Sheng Siong Group Ltd (OV8.SI): Can a Supermarket Compound?

Sheng Siong's competitive position rests on three components. None is a single decisive wall. Each is an operating advantage that means little on its own and matters because it works with the others: location, procurement, and fresh food execution, coordinated across the network.

The One-Liner

Sheng Siong sells groceries. That sounds too simple to be interesting.

The harder question is whether decades of procurement discipline, fresh food execution, and neighbourhood positioning have turned an essential, recurring demand into a genuinely durable cash-compounding machine, inside a market the size of Singapore.

The market has largely decided the answer is yes. The shares have re-rated to a premium multiple near their all-time high. Whether the business earns that verdict is what the financial record has to show.

Sheng Siong first entered my investment radar in early 2021, after news broke that the company had awarded its employees an unusually large bonus following a strong FY2020.

I already knew it as one of Singapore’s major supermarket chains, but at the time I had not realised it was publicly listed. The news reflected well on management, so I took a brief look.

I dismissed it fairly quickly.

At the time, I was still new to investing and saw its single-digit net profit margin as a sign that the business was not especially attractive. I had not yet understood that different industries must be judged by different economics.

For a supermarket, the strength is not necessarily a large profit on every basket. It is the ability to keep prices competitive, move inventory quickly, control waste and operating costs, generate cash consistently, and repeat that process across many stores.

Seen through that lens, Sheng Siong looked different. Its relatively modest margin was not automatically a weakness. Maintaining it consistently while offering value to customers could itself be evidence of a resilient operating model. By the time I understood that distinction, the market appeared to understand it too. Sheng Siong was already being priced as a high-quality business.

That did not make it less interesting. It changed the question from whether Sheng Siong was a good business to whether its operating system could continue compounding fast enough to justify the price already placed on it.

What This Business Actually Is

Sheng Siong Group Limited is a supermarket operator listed on the SGX Mainboard under the ticker OV8.SI, with a market capitalisation of approximately S$4.8 billion as of late June 2026, at a share price of around S$3.20 on roughly 1.50 billion shares.1 It operates 87 supermarkets in Singapore and 6 stores in Kunming, China, as of 31 March 2026, across a Singapore retail footprint of roughly 759,961 square feet.2

The stores sell fresh produce, seafood, meat, vegetables, frozen food, dry groceries, and household necessities. The format is neighbourhood-scale, concentrated in and around Housing Development Board (HDB) public housing estates, where about 80% of Singapore's resident population lives.3 A small e-commerce channel, Sheng Siong Online, contributes roughly 1% of revenue and is described by management as modestly profitable.4

Revenue for FY2025 was S$1,570 million, up 9.9% on FY2024 and a compound annual growth rate of approximately 8% over the past decade from S$796.7 million in FY2016.5 Revenue for 1Q FY2026 was S$452.8 million, up 12.4% year-on-year, driven mainly by twelve new stores opened in FY2025.6 China contributed about 2.1% of total revenue in 1Q FY2026 and ran at breakeven.7 The company was founded in 1985 by three brothers, Lim Hock Eng, Lim Hock Chee, and Lim Hock Leng, who remain active today with Lim Hock Eng as Executive Chairman and Lim Hock Chee as Chief Executive Officer.8 This is a founder-controlled, family-run operation with a listed vehicle.

Why This Business Exists

Every household has to eat, and grocery spending is one of the few genuinely recurring, non-discretionary obligations in a consumer's budget. Singapore's grocery market is led by the NTUC FairPrice cooperative, founded in 1973 with an explicit social mission to keep essential goods affordable, alongside DFI Retail Group's Cold Storage and Giant chains.9 That is the field Sheng Siong entered, and the question of why it exists is really the question of what room was left in it.

The answer is in the founding. The Lim brothers grew up helping at their father's pig farm in Punggol. When an oversupply of pigs coincided with the government's move to phase out pig farming, Lim Hock Chee and his wife rented a pork counter inside a Savewell provision store in Ang Mo Kio. The Savewell chain then ran into financial trouble, and with seed capital from their father the brothers bought the failing outlet in 1985 and turned it into the first Sheng Siong store.10 They ran it on a simple principle that still defines the business: a wide range of no-frills goods sold at low margins and high volume, with cost discipline measured down to the profit earned per square foot of shelf space.11

That value DNA found its structural home in Singapore's public housing. Over 80% of the population lives in HDB estates that are geographically clustered, largely car-free for daily errands, and served by a residential composition that changes slowly. A store secured in one of these locations does not have to buy foot traffic through advertising. The neighbourhood supplies it. This is the condition that separates a heartland grocer from most of retail: the customer is a household that has to eat, and the only real question is which nearby store is the most reliable, accessible, and fairly priced.

