The way I see it, digital gaming has become what coffee is to the modern professional: a near-daily ritual, recession-resistant, and remarkably sticky. In idle moments, in downtime, in the spaces between — people reach for it. The market is enormous. The question is who's capturing it.

A few weeks ago, I came across news of a mobile action-MMO called Where Winds Meet. The hype was loud enough that even friends outside the gaming world were talking about it. I watched the gameplay footage and was genuinely struck — not just by the visuals, but by what they represented. A decade ago, an experience like this would have demanded a high-end desktop and hours of setup. Now it lived in someone's pocket.

It pulled me back. I spent years — and more money than I'd care to admit — deep in an MMORPG during my younger days. I knew firsthand how consuming these worlds could be. What I was seeing with Where Winds Meet was that same pull, but more refined, more accessible, and available to an audience ten times the size.

That got me thinking: who builds these things? And more importantly — are they making money?

The way I see it, digital gaming has become what coffee is to the modern professional: a near-daily ritual, recession-resistant, and remarkably sticky. In idle moments, in downtime, in the spaces between — people reach for it. The market is enormous. The question is who's capturing it.

That's when I found NetEase.

The One-Liner

NetEase is China's second-largest game developer — a company that builds and operates its own games, on its own technology, for decades at a time.

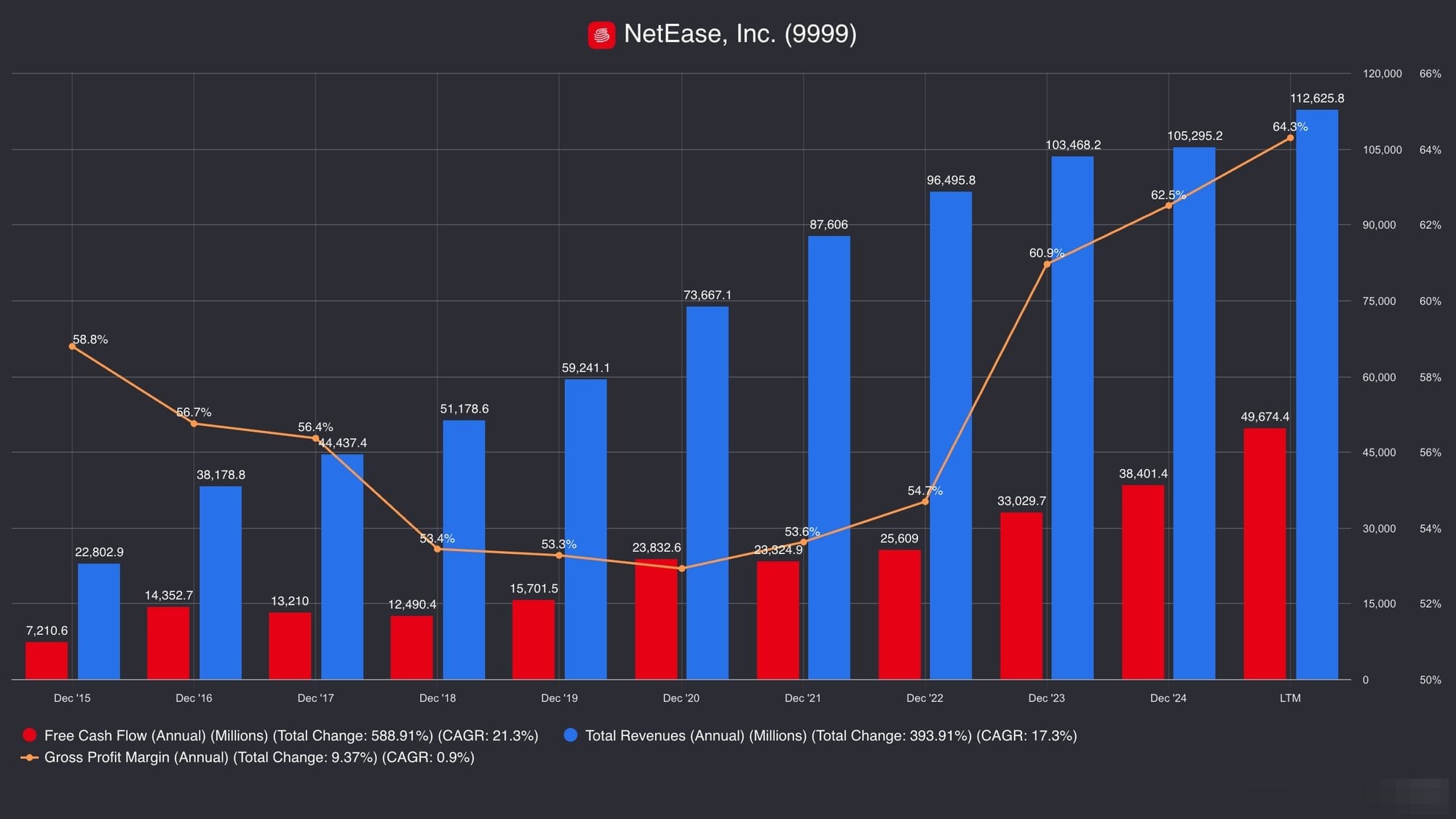

Most businesses with $23.4 billion in net cash, free cash flow conversion above 100%, 64% gross margins, and 20-year-old games still breaking concurrent player records would command a premium valuation. NetEase trades at 15x earnings — a multiple more consistent with a struggling cyclical than a cash-compounding content machine. That disconnect is the paradox. Not whether this is a quality business, but why the market prices it like it isn't. The answer sits in three persistent shadows: regulatory overhang, founder concentration, and a VIE structure that makes legal ownership of the underlying business technically ambiguous. Whether those shadows represent genuine mispricing — or fair compensation for structural risk that simply won't go away — is the question this analysis is built around.

The First Principles Brief

What the Business Does

NetEase is a premium content developer with technical sovereignty. It builds games in-house, runs them on proprietary engines, and monetises them through microtransactions — cosmetics, virtual items, and battle passes — rather than upfront sales. Mobile accounts for roughly 73% of gaming revenue, with PC and console growing as titles like Marvel Rivals and Naraka: Bladepoint gain global traction. 1

The portfolio spans two ends of a spectrum. At one end sit evergreen franchises: Fantasy Westward Journey (launched 2003, 3.58 million peak concurrent players in 2025 2) and Westward Journey Online II (launched 2002, still generating cash flow after 24 years). These aren't legacy holdovers — they function as annuity streams, with deeply embedded player communities built on years of character progression, guild bonds, and social identity. NetEase treats them as living economies, actively managing in-game inflation so virtual assets retain value across decades.

At the other end, NetEase still creates blockbusters. Marvel Rivals drew 10 million players within 72 hours of its December 2024 launch and reached 40 million registered users by February 2025. 3Where Winds Meet accumulated 80 million cumulative players. Eggy Party commands 40 million daily active users in casual gaming.

Beyond games, NetEase operates Youdao (education technology), NetEase Cloud Music (China's #2 music streaming platform), and Yanxuan (e-commerce). But these are peripheral. This is, at its core, a games business — and the investment case is priced accordingly.

Why the Business Exists

NetEase was built on a single conviction: in a digital economy where most content decays, premium proprietary IP compounds.

Founder William Ding refused the binary choice facing most early Chinese internet companies — become a traffic aggregator or a licensed distributor of foreign content. Instead, since 1997, NetEase has operated on what it calls the Self-Development Mandate: own the IP, own the engine, own the relationship with the player. 4

The customer insight driving this is precise. Players don't buy games — they buy emotional and social outcomes: mastery, belonging, status, escape. In live-service models, they're buying an ongoing relationship with a world that evolves around them. NetEase's business exists to build those worlds and sustain them — not for a product cycle, but for a generation.

Two macro conditions make this viable. China is one of the world's largest game markets, with domestic sales surpassing RMB 325 billion in 2024. 5 And Chinese-developed content is increasingly competitive globally, with production values and live-operations infrastructure that travel across borders. The structural constraint — and it's permanent — is regulatory. Chinese authorities can and do alter access and monetisation rules. Minor playtime restrictions remain in force. That friction is baked into every valuation discussion about this company.

How the Business Succeeds

NetEase makes money by converting player attention into recurring digital spending — and doing so at margins that most entertainment businesses cannot match.

Self-developed titles carry gross margins of 67–70%, versus significantly lower margins on licensed games. 6 The Blizzard partnership — restored in 2024 after a 14-month hiatus, bringing back World of Warcraft, Hearthstone, and Overwatch 2 — boosted revenue but compressed margins through revenue-sharing arrangements. That trade-off is instructive: licensed Western IP provides stable cash flow, