Samudera Shipping Line Ltd. (S56.SI): The shipping company that wins by not losing.

The shipping company that wins by not losing. Samudera Shipping Line compounds through survival—conservative leverage, Indonesian regulatory protection, and the discipline to capture share when overleveraged peers sink.

The shipping company that wins by not losing. Samudera Shipping Line compounds through survival—conservative leverage, Indonesian regulatory protection, and the discipline to capture share when overleveraged peers sink.

The One-Liner

A resilient, regionally focused container shipping operator that survives through financial discipline in a structurally volatile industry. Samudera Shipping Line turns Southeast Asia's archipelago geography and Indonesian cabotage protection into defensive positioning—earning stable returns not through moats, but through conservative leverage, cycle navigation, and the ability to capture market share when overleveraged competitors fail.

Samudera Shipping first surfaced through my Investment Rubric, scoring unusually well on structural quality metrics during that period—notable for a cyclical shipping business and far better than many larger peers. That fundamental strength, combined with its strategic positioning, made it worth a deeper look.

From a thematic perspective, the setup was compelling. Sea transport remains a non-substitutable backbone of global trade; aircraft, rail, and road each have physical or economic limitations that shipping does not. Meanwhile, ongoing port expansions across Southeast Asia, India, and the Middle East signal long-term confidence in maritime volume growth.

Samudera's position at the intersection of these trends—regional feeder networks, intra-Asia trade lanes, and industrial shipping—made it an unusually interesting candidate.

The First Principles Brief

What is the Business?

Samudera Shipping Line is a Singapore-listed regional container shipping operator specializing in feeder and intra-Asia containerized cargo flows, complemented by bulk and tanker services. The company operates a fleet of 36 vessels across trade routes connecting Southeast Asia, the Indian Subcontinent, the Far East, and the Middle East.Unlike businesses built on brand moats or network effects, Samudera operates in a commoditized, rate-dependent industry. What sets it apart is how it manages its fleet: Samudera charters most of its ships instead of owning them, which lets the company quickly adjust capacity when freight rates swing while avoiding the fixed costs that crush overleveraged competitors.

Samudera Shipping Line is not a moat-driven franchise. It is a resilience-engineered operator inside a price-taking industry, succeeding through financial discipline and cycle navigation rather than structural competitive advantage.

Why Does the Business Exist?

Global shipping giants face a "Geometry Problem"—their mega-ships are too large for Southeast Asia's fragmented ports—and Samudera Shipping Line capitalizes by performing the "Efficiency Arbitrage": using smaller vessels to aggregate cargo from archipelago markets and feed it to Singapore's hub.

The Problem: Massive container ships (20,000+ TEU) physically cannot dock at most Southeast Asian archipelago ports due to shallow drafts and inadequate infrastructure. Even where possible, making multiple small port stops destroys their economic model—the detours and port fees outweigh efficiency gains from vessel scale.

The Solution: Samudera performs the "Efficiency Arbitrage." It uses smaller, flexible vessels (1,000–3,000 TEU) to aggregate cargo from regional "spoke" ports and deliver it to Singapore's deep-water "hub" where mega-ships await. As long as Southeast Asia remains an archipelago, this intermediary role is structurally necessary.

Think of Samudera Shipping Line as the postal service for containers in Southeast Asia's island economies. Amazon can efficiently ship a massive truck full of packages to your city's distribution center, but they still need local carriers to deliver individual parcels to scattered residential addresses. Similarly, mega-ships from Maersk or MSC can economically move 20,000 containers to Singapore's deep-water hub, but they can't profitably make dozens of stops at smaller Indonesian or Philippine ports—the detours destroy their cost advantage. Samudera operates the right-sized vessels (1,000-3000 TEU) that collect and distribute cargo between Singapore and these archipelago ports, solving a geometry problem that gets more valuable as global ships grow larger. Indonesia's cabotage laws—requiring domestic routes to use Indonesian-flagged vessels—add a regulatory barrier that locks out global competitors entirely, creating a protected franchise in a market expected to become the world's 4th largest economy by 2050.

How Does It Succeed?

The "Three-Layered Defense"

How does a commodity operator survive in a brutal industry? By building defenses that competitors cannot easily replicate.

Layer A: The "Indonesia Inc." Defense (Regulatory Moat)

Cabotage Law: Indonesia restricts domestic shipping to Indonesian-flagged vessels owned by Indonesian entities.