Fresh food is what let the business compound rather than merely survive. In 1995 Sheng Siong opened a Woodlands store built around a wet-market-style fresh section inside a supermarket, a "wet and dry" format that competed directly with traditional wet markets on convenience while holding prices down.12 That format became the template. It positioned Sheng Siong as the value-and-fresh alternative in the same heartland catchments the market leader occupies, and it worked well enough that FairPrice's own leadership has publicly named Sheng Siong its biggest competitor and now runs dedicated stores to fight it on price.13

The deeper question is whether that position rests on a structurally lower-cost operating model or simply on proximity and habit. That is what the financial record has to answer.

How It Succeeds

Sheng Siong's competitive position rests on three components. None is a single decisive wall. Each is an operating advantage that means little on its own and matters because it works with the others: location, procurement, and fresh food execution, coordinated across the network and compounded over decades of customer habit.

Location Lock-In Through HDB Tender Access

Most of Sheng Siong's stores sit in HDB estates, and new locations depend on winning government-issued HDB retail tenders. That creates a supply constraint working in the company's favour. Not every competitor can access the same sites, and the tender process is formal and commercially evaluated. Management has confirmed directly that the expansion strategy is tied to HDB supply, growing the Singapore network to 87 stores today.14 New HDB stores are primarily on a lease-term basis, with the property acquired for the purpose of operating a supermarket rather than as a real-estate play.15

Once a store is established in a mature estate, habit forms. The store that becomes part of a household's weekly routine in year one tends to remain part of it in year five. Not because customers are contractually locked in, but because a reliable, accessible, fairly priced store gives them no reason to leave.

Procurement, Distribution, and the House Brand

As the network grows, procurement leverage grows with it. The family’s roots in pig farming gave them an unusually intimate feel for supply-chain costs, a capability the group has translated into procurement discipline across categories.16 Like every grocer in Singapore, Sheng Siong sells goods that are overwhelmingly imported; its response is to source directly where it can, buy at scale, and develop private-label alternatives rather than relying solely on branded distributors.17 Sourcing is not a back-office function but where a large share of the margin is won or lost, and it runs on a self-operated central distribution centre. Singapore’s compact geography makes centralised distribution unusually effective for every grocer here; the open question for Sheng Siong is whether its self-run network exploits that density more efficiently than competitors.18

The house brand is the clearest output of that leverage: more than 1,750 products across roughly 25 house brands priced 5 to 20 percent below leading brands.19 It does three things at once: it gives price-sensitive customers a credible alternative, gives Sheng Siong greater control over pricing and margin than branded equivalents, and builds differentiation that a competitor stocking only the same branded goods cannot replicate.

Direct sourcing, long-term supplier relationships, and an expanding house brand show up in the gross margin trend, which has risen from about 25.7% in FY2016 to above 30.5% in FY2025.20That is a 480-basis-point improvement in a business where every basis point takes daily operational discipline. It is a decade-long structural gain, not one good year.

Fresh Food Execution and Customer Frequency

Fresh food, meaning seafood, meat, vegetables, and fruit, is the most operationally demanding part of the business and the single biggest driver of customer frequency. Fresh food can bring households back more frequently than dry groceries alone, increasing the share of the annual basket captured.

It is also intensive to run: cold chain management, waste control, daily repricing, perishable supplier relationships, and in-store presentation all demand sustained capability. A competitor can copy a Sheng Siong dry-goods range in months. Fresh food is harder, though established rivals like FairPrice and the wet markets are not starting from zero; they already have cold chain and sourcing relationships. What is difficult to replicate is not fresh food as a category but the coordinated combination of freshness, value pricing, high turnover, low waste, and neighbourhood-scale economics, held together consistently across the network. The company has deployed AI-powered scales for fresh pricing accuracy and is developing an AI-driven demand forecasting system with AI Singapore to improve inventory management and cut waste.21 That is the right place to invest.

The advantage is not the groceries, and it is not any single component. It is the coordination of neighbourhood location, procurement and distribution, and fresh food execution, bound together by cost discipline, into one operating system repeated across 87 stores and decades of customer habit. Whether that system is genuinely self-reinforcing, where scale sharpens purchasing, sharper prices sustain traffic, and traffic feeds back into scale, or whether it is simply a very well-run grocer, is the question the moat ultimately turns on. Either way it is a "many small edges" model, resilient but not invulnerable, and it does not survive a sustained failure across the components at once.

The Stewards

Sheng Siong was founded by three brothers who remain actively involved. Lim Hock Eng serves as Executive Chairman, Lim Hock Chee as Chief Executive Officer, and Lim Hock Leng in an executive capacity. All three have drawn the same basic salary since their service agreements were formalised in 2011.22 Variable bonuses are performance-linked and tied directly to financial results, so in a weak year executive compensation compresses alongside earnings.23

The founding family retains a controlling stake of roughly 52%, held about 30% through the family holding company, Sheng Siong Holdings Pte. Ltd., and about 22% directly by the three brothers, aligning family wealth directly with long-term business outcomes.24 Institutions hold only about 11%, leaving the register tightly held. This is not only a governance positive. It is a structural signal about the time horizon management operates on. A modest step toward professionalising the finance function came in February 2026, when Fan Hongbo was elevated from Financial Controller to Chief Financial Officer.25

At the April 2026 AGM, CEO Lim Hock Chee's re-election drew 99.82% support, with Executive Chairman Lim Hock Eng absent due to minor illness.26 The business has been built and run by three founders for more than four decades. Whether professional successors would preserve the operating culture and capital discipline that define the company is the open governance question here.

Capital allocation has been disciplined in the ways that matter most for a grocer. The group has pursued no unrelated acquisitions, issued no dilutive equity since a single placement in 2014, and has not leveraged the balance sheet for financial engineering.27 The cash position of S$461 million as of 31 March 2026 is described by management as reserved for working capital, store acquisition opportunities, and the group's largest-ever capital commitment, a new automated distribution centre and headquarters at Sungei Kadut.28 Whether that reserve is a strategic war chest or an accumulating inefficiency is left open.

External recognition offers some independent calibration. In 2024 SIAS conferred its Outstanding CEO Award on Lim Hock Chee, named the company Most Transparent Company in the Consumer Staples category, and the group has ranked among the top ten globally in the Grocery and Convenience Stores category of the Newsweek and Statista Most Trustworthy Companies list.29 These are not analytical conclusions. They are not irrelevant signals either.

Where the Moat Is Being Tested

The risks below are not separate from the business model. They are where the model is tested.

Can the Neighbourhood Model Keep Expanding?

Singapore is a city-state of roughly 5.9 million people. At 87 stores and a target of three to five new openings a year, the expansion runway is inherently finite. What matters more as the network matures is same-store economics. Management has acknowledged directly that newly opened stores need time before they contribute meaningfully to earnings, while older stores in mature estates can grow more slowly in the absence of new residential development nearby.30 Comparable same-store sales rose 3.5% in Singapore in 1Q FY2026.31 If that rate slows as the network ages, earnings growth compresses even while store count keeps rising, and the market tends to compress the multiple before the underlying business has visibly deteriorated.

Can Productivity Outrun Labour and Rental Inflation?

Grocery retail is intensely labour-dependent. Singapore's Progressive Wage Model (PWM) sets a rising wage floor for retail workers. Sheng Siong raised retail salaries in September 2025 to meet PWM requirements, contributing to an S$8.8 million rise in selling and distribution staff costs in 1Q FY2026 alone, the single largest cost increase in the quarter.32 Total staff costs for the quarter were S$73.2 million, up from S$63.1 million a year earlier.33 The PWM will keep pushing upward, and there is no structural way to avoid it. The company can absorb it through gross margin gains, productivity from AI and automation, and disciplined pricing. Each lever has a limit, and labour inflation combined with rental renewals on well-located estates is the primary margin-compression risk for the outer years.

Does the Sourcing Engine Hold Up Under Pressure?

That Singapore imports over 90% of its food is not the interesting fact, because every grocer here faces the same exposure to imported-input inflation, currency swings, tariffs, and supply-chain disruption.34 The test is whether Sheng Siong's sourcing responds better than rivals' when those pressures hit. The operator that diversifies suppliers, buys direct, and manages the chain most tightly is the one that protects its margin when input costs move, which is where the procurement advantage claimed earlier either proves real or proves ordinary.

Management frames the exposure the same way. It notes that the group does not export and so sees no direct tariff impact, and that its answer to a more uncertain cost environment is to diversify supply sources, deepen supplier relationships, and lean on efficient supply-chain management.35 That is the right playbook. Whether it delivers genuinely more resilient sourcing than peers, or simply benefits, like everyone, from a benign stretch of input costs, is the same question the gross margin trend raises.

Will Sungei Kadut Deepen or Dilute the Advantage?

Logistics is the quiet constraint on this business. Sheng Siong runs its own warehouse and distribution centre at Mandai Link, completed in 2011 and designed for a much smaller store network. With the group now operating more than 85 supermarkets, the decision to build a new facility indicates that additional capacity is required. Analysts believe the existing constraint may already be limiting the opportunistic bulk buying that helps support margin.36

The response is the largest capital commitment in the group’s history. In September 2025 Sheng Siong took a 33-year lease on a Sungei Kadut site roughly 2.5 times the size of Mandai Link. The company plans to build a new automated distribution centre and headquarters, with total outlay estimated at around S$520 million, funded by internal cash and borrowings.37 It will add temperature-controlled zones, integrated food processing, and warehouse automation, with capacity for at least 120 supermarkets and completion targeted around 2029.

The strategic logic is sound: it adds the capacity needed for further store growth, can improve procurement and distribution efficiency, and may support online fulfilment. The risk is that it is large, multi-year, partly debt-funded, and will carry a meaningful depreciation load once live, before all the incremental stores needed to justify it are open.

These are the four immediate tests of the operating system. Other questions remain, from online fulfilment and inventory efficiency to China and cross-border spending; they carry different weights, and the questions that follow take up the ones that matter most.

What the Engine Shows

The financial profile over the past decade reflects a business that has strengthened steadily without dramatic discontinuity. There is no pandemic collapse and recovery to parse. There are no investment gains distorting the headline figures. The picture is unusually clean for a company that has been growing.

Revenue has grown from S$796.7 million in FY2016 to S$1,570 million in FY2025, a compound annual rate of about 8%.38 The 1Q FY2026 figure of S$452.8 million is up 12.4% year-on-year.39

Read the bars for the growth trajectory and the EPS CAGR line for quality of that growth. Revenue has risen every year bar a brief normalisation after the FY2020 pandemic uplift, with LTM revenue at S$1,619.8 million. The diluted EPS 3Y CAGR line, negative as recently as FY2023, has recovered to 5.44%, confirming revenue growth is now translating into per-share earnings.

Gross margin tells the more important story. From about 25.7% in FY2016 it has expanded to above 30.5% in FY2025 and reached 31.0% in 1Q FY2026.40 That is a 480-basis-point structural improvement held across a decade in a sector where most operators struggle to keep margins flat. It reflects the shift toward fresh produce, direct sourcing, procurement scale, and the house brand, not one-off cost cuts.

Watch the gross margin line for the structural trend and ignore the FY2020 bump, which was pandemic-era demand, not mix. Gross margin sits at 31.5% LTM, operating margin at 11.1%, net margin at 9.5%, all above their FY2016 starting points. The floor since FY2022 has held near 30% gross margin, which is the evidence that the procurement and mix gains are durable.

Net profit attributable to owners in FY2025 was S$149.5 million, up 8.7% on FY2024, at a net margin of about 9.5% and earnings of S$0.099 per share.41 EPS for 1Q FY2026 was 2.87 cents, up 11.7% year-on-year.42 There are no material investment gains in these figures. What you see is what the operating business earns.

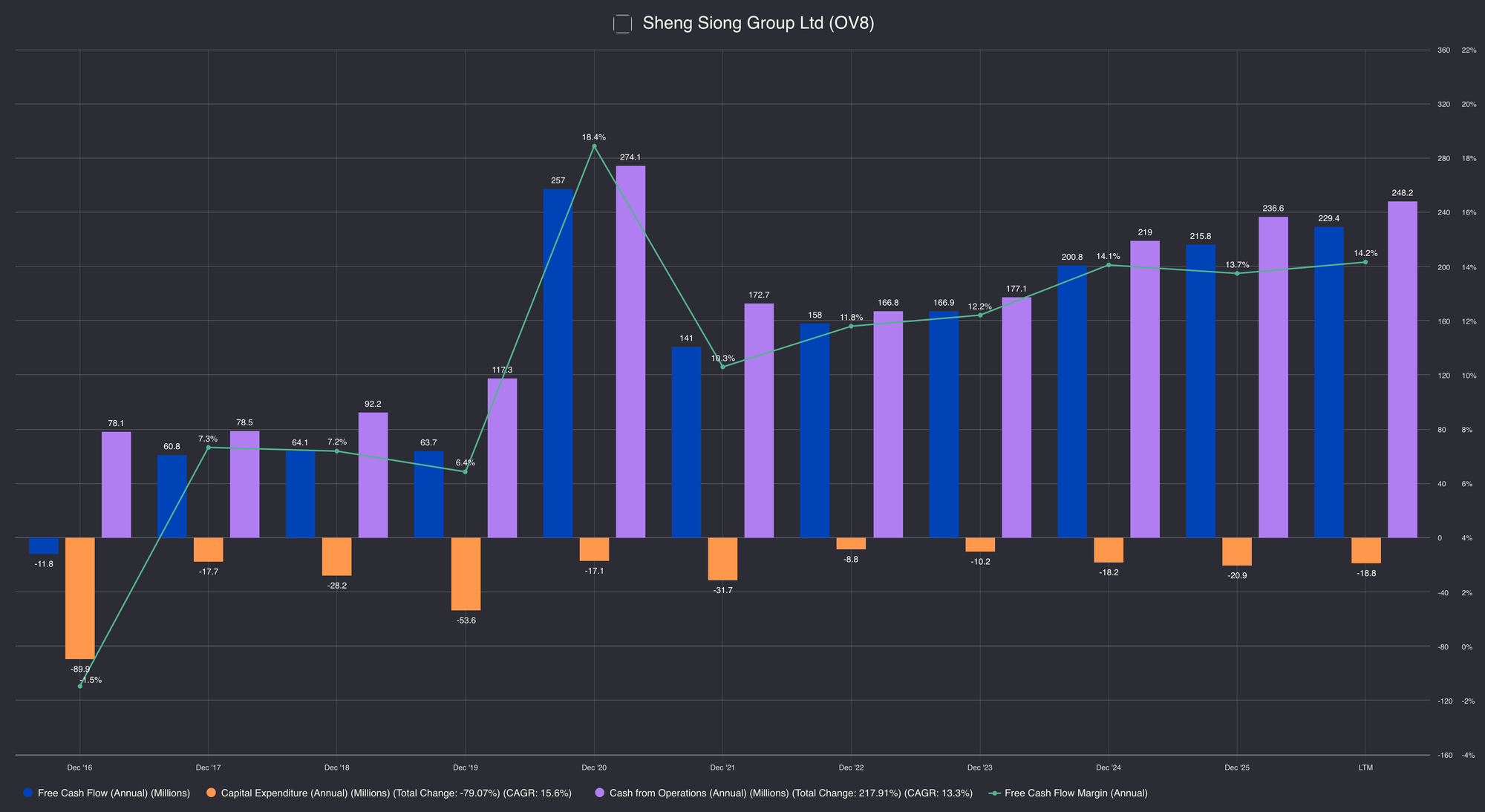

Cash generation is the most compelling part of the record. Cash from operations grew from S$78.1 million in FY2016 to S$236.6 million in FY2025, a compound annual rate of about 13.3%.43 Free cash flow margin reached about 13.7% in FY2025 and 14.2% LTM.44 Capital expenditure has stayed modest and disciplined, at S$20.9 million in FY2025 and S$2.9 million in 1Q FY2026, mostly store fit-out and vehicles.45

The core of the cash-machine thesis is operating cash flow compounding near 13% a year while capex stays below S$25 million in most years. The FY2019 capex step-up marks the prior store-expansion cycle and is the right reference point when weighing the committed Sungei Kadut build.

The balance sheet is a genuine asset. Cash and cash equivalents stood at S$461.1 million as of 31 March 2026, against total equity of S$634.6 million.46 The reported Debt/Equity ratio of roughly 0.3x is attributable entirely to lease liabilities of S$162.7 million, not financial borrowings; the current ratio of about 1.8x and EBITDA-to-interest coverage above 35x round out a group carrying no meaningful financial debt.47 Returns on capital confirm the quality: ROIC has held in the mid-20s percent and ROE in the mid-to-high-20s percent through the decade, high for a mature, capital-light retailer, and evidence that new capital deployed into new stores still earns at acceptable rates.48

The test is whether returns dilute as the asset base grows. Total assets have risen from S$387.8 million in FY2016 to S$1,074.9 million LTM, yet ROIC sits at 26.8% LTM and ROE at 25.4%, both in the same band they occupied a decade ago. Returns have not thinned with scale, which is the key evidence on whether the capital deployment is creating value or merely enlarging the business.

One fact the reader should hold before turning to valuation: the market has already noticed. The shares have re-rated roughly 72% over the past year to around S$3.20, near an all-time high, at about 31 times trailing earnings, with a dividend yield near 2.2% on a payout of roughly 70%.49 What the engine earns is no longer a secret. Whether the price paid for it is reasonable is the work reserved for the analysis to come.

What I'll Be Looking At

Sheng Siong in mid-2026 is a cash-generative, founder-controlled, operationally disciplined grocer with a clean balance sheet, a decade of margin expansion, and a defined store-opening runway in Singapore. The business is not complicated and the execution is genuinely good. It is also no longer a hidden one: the market has re-rated the shares to a premium multiple near their high. This is not a reclassification story where the category has been misread. The unresolved question is whether the compounding is durable and fast enough to justify the price the market now assigns, and five questions decide the case.

Store maturity and space productivity. Sheng Siong does not disclose per-store profitability, so this has to be reconstructed from the same-store and new-store splits and from sales per square foot: does the new-store cohort earn like the mature estate base, and is the network becoming more productive per square foot or simply larger?

Inventory efficiency and cash conversion. Do inventory turns, supplier payment terms, and the cash conversion cycle confirm that Sheng Siong moves goods through the system more efficiently as it scales, or is the strong cash generation driven by something else?

Gross margin durability and sourcing resilience. Is the 480-basis-point expansion structural procurement, direct-sourcing, and mix improvement, or a stretch of benign imported-input costs, and does the sourcing engine hold up against currency and supply-chain shocks?

The economics of the Sungei Kadut build. Does the S$520 million distribution centre earn an adequate return on the cash and debt it will absorb, is it the best use of the S$461 million reserve, and how much does its depreciation load reset the margin structure once live?50

The physical-first model versus online fulfilment. Amazon Fresh is exiting Singapore in 2026, which supports the caution, yet RedMart and FairPrice online stay entrenched: is Sheng Siong's roughly 1% online mix economic discipline, or could shifting fulfilment habits slowly weaken the neighbourhood-store advantage?51

The compounding question and the pricing question are now the same one: can a business the market already treats as a premium defensive compounder keep compounding fast enough to deserve that treatment?

