% of preceding year's sales revenue. On FY2025 net revenues of RMB 62,409 million, a maximum fine would be approximately RMB 6.2 billion. Trip.com Q1 2026 Release balance sheet: cash and liquid assets totalling RMB 104.0 billion as of March 31, 2026.

Bamboo Works, "Tongcheng's rosy report fails to discuss the worrisome elephant in its house," citing Tongcheng Travel Holdings filings. Trip.com holds approximately 20.86% of Tongcheng; Tongcheng receives hotel booking inventory from Trip.com's database as part of the commercial arrangement. SAMR-forced divestiture would sever this inventory relationship.

Hagens Berman, GlobeNewswire, May 6, 2026. "TCOM SHAREHOLDER UPDATE: Trip.com (TCOM) Facing Securities Class Action After AI Pricing Controversy and Anti-Monopoly Probe Sends Shares Tumbling." Putative US federal securities class action filed in or around March 2026, arising from SAMR investigation disclosure and AI pricing controversy.

Q1 2026 Release, Business Outlook section. "For the second quarter of 2026, the Company expects net revenue to grow by approximately 3%-8% year-over-year...This reflects direct and indirect impacts from macro headwinds such as elevated energy pricing and geopolitical volatility, alongside operational adjustments the Company implemented to align with evolving industry standards and compliance frameworks."

Q1 2026 Release, Unaudited Consolidated Statements of Income. Equity in loss of affiliates: RMB (1,151) million in Q1 2026, vs. RMB (102) million in Q1 2025 and RMB (28) million in Q4 2025.

20-F. Holding company structure, VIE contractual arrangements, and PRC foreign ownership restriction disclosures. Item 3 Risk Factors and Item 4 Information on the Company sections.

Fiscal.ai chart data, Trip.com Group Limited TCOM, Revenue by Geography chart. Greater China FY2025: RMB 51,700 million (CAGR 9.7% since 2017). Other Geographies FY2025: RMB 10,810 million (CAGR 21.2% since 2017). Total revenue CAGR 11.3%.

Q4 2025 Release, Key Highlights. The Company served approximately 20 million inbound travellers during 2025. Q1 2026 Release, Key Highlights: inbound travel bookings surged approximately 90% year-over-year in Q1 2026.

Fiscal.ai chart data, Trip.com Group Limited TCOM, Revenue chart. Total revenue 2025: CNY 62,409 million. CAGR 14.0% from 2016-2025.

Morningstar Equity Analyst Report, Business Strategy and Outlook. Long-term non-GAAP operating margin target 25-30%.

Q1 2026 Release, Unaudited Consolidated Statements of Income. Gross profit Q1 2026: RMB 12,878 million on net revenues of RMB 16,208 million, implying a gross margin of approximately 79.5%. Compared with 80.6% for full-year 2025.

Q1 2026 Release, Unaudited Consolidated Balance Sheets as of March 31, 2026. Cash, cash equivalents, restricted cash, short-term investments, and held-to-maturity products totalling RMB 104.0 billion. Total debt (short-term debt and current portion of long-term debt, plus long-term debt): RMB 20,087 million plus RMB 10,742 million, approximately RMB 30.8 billion.

Fiscal.ai chart data, Trip.com Group Limited TCOM, Free Cash Flow and Operating Cash Flow chart. Operating cash flow: RMB 22,004 million (2023), RMB 19,625 million (2024), RMB 13,582 million (2025).

Morningstar Equity Analyst Report. Last close USD 45.10; fair value estimate USD 70.00; Price/FVE 0.64, as of 18 June 2026.

Disclosure: Glavcot Insights and its contributors may hold positions in securities discussed in this article. All content is provided for informational and educational purposes only. Nothing published by Glavcot Insights constitutes investment advice. Readers should conduct their own research and consult qualified financial professionals before making investment decisions.

Glavcot Insights is an independent equity research publication founded by Ryan Gallinera and managed under Glavcot LLP, Singapore.

Where Clarity Meets Conviction

Glavcot Insights is now live. Join the free tier to get new research, updates, and future analysis directly in your inbox. (Check your spam folder if you don't see the confirmation email)

You might also like

Jul 07

Sheng Siong Group Ltd (OV8.SI): Can a Supermarket Compound?

Sheng Siong's competitive position rests on three components. None is a single decisive wall. Each is an operating advantage that means little on its own and matters because it works with the others: location, procurement, and fresh food execution, coordinated across the network.

25 min read

Jul 01

Pan-United Corporation Ltd. (P52.SI): First Principles Analysis

If you're coming from the First Principles Brief, you already know what Pan-United does and why the

31 min read

Jun 21

Zijin Mining Group (2899.HK): Finding Advantage in Difficult Ground

At the surface level, Zijin exists to resolve a physical supply deficit. Decarbonisation, electric vehicles, solar and wind, transmission grids, and the computing infrastructure behind AI all require more copper at a time when the global mining sector has been starved of new supply.

22 min read

Jun 05

Pan-United Corporation Ltd (P52.SI): Concrete Is the Business. The System Around It Might Be the Moat.

There is also a durability argument that I keep returning to. Concrete has not fundamentally changed in a hundred years. You can make it greener, stronger, lighter, smarter to deliver. But the thing itself, a material that hardens into infrastructure, is not going away.

17 min read

May 19

Haidilao (6862.HK): Is Service the Moat, or the Cost?

Haidilao's service quality did not emerge from a training manual. It was built through a specific mechanism: a master-apprentice incentive structure where store managers are compensated not just on their own store's performance, but on the performance of managers they trained