The Mechanism: Global competitors like Maersk and MSC cannot legally enter the Indonesian domestic market. Samudera, through its relationship with parent PT Samudera Indonesia and local joint ventures (e.g., PT Samudera Shipping Indonesia), holds the "birthright" to operate inside this protected market.

Result: A protected volume base that pure foreign competitors cannot touch—and one that grows as Indonesia becomes the world's 4th largest economy by 2050.

Layer B: The "Fortress Balance Sheet" (Financial Moat)

Counter-Cyclical Survival: Shipping is infamous for bankruptcies. Samudera's first principle is survival over growth.

The Cash Fortress: Holding ~USD 382.6M in cash—comparable to its entire market capitalization—the company eliminates insolvency risk. It operates like "a savings account with a shipping business attached," weathering freight recessions that sink leveraged peers. During the 2016 crisis, this balance sheet strength allowed Samudera to maintain dividends and capture market share while competitors like Hanjin collapsed under USD 5.5B in debt.

Leverage Discipline: Gearing ratio of 0.47x vs. industry distress threshold of 2.0x+. This isn't just conservative—it's a competitive weapon.

Layer C: Vertical Integration (Operational Moat)

The "Price-Maker" Shift: Shipping lines are price-takers—the market sets freight rates. To escape this trap, Samudera is acquiring assets where it becomes a price-maker or controls its own costs:

The Shipyard (Samudera Madura): Instead of paying inflated rates to third-party repair yards during boom times, Samudera fixes its own ships, controlling maintenance costs and ensuring vessel availability during peak seasons.

The Port (Patimban): By investing in the Patimban Port joint venture, Samudera transitions from "tenant" paying port fees to "landlord" collecting them—converting a variable cost into a revenue stream while securing berth access during congestion.

The Strategic Logic: These moves don't eliminate commodity economics—they reduce exposure to them. Each vertical integration captures margin that would otherwise leak to suppliers during boom cycles, while providing cost stability during busts.

Insight: Samudera Shipping Line doesn't win through scale or pricing power—it wins by not losing. The company layers three defenses competitors can't easily replicate: Indonesian cabotage protection that excludes global giants from a market racing toward world's 4th largest economy status; a fortress balance sheet (USD 382.6M cash, 0.47x gearing) that allows it to pay dividends and capture share during crises that bankrupt leveraged peers; and vertical integration into shipyards and ports that transforms commodity cost centers into controlled revenue streams. In an industry famous for bankruptcies, survival itself becomes the moat.

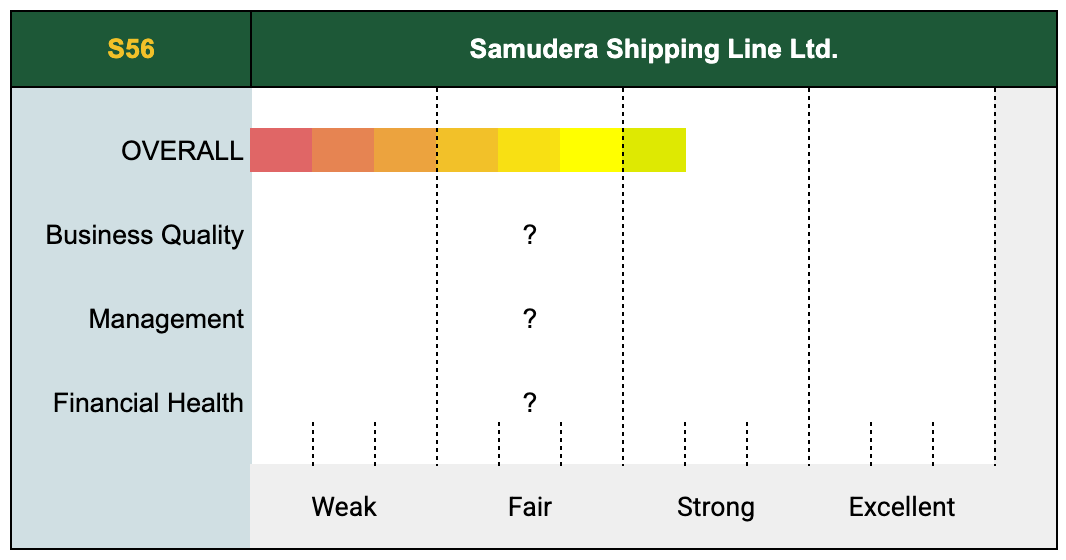

The Glavcot Business Quality Scorecard

Understanding the "?": Our initial assessment points to an Overall Quality of Excellent. But what truly drives this rating? Is it the underlying Business Quality, the Management decisions, or the Financial Health? Unpacking these crucial components requires the deep dive - The Owner’s Analysis.

Summary of Initial Assessment

Samudera Shipping Line is a high-quality, resilient operator in a structurally challenging industry. The business has demonstrated rare survival capability through multiple shipping crises, turning conservative leverage and operational discipline into a defensive moat. Management is excellent—long-term thinkers with proven cycle navigation skills and strong capital allocation track record. The balance sheet is fortress-level with 0.47x gearing.

Here's the concern: this is a commodity business with no pricing power, operating in a brutal boom-bust industry. Returns are solid during good times but compressed during downturns. The 67% parent ownership creates governance constraints that limit strategic flexibility. That said, the parent structure has paradoxically enhanced discipline rather than extracted value—the 5-year track record proves minority shareholder alignment.

Note on Initial Assessment: This summary and Overall score reflect our high-level findings. The final assessment of each pillar (Business Quality, Management Quality, Financial Health) is determined through our comprehensive Owner's Analysis, available exclusively to members after rigorous investigation.

Business Quality & Moat

Survival as Competitive Advantage

Samudera operates in a structurally challenging industry (price-taking, cyclical, capital-intensive), but has demonstrated operational excellence that separates it from failed competitors. In commodity businesses, endurance itself becomes moat—and the evidence is compelling.

The 2016 Crisis: Proof of Resilience

Survival through the 2016 crisis — While Hanjin (world's 7th largest, $5.5 billion in debt) and dozens of regional operators collapsed, Samudera maintained operations and dividend payments.In 2009, the container industry posted operating losses of ~$20 billion, yet Samudera navigated multiple downturns without restructuring.

Network density in growing markets — The company operates 31 services covering India, Bangladesh, Sri Lanka, Pakistan, UAE, Saudi Arabia, Jordan, Egypt, and Turkey, with frequencies up to 4 sailings per week.This network, built over decades, creates operational expertise and customer relationships that cannot be easily replicated.

Operational Flexibility

Operational flexibility — The asset-light, charter-heavy model allows rapid capacity adjustment. During FY2024, management reduced cost of sales by 9.3% while maintaining service quality.

Competitive Positioning

Among regional container operators, Samudera stands in the top quartile for balance sheet strength (gearing 0.47x vs. industry distressed threshold >2.0x), dividend consistency, and management discipline (avoided overleveraging during 2021-2022 boom).

The nuance: This isn't a "great" business by absolute standards—it lacks pricing power and operates with commodity economics. But relative to its industry context, Samudera has built a resilient operation through discipline, relationships, and financial strength that compounds over decades.

Management Quality

Management is led by Bani Maulana Mulia, appointed Group CEO on 1 September 2020, also President Director of PT Samudera Indonesia. With over two decades in shipping, ports, and logistics, he began as a finance officer in Samudera Indonesia in 2001.

Evidence of Disciplined Decision-Making

Fleet strategy during boom (2021-2023) — Avoided overleveraging when competitors ordered expensive newbuilds at peak prices. Maintained balanced owned/leased mix rather than committing to long-term vessel obligations. Result: Positioned to reduce costs when rates normalized, while overleveraged competitors faced distress.

Cost discipline through normalization (2024) — Cost of sales fell 9.3% despite maintaining service capacity.Gross profit margin protected at 19.2% (FY2024) vs 18.7% (FY2023). Demonstrated ability to flex charter commitments and slot purchases.

Capital allocation excellence — Board proposed special dividend of 5.8 Singapore cents plus final dividend of 1.0 cent, bringing total FY2024 dividend to 7.8 cents (44% payout ratio). Dividend maintained across cycles: 0.30 SGD¢ (2020 crisis), 25.0 SGD¢ (2022 boom), 7.8 SGD¢ (2024 normalization). This consistency demonstrates commitment to shareholder returns while maintaining financial strength.