That turns on whether the operating system is genuinely self-reinforcing or simply very well-run.

The analysis to come works it through as a bull and bear case, and by reading what the current price implies, rather than by publishing a single target.

The evidence suggests Sheng Siong runs one of the most disciplined grocery operations in the region today. The better question is whether that discipline is a widening moat, or a standard the market now assumes will hold, at a price that leaves little room if it slips.

First Principles Analysis coming this September

Footnotes:

Footnotes (51)

Share price and market capitalisation as of late June 2026 per SGX market data (OV8.SI trading around S$3.20 to S$3.30 on approximately 1.50 billion shares, market capitalisation approximately S$4.8 to S$5.0 billion; Simply Wall St stock report shows S$5.0 billion). The shares traded in a 52-week range of approximately S$1.86 to S$3.28.

Sheng Siong Group Ltd 1Q FY2026 Business Update, 29 April 2026 ("1Q FY2026 Update"). Stores as of 31 March 2026: 87 Singapore and 6 China. Singapore retail area 759,961 sq ft.

Housing and Development Board, Singapore. Approximately 80% of Singapore's resident population lives in HDB public housing.

AGM Minutes, Fifteenth Annual General Meeting, 29 April 2026 ("AGM Minutes"), Appendix A, Response to Question 5: Sheng Siong Online contributes approximately 1% of revenue and is modestly profitable.

Fiscal.ai, Sheng Siong Group Ltd OV8, Revenue chart, and reported FY2025 results. Total Revenues FY2016 S$796.7 million; FY2025 S$1,570 million; FY2024 S$1,428.7 million. FY2025 growth 9.9%. Period CAGR approximately 8.0%.

1Q FY2026 Update, Performance Review. Revenue 1Q FY2026 S$452,802 thousand, up 12.4% year-on-year, "mainly driven by the twelve new stores opened in FY2025."

1Q FY2026 Update, Foreign Operations, China: "China operations accounted for 2.1% of total revenue in 1Q FY2026 and achieved a breakeven result for the quarter."

AGM Minutes. Lim Hock Eng, Executive Director and Executive Chairman; Lim Hock Chee, Executive Director and Chief Executive Officer, re-elected under Resolution 3. Company founded 1985.

NTUC FairPrice Co-operative, established 22 July 1973 by the National Trades Union Congress with a social mission to moderate the cost of living through affordable essentials; Singapore's largest grocery retailer. Singapore's grocery market is dominated by three chains: NTUC FairPrice, DFI Retail Group (Cold Storage and Giant), and Sheng Siong. Sources: NTUC FairPrice corporate history; National Library Board Singapore; industry market overviews.

National Library Board Singapore, "Sheng Siong"; Sheng Siong corporate history. The Lim brothers helped at their father's Punggol pig farm; amid a pig oversupply and the government's phase-out of pig farming, Lim Hock Chee and his wife ran a pork counter at a Savewell provision store in Ang Mo Kio, then bought the failing outlet in 1985 with seed capital from their father to open the first Sheng Siong store.

National Library Board Singapore, "Sheng Siong"; The Straits Times (2008), founder Lim Hock Chee on running the business to maximise profit per square foot of retail space so costs can be cut and prices kept low. The first store focused on a wide range of no-frills products sold at lower profit margins and higher volume.

National Library Board Singapore and Sheng Siong corporate history. The third store, in Woodlands (1995), was the first to feature a wet-market-style fresh section within a supermarket, establishing the "wet and dry" format that competed with traditional wet markets on convenience and price.

Mothership.sg (2023), interview with FairPrice Group leadership identifying Sheng Siong as its biggest competitor and describing dedicated stores set up to compete with Sheng Siong on price; Sheng Siong cited as the second-largest supermarket chain, having overtaken Cold Storage / CS Fresh.

AGM Q&A FY2024 (Sheng Siong FY2024 AGM Responses, published 23 April 2026), Response to Question 7: "Yes, the Group's expansion strategy is closely connected with the supply of new flats from the Housing Development Board (HDB)."

AGM Q&A FY2024, Response to Question 9: "The Group acquires property with the primary goal of operating a supermarket business. Currently, new stores supplied by HDB are primarily on a lease-term basis."

Mothership.sg (2023), industry commentary noting that Sheng Siong's pig-farming roots gave the founders an intimate understanding of supply-chain costs, which they translated into stronger procurement and margins.

Direct and diversified sourcing: AGM Q&A FY2024, Response to Question 2 (diversifying and expanding supply sources, strengthening supplier relationships, efficient supply-chain management, and expanding house-brand offerings); 1Q FY2026 Update, Looking Forward (margin improvement sought through better sales mix, stronger fresh-produce contribution, and direct sourcing).

