Good process does not remove luck. It reduces the amount of luck required.

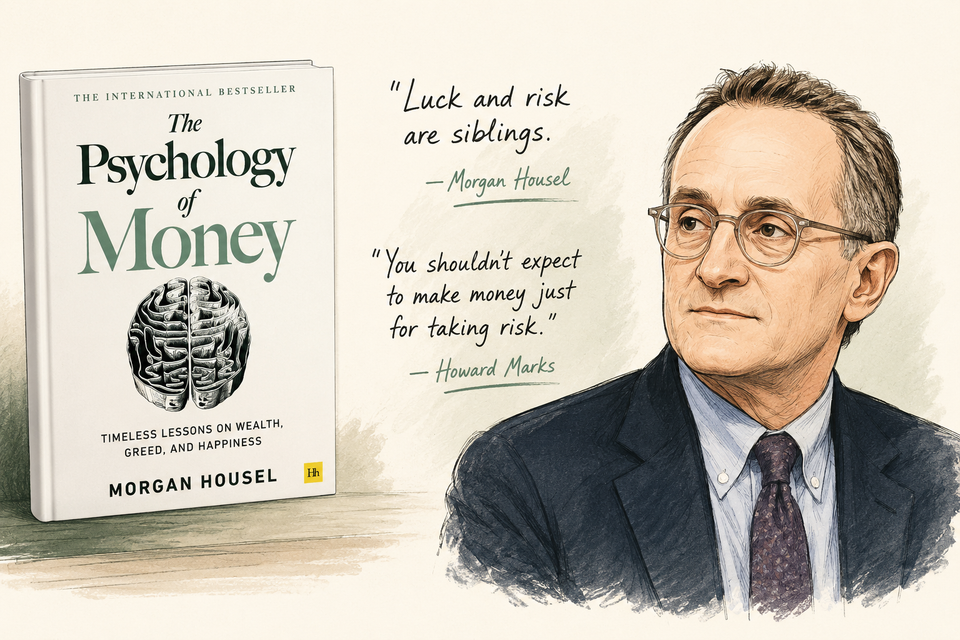

There is a story Morgan Housel tells in The Psychology of Money that has stayed with me longer than most investment ideas I have read.

Bill Gates attended Lakeside School in Seattle. In 1968, Lakeside was one of the only schools in the world with a computer terminal. Gates had access to it at thirteen.

His school friend Kent Evans was on the same trajectory. Same school. Same access. Same intellectual firepower. By most accounts, Evans was the person who would have been Gates' co-founder.

He died in a mountaineering accident before graduating.

Same world. Same starting point. One life cut short by unfortunate circumstance, the other shaped by it.

Housel's point is not that success is random. It is more precise and more uncomfortable: outcomes carry a component that skill and preparation did not earn and cannot fully control. Luck and risk are siblings. They operate on the same axis. We may benefit from one without asking for it. We are exposed to the other without consenting to it.

Most investment writing quietly sidesteps this. The narrative points in the opposite direction: here is the framework, here is the process, here is the outcome it produces. Clean. Causal. Confident.

That architecture is not wrong. It is incomplete.

The Missing Half of "High Risk, High Reward"

We have all heard the phrase. More risk, more reward. It is repeated so often it has stopped sounding like an argument and started sounding like a fact. Take the chance, earn the return. Accept the uncertainty, collect the return.

And often, we forget what sits in the fine print: returns are not guaranteed.

Howard Marks has spent decades dismantling that framing. In his Oaktree memo "The Indispensability of Risk," he writes plainly: "You shouldn't expect to make money without bearing risk, but you shouldn't expect to make money just for taking risk."

The full version of what "high risk" actually means is not a higher reward. It is a wider distribution of outcomes. The upside extends. So does the downside. The possibility of significant loss is not a theoretical caveat appended at the end of a pitch. It is the thing that makes the word "risk" accurate in the first place.

Marks again, from the same memo: "You have to take it to be successful in competitive, high-aspiration arenas. But taking it doesn't mean you'll be successful. That's why they call it risk." Read that twice.

Taking risk is necessary. But it does not complete the equation. The outcome was never promised. The distribution simply widened.

This is what the phrase "high risk, high reward" gets quietly wrong. Not in its logic, but in what it implies. What it implies is that risk and reward travel together in a predictable direction. What is actually true is that risk expands the range of what is possible, in both directions, with no guarantee about which end of that range you land on.