Opportunistic expansion — Launched two new services in 2024 connecting Gulf region and India to Mediterranean during Red Sea crisis.Logistics subsidiary in Jakarta grew from 3 to 7 warehouse sites in FY2024. Took delivery of two container newbuilds in August and December 2024 when asset prices normalized.

The Parent Structure as Discipline Mechanism — While 67% ownership by PT Samudera Indonesia creates governance questions, it has paradoxically reinforced discipline rather than extracted value. The parent provides strategic stability, patient capital during downturns, regional relationships, and prevention of empire-building that destroyed competitors like Hanjin.

Comparative Context

Management avoided strategic errors that bankrupted major competitors. Hanjin over-leveraged with long-term charter commitments at high rates and collapsed when markets turned. Hyundai Merchant Marine posted $556M operating loss in 9 months of 2016, requiring debt-for-equity restructuring.Dozens of regional operators exited during 2016 crisis; most lacked balance sheet discipline to survive.

Management has demonstrated rare long-term thinking in a short-term industry, with concrete evidence of cycle discipline, capital allocation skill, and shareholder alignment.

Financial Health

Samudera maintains the strongest financial profile among regional container shipping operators, with metrics positioning it in the top tier globally for its segment.

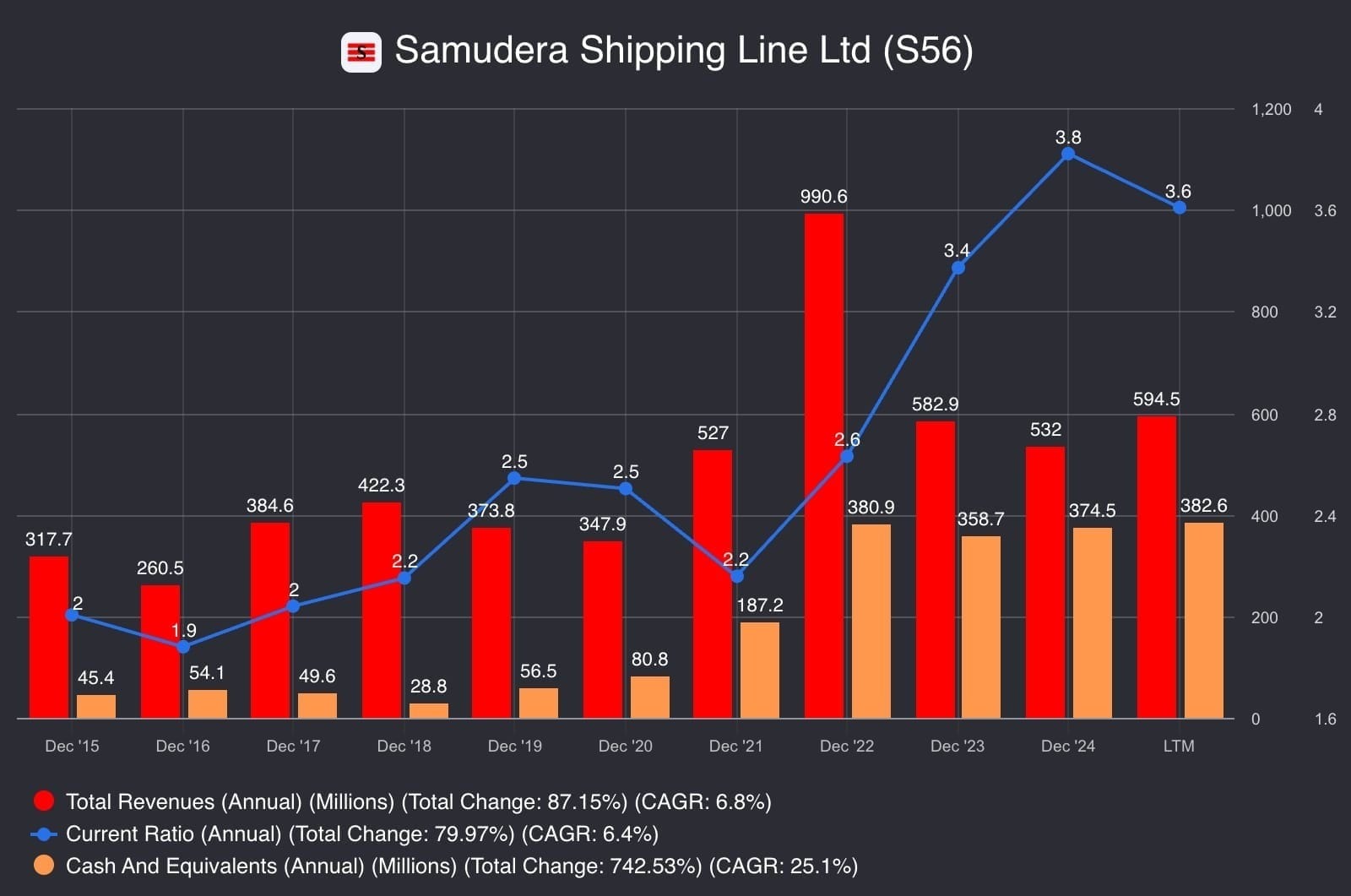

The Revenue and Profitability Story

Chart 1 shows Samudera Shipping Line's journey through shipping's brutal cycles. Revenue peaked at USD 990.6M in 2022 during the post-pandemic boom, then normalized to USD 594.5M (LTM Q2 2025)—demonstrating the inherent volatility of commodity shipping.

Chart 1

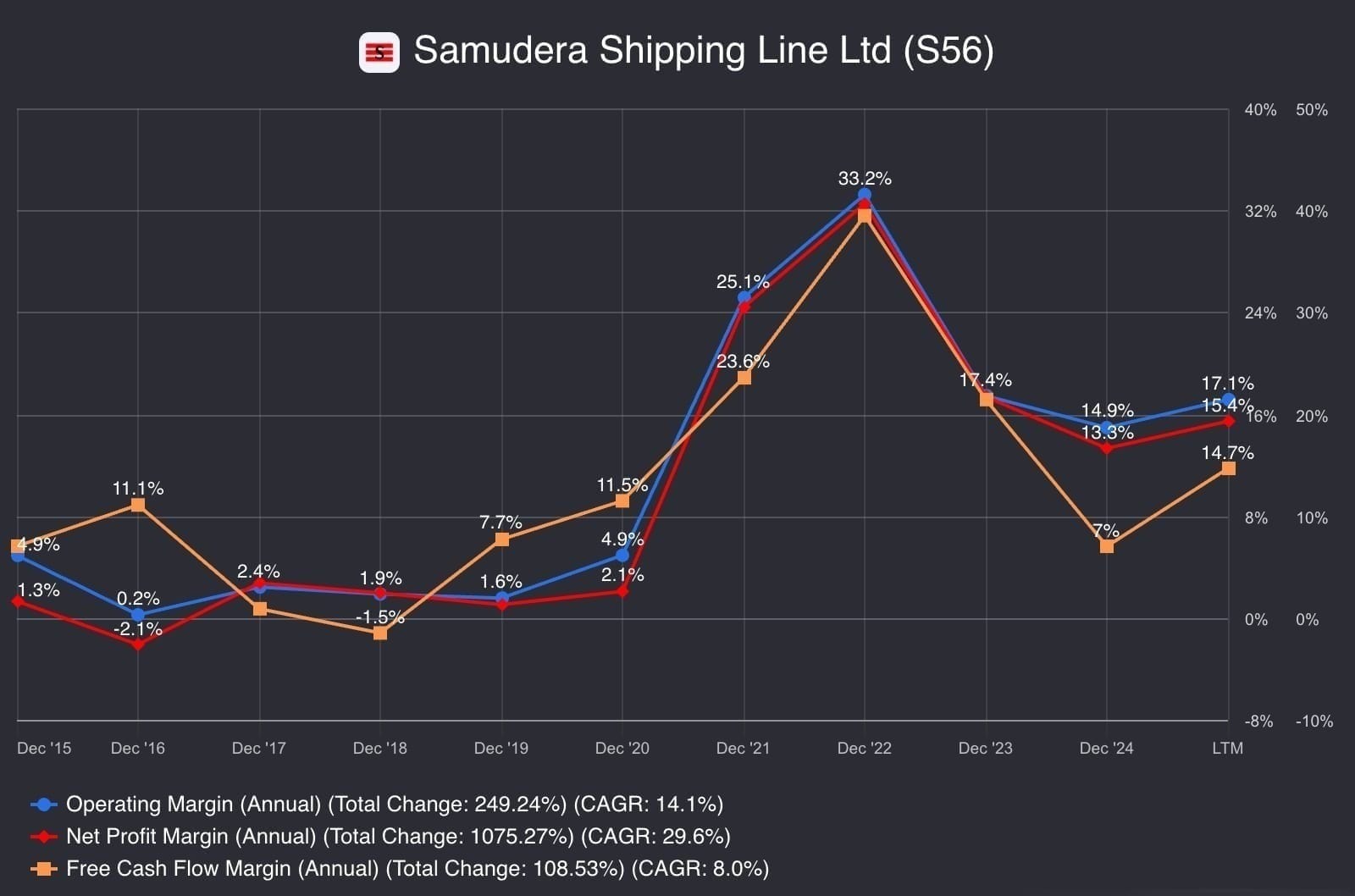

But here's the critical insight: net profit margins tell the survival story. The company maintained profitability even during the 2016 crisis (4.2% margin) when dozens of competitors collapsed. During the 2022 boom, margins exploded to 32.5%, proving the business can generate outsized returns when rates are favorable. As of LTM Q2 2025, margins have normalized to 15.4%—still healthy and demonstrating pricing discipline.

Operating Leverage Finally Kicking In

Chart 2 reveals the operating leverage story. Operating margins have improved from near-zero in 2015-2020 (averaging ~2%) to 17.1% (LTM Q2 2025). This isn't just boom-time luck—it's structural improvement in cost management and operational efficiency.

Chart 2

The FCF margin compression from 33.2% (2022) to 14.7% (LTM Q2 2025) reflects working capital investment during normalization, not distress. Free cash flow remains positive and healthy at this normalized level.