Sheng Siong operates its own warehouse and distribution centre (currently at Mandai Link), giving it direct control over store replenishment, and Singapore's small size keeps distribution distances short. Company disclosures; Sheng Siong SGX announcement on the Sungei Kadut facility, 25 September 2025.

AGM Q&A FY2024, Response to Question 2: house brand products offer "savings of 5-20% versus leading brands in Singapore." Sheng Siong offers over 1,750 products across roughly 25 house brands (company disclosures).

AGM Q&A FY2024, Response to Question 12: "In 2024, we have implemented AI-powered scales for accurate pricing... we are also developing an AI-driven demand forecasting system in collaboration with AI Singapore to enhance inventory management and boost productivity."

AGM Q&A FY2024, Response to Question 6: "The Group's founders, Mr. Lim Hock Eng, Mr. Lim Hock Chee and Mr. Lim Hock Leng, have been drawing the same basic salary since the effective date of their service agreements in 2011."

AGM Q&A FY2024, Response to Question 6: the variable Incentive Bonus makes up a significant portion of total remuneration. AGM Minutes, Response to Question 3: "variable bonuses and dividend payouts would correspond to the Group's overall performance."

Shareholding disclosure (top shareholders): Sheng Siong Holdings Pte. Ltd. holds 29.9% (448,800,000 shares); Lim Hock Eng 8.65% (130,000,000); Lim Hock Leng 6.6% (99,257,693); Lim Hock Chee 6.54% (98,374,100), a combined family stake of approximately 52%. Ownership breakdown: Individual Insiders 22.9%, Private Companies 29.8%, Institutions 11.3%, General Public 35.9%; top 25 holders own 62.83%. Corroborated via Simply Wall St.

Simply Wall St / company announcement: Fan Hongbo re-designated from Financial Controller to Chief Financial Officer effective 1 February 2026.

AGM Minutes. Resolution 3 (re-election of Lim Hock Chee): For 920,092,339 (99.82%), Against 1,683,389 (0.18%). Introduction: Lim Hock Eng absent due to minor illness.

AGM Minutes, Response to Question 6: placement exercise in 2014 for 120,000,000 shares; "the issued share capital has remained unchanged since then."

AGM Q&A FY2024, Response to Question 5: cash reserved "not only for working capital needs but also as its war chest... such as potential acquisition of new stores and strategic investments in supply chain infrastructure like warehouse and distribution space, automation and technology." Cash balance S$461.1 million as of 31 March 2026 (1Q FY2026 Update).

AGM Q&A FY2024, Response to Question 6: SIAS Outstanding CEO Award (Lim Hock Chee, 2024) and Most Transparent Company, Consumer Staples category (SIAS); ranked within the top ten globally, Grocery and Convenience Stores category, Newsweek and Statista World's Most Trustworthy Companies (2024 and 2025).

AGM Minutes, Appendix A, Response to Question 1: "newly opened stores generally require time to mature before contributing meaningfully to earnings growth, while older stores located in mature estates may experience slower growth in the absence of new residential developments."

1Q FY2026 Update, Performance Review: "Comparable same store revenue in Singapore for 1Q FY2026 increased by 3.5%."

1Q FY2026 Update, Selling and Distribution Expenses table. Staff cost increase S$8.8 million; "The Group also raised retail workers' salaries in September 2025 to meet the Progressive Wage Model requirements in the retail sector."

Singapore imports over 90% of its food from more than 170 countries and regions (Singapore Food Agency; industry market overviews).

AGM Q&A FY2024, Response to Question 1: the Group does not export goods and so does not foresee an immediate tariff impact, and will continue monitoring supply-chain risks and diversifying its supply sources. Response to Question 2: value delivered by diversifying supply sources, strengthening supplier relationships, and efficient supply-chain management.

The Mandai Link distribution centre (completed 2011, land area about 25,005 sqm) was designed to support roughly 50 supermarkets; with the network now above 85 stores, analysts estimate it is near practical capacity, which limits opportunistic bulk buying (DBS, October 2025). Sheng Siong SGX announcement, 25 September 2025.

Sheng Siong SGX announcement, 25 September 2025: wholly-owned subsidiary CMM Marketing Management signed a 33-year JTC lease over 61,297 sqm at Sungei Kadut Street 1 (about 2.5x the Mandai Link site) for a new warehouse, distribution centre and headquarters; total estimated outlay approximately S$520 million (including at least S$120 million in plant and machinery, plus land rent, construction, automation and solar), funded by internal cash and borrowings; features multiple temperature-controlled zones, integrated food processing, automated storage and retrieval systems, robotics, and smart inventory management; capacity for at least 120 supermarkets; targeted completion around end-2029 (analyst estimate); existing Mandai Link facility to be divested within about two years of the new site's occupation. 1Q FY2026 Update: additional Sungei Kadut land lease commenced September 2025.

Fiscal.ai, Sheng Siong Group Ltd OV8. Total Revenues FY2016 S$796.7 million; FY2025 S$1,570 million; LTM S$1,619.8 million. Period CAGR approximately 8.0%.

Reported FY2025 results (per Simply Wall St summary of company filing): net income attributable S$149.5 million, up 8.7% on FY2024; net margin approximately 9.5%; EPS S$0.099.

1Q FY2026 Update. Basic and diluted EPS 1Q FY2026 2.87 cents; 1Q FY2025 2.57 cents, up 11.7%.

Fiscal.ai, Sheng Siong Group Ltd OV8, Cash Flow chart. Cash from Operations FY2016 S$78.1 million; FY2025 S$236.6 million. Period CAGR approximately 13.3%.

Fiscal.ai, Cash Flow chart, and 1Q FY2026 Update. Capital Expenditure FY2025 S$20.9 million; 1Q FY2026 purchase of property, plant and equipment S$2.863 million.

1Q FY2026 Update, Statements of Financial Position. Cash and cash equivalents S$461,070 thousand; total equity S$634,606 thousand as of 31 March 2026.

1Q FY2026 Update, Statements of Financial Position: lease liabilities S$117,161 thousand (non-current) and S$45,512 thousand (current), total S$162,673 thousand, with no financial debt lines outside lease liabilities. Fiscal.ai, Image 2: Debt/Equity approximately 0.3x LTM; Current Ratio approximately 1.8x LTM; EBITDA/Interest Expense 36.2x LTM.

Fiscal.ai, Sheng Siong Group Ltd OV8, Returns chart. Return on Invested Capital FY2025 23.8%, LTM 26.8%; Return on Equity FY2025 26.5%, LTM 25.4%; Return on Assets FY2025 14.9%, LTM 15.3%. Total Assets FY2016 S$387.8 million; LTM S$1,074.9 million.

SGX market data and market summaries (Stockopedia, MSN Money, Simply Wall St), late June 2026: share price around S$3.20, up roughly 72% over the prior year to near an all-time high; trailing P/E approximately 31x; trailing dividend yield approximately 2.2%; payout ratio approximately 70%.

AGM Minutes, Appendix A, Response to Question 3: on the new distribution centre, "Debt financing is being considered as part of the Group's prudent capital management strategy to optimise returns while maintaining financial flexibility."

Amazon announced on 7 May 2026 that it would shut its Amazon Fresh grocery delivery service and phase out local fulfilment in Singapore from 6 July 2026, ending grocery partnerships with Little Farms and A.S. Watson, and retreating to a cross-border catalogue on Amazon.sg (Prime and the storefront continue); the stated rationale was that local grocery economics do not work in a dense market where supermarkets sit minutes from most homes. Singapore's grocery delivery market was worth roughly US$1.1 billion in 2024 and continues to grow, with RedMart (Lazada) and NTUC FairPrice among the leading online players. Sources: Singapore technology and business press (May 2026); industry market overviews.

Disclosure: Glavcot Insights and its contributors may hold positions in securities discussed in this article. All content is provided for informational and educational purposes only. Nothing published by Glavcot Insights constitutes investment advice. Readers should conduct their own research and consult qualified financial professionals before making investment decisions.

Glavcot Insights is an independent equity research publication founded by Ryan Gallinera and managed under Glavcot LLP, Singapore.

Where Clarity Meets Conviction

Glavcot Insights is now live. Join the free tier to get new research, updates, and future analysis directly in your inbox. (Check your spam folder if you don't see the confirmation email)

You might also like

Jul 15

Trip.com Group Limited (TCOM): Is Travel Still the Product, or Is the Platform the Asset?

The business itself made intuitive sense. Travel is not a fad. People still want to move, explore, visit family, take holidays, and experience places beyond where they live. The form of travel may change. The human desire behind it is unlikely to disappear.

21 min read

Jul 01

Pan-United Corporation Ltd. (P52.SI): First Principles Analysis

If you're coming from the First Principles Brief, you already know what Pan-United does and why the

31 min read

Jun 21

Zijin Mining Group (2899.HK): Finding Advantage in Difficult Ground

At the surface level, Zijin exists to resolve a physical supply deficit. Decarbonisation, electric vehicles, solar and wind, transmission grids, and the computing infrastructure behind AI all require more copper at a time when the global mining sector has been starved of new supply.

22 min read

Jun 05

Pan-United Corporation Ltd (P52.SI): Concrete Is the Business. The System Around It Might Be the Moat.

There is also a durability argument that I keep returning to. Concrete has not fundamentally changed in a hundred years. You can make it greener, stronger, lighter, smarter to deliver. But the thing itself, a material that hardens into infrastructure, is not going away.

17 min read

May 19

Haidilao (6862.HK): Is Service the Moat, or the Cost?

Haidilao's service quality did not emerge from a training manual. It was built through a specific mechanism: a master-apprentice incentive structure where store managers are compensated not just on their own store's performance, but on the performance of managers they trained