Process Improves the Odds

Put Housel and Marks together and the lesson is not that process is useless. It is that process has to be understood honestly.

Process does not promise an outcome. It improves the conditions under which outcomes unfold. The future is not a controlled experiment. The world does not hold your other variables constant while your thesis plays out. A regulatory reversal. A founder who changes. A macro shock that nobody modeled. These are not always failures of analysis. Sometimes, they are the luck and risk variables doing what they always do.

This does not make process irrelevant. It makes process the only honest lever available.

What process can do is reduce avoidable error. It can separate businesses that are genuinely durable from ones that only look durable. It can identify stewards who allocate capital with minority shareholders in mind versus ones who extract it quietly. It can distinguish a strong financial engine from one that produces good numbers under forgiving conditions and fails under stress.

What process cannot do is compress the distribution to a single point. It cannot eliminate the tail. It cannot substitute for the variable that Housel named honestly and that most investment writing prefers to avoid.

What a Framework Is For

This is where owner-minded analysis matters. Not because it predicts the future better than everyone else, but because it is honest about what it cannot know.

If process improves the odds, then the next question is what kind of process is worth having.

Not every framework reduces risk. Some only organize confidence. Some make the future look neater than it really is. In my opinion, a useful framework should do something more modest and more valuable: improve the quality of the decisions we make under uncertainty.

That is how I think about the Three Pillars.

The Moat, the Stewards, and the Engine are not a prediction engine. They are a discipline for reducing avoidable error.

Moat analysis asks whether the business has structural reasons to persist, not just current reasons to perform. Stewards analysis asks whether the people running the business behave like long-term owners, not short-term operators. Engine analysis asks whether the financial structure is robust enough to survive conditions that the base case did not model.

None of this removes luck from the equation. A business with a genuine moat, disciplined stewards, and a strong engine can still be hit by a regulatory change it did not cause, a commodity shock it could not predict, or an outcome that nobody had on their scenario list.

What the framework does is reduce the number of things that need to go right.

That distinction is not small. Over a long investment horizon, the compounding effect of reduced fragility matters substantially. Not because it guarantees outcomes. Because it reduces the frequency and severity of the errors that permanently impair capital.

A fragile business needs luck to survive. A durable one needs less of it.

We Can Be Our Own Nemesis

The investors I have come to respect share a common trait. They are reflective. They can look at an outcome, good or bad, and ask honestly what they actually controlled and what they did not.

That sounds simple. It is not.

The most dangerous investor is not the one who admits uncertainty.

It is the one who mistakes a good outcome for proof of a good process. Or a bad outcome for evidence of a bad one.

Both errors are seductive. A run of successful investments feels like validation. It may be. It may also be a favorable draw from a distribution that included far worse outcomes. A poor result after rigorous analysis feels like the framework failed. It may not have. The framework reduced the probability of failure. It did not eliminate it.

Humility in investing is not a personality trait you are born with. It is something practiced, and often learned through outcomes that did not go as expected.

When outcomes contain a component we did not control, holding any process with open hands becomes part of the discipline. The investor who forgets this tends to overtrade after a loss, overconcentrate after a win, and over-attribute in both directions.

And when that happens, it is not bad luck that breaks the process. It is the investor who does.

Keeping that in check, staying honest about what the outcome did and did not prove, is what allows the process to keep doing its job over time.

Good process does not remove luck.

It reduces the amount of luck required.

- Morgan Housel, The Psychology of Money (Harriman House, 2020), Chapter 2: "Luck and Risk." The Gates and Kent Evans example appears in this chapter. Evans died in a mountaineering accident before graduating from Lakeside School. Housel uses the contrast to illustrate that outcomes are shaped by forces beyond skill and effort.

- Howard Marks, "The Indispensability of Risk," Oaktree Capital Management memo, April 17, 2024. Both quoted passages are drawn from this memo. Marks also quotes Maurice Ashley approvingly on the nature of risk-taking. Available at oaktreecapital.com

Disclosure: This Perspectives piece reflects the author's personal observations and investment philosophy, not investment advice. Glavcot Insights and its contributors may hold positions in securities discussed in this publication. All content is provided for informational and educational purposes only. Nothing published by Glavcot Insights constitutes investment advice. Readers should conduct their own research and consult qualified financial professionals before making investment decisions.

Glavcot Insights is an independent equity research publication founded by Ryan Gallinera and managed under Glavcot LLP, Singapore.