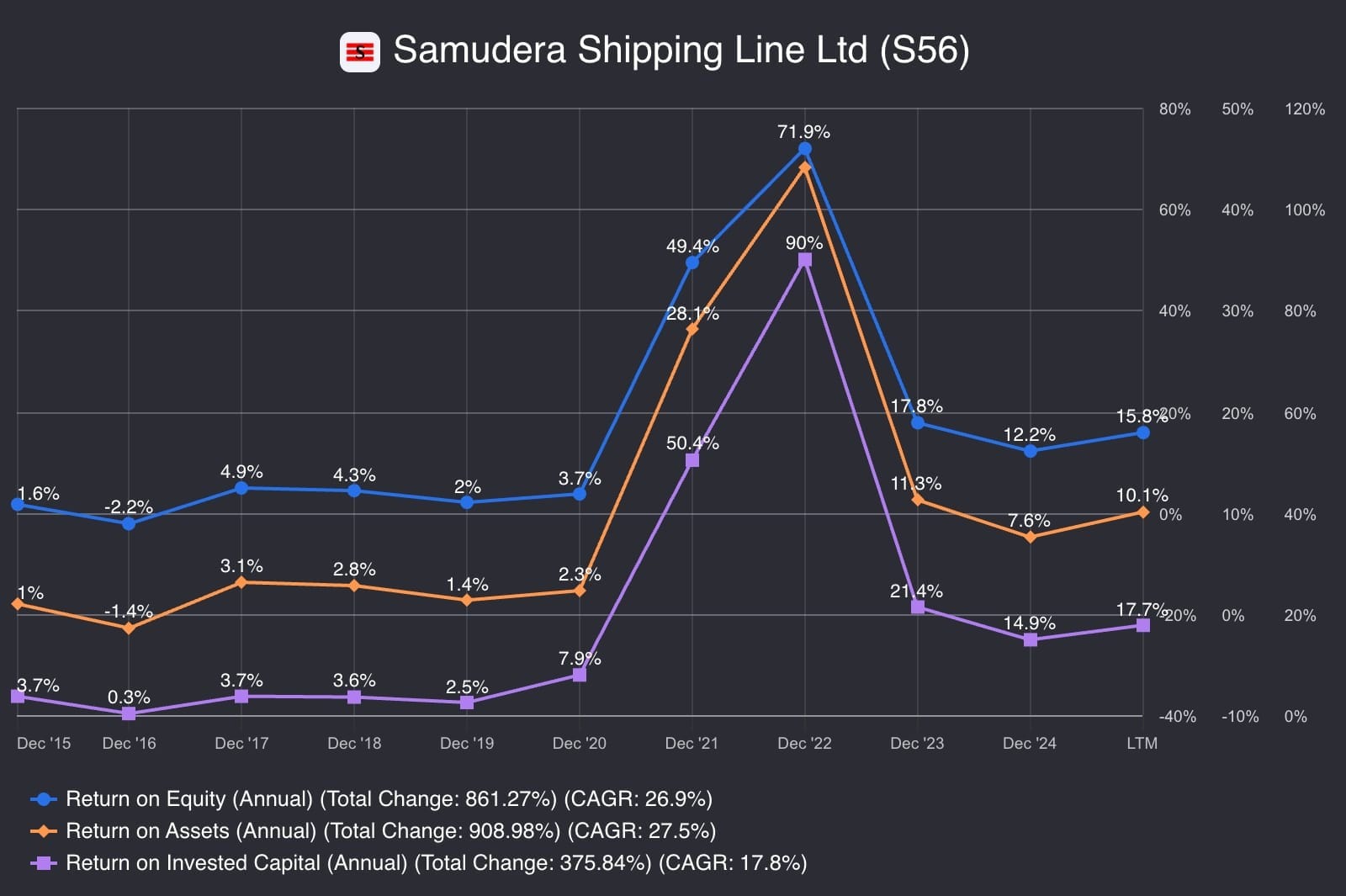

Returns on Capital: Cyclical but Resilient

Chart 3 shows the boom-bust reality of shipping economics. ROE peaked at 71.9% (2022) and has normalized to 15.8% (LTM Q2 2025). ROA and ROIC follow similar patterns.

The key observation: Even in down years (2015-2020), Samudera Shipping Line maintained positive returns while competitors posted massive losses. The current 15.8% ROE at normalized rates demonstrates the business can generate acceptable returns across the cycle.

Liquidity Fortress

Current ratio: 3.6x (LTM Q2 2025), consistently above 2.5x since 2020—providing substantial cushion against multi-year downturns.

Leverage Discipline

Gearing ratio: Consistently maintained between 0.34x-0.50x over the past decade.

Industry context: Healthy operators run 0.6-1.0x; distressed operators exceed 2.0x. Samudera operates well below even "healthy" thresholds, providing maximum financial flexibility.

Shareholder Returns Through Cycles

Dividend consistency: Maintained across all cycles—0.30 SGD¢ (2020 crisis), 25.0 SGD¢ (2022 boom), 7.8 SGD¢ (2024 normalization). Payout ratio sustained at ~44% in both boom and normalization years.

The Critical Insight:In commodity industries with severe cyclicality, balance sheet strength is the primary determinant of long-term survival and value creation. Samudera's financial position enables it to maintain operations when competitors cut capacity, capture market share from distressed exits, sustain dividends through downturns, and invest opportunistically when asset prices collapse.

Historical Validation

During the 2016 shipping crisis when Hanjin collapsed with $5.5B debt and HMM required bailout, Samudera Shipping Line maintained uninterrupted operations, sustained dividend payments, preserved balance sheet strength, and emerged with enhanced competitive position.

Among regional shipping operators globally, Samudera Shipping Line ranks in the top quartile for financial strength and resilience.

Structural Autonomy: The Parent Question

The 67% parent ownership by PT Samudera Indonesia creates a complex structure requiring nuanced assessment—it's neither purely constraining nor purely beneficial.

The Parent Structure: Constraints vs. Benefits

Limiting Aspects — The parent structure creates real strategic constraints. PT Samudera Indonesia ultimately controls major decisions including expansion into new geographies, transformative M&A opportunities, and capital structure changes. While the current 44% dividend payout ratio is shareholder-friendly, parent priorities ultimately shape capital allocation decisions. The structure may also limit addressable markets where direct competition with parent operations could occur.

Protective Aspects — Paradoxically, the parent structure has enhanced operational discipline rather than extracted value. It has prevented the empire-building and over-leveraging that destroyed competitors like Hanjin ($5.5B debt) and crippled HMM. The 67% stake provides long-term strategic patience without quarterly earnings pressure, resistance to value-destroying M&A, and immunity from activist pressure for high-risk strategies. During the 2016 crisis when banks withdrew from shipping, the parent provided capital stability without forced asset sales. The relationship also delivers tangible advantages: backhaul cargo for Indonesia-Singapore routes, regional government relationships critical for port access, access to Indonesian cabotage-protected domestic shipping, and management talent sharing.

Evidence of Alignment — The 5-year track record demonstrates alignment over extraction: consistent dividend policy across cycles (2020-2024), prudent capital allocation that avoided boom-year overleveraging, no value extraction via related-party transactions beyond normal business dealings, and professional management with long-term skin in the game.

The Investment Implication: This is controlled, not captive. For investors seeking explosive growth or transformative strategic optionality, this structure is a genuine ceiling. For those seeking steady compounding with defensive characteristics, it's a feature, not a bug. The 5-year evidence shows the parent has enhanced minority shareholder value creation rather than undermined it.

Conclusion: The Owner's Dilemma

If you're considering Samudera as a long-term holding, you're not buying a classic "moat compounder." You're buying one of the most disciplined, cycle-tested operators in a structurally volatile, price-taking industry.

The core tension is simple:

You're trading durable balance sheet strength and disciplined execution for exposure to an industry with no true pricing power, high capital intensity, and a controlling parent that caps strategic ambition.

The question isn't "Can Samudera become a different kind of business?" It's "Can this kind of business endure, compound, and keep paying you while others fail?"

In short, what are we really watching? ...Whether cycle discipline and balance sheet strength keep translating into steady dividends and opportunistic expansion. ...Whether fleet renewal and regulatory adaptation stay ahead of IMO and carbon constraints ...Whether the parent-controlled structure continues to protect rather than extract value over the next decade

The Questions You Should Be Asking

Can Samudera maintain dividends through the next downcycle without sacrificing fleet renewal? Can the company's fleet handle stricter environmental regulations, or will compliance costs permanently squeeze margins? Will the parent's 67% stake continue protecting minority shareholders—or shift toward value extraction? And what would make you sell: dividend cuts, rising leverage, or governance red flags?

The upside is steady cash returns and quiet compounding as capacity consolidates to survivors.

The risk is that industry structure, regulation, or governance shift just enough that discipline is no longer sufficient to protect returns.

Understanding where you stand on that trade-off determines whether Samudera deserves a place in your portfolio—and at what size.

Samudera Shipping Line is a high-quality, resilient operator in a structurally challenging industry. It succeeds not through moats or competitive advantages, but through superior execution, financial discipline, and the ability to survive and capture market share when competitors fail.

The stakes are clear, but the devil is in the details. Our comprehensive members-only analysis dissects the unit economics behind each business segment, maps out the competitive threats that could derail this turnaround, and reveals whether management's capital allocation track record justifies your trust. This is where conviction gets built—or where you discover the red flags hiding in plain sight.

Disclosure: As of the date of publication, the author holds a long position in the following securities mentioned: Samudera Shipping Line Ltd. (S56) The author has no plans to initiate or alter a position in any of the securities mentioned within 72 hours of publication.*

Where Clarity Meets Conviction

Glavcot Insights is now live. Join the free tier to get new research, updates, and future analysis directly in your inbox. (Check your spam folder if you don't see the confirmation email)

You might also like

Feb 26

NetEase: The Artisan's Engine in a Platform World

The way I see it, digital gaming has become what coffee is to the modern professional: a near-daily ritual, recession-resistant, and remarkably sticky. In idle moments, in downtime, in the spaces between — people reach for it. The market is enormous. The question is who's capturing it.

6 min read

Jan 05

Samudera Shipping Line Ltd. (S56): The Owner's Analysis

Samudera Shipping Line operates at the intersection of structural advantage and cyclical volatility. This analysis examines whether the company's Three-Layered Defense—cabotage protection, niche regional focus, and vertical integration—creates a sustainable moat

21 min read

Jan 01

TAYLOR SWIFT: THE ECONOMICS OF OVER-SERVING

"It is our job to make this look accidental, and it is our job to make this look effortless. I don't think of this as the pieces falling into place. You PUT the pieces where they are."

— Taylor Swift to her dancers and co-performers,The Eras Tour (Taylor's Version) documentary

That stopped me.

8 min read

Dec 22

Samduera Shipping Line: Snapshot

3 min read

Dec 07

The Hour Glass Limited (AGS.SI): Gatekeepers of Time — How a Family Retailer Built a Luxury Moat Piece by Piece

A family-owned gatekeeper to the world's most exclusive timepieces across Asia-Pacific — holding authorized dealer relationships with Swiss luxury brands that most retailers can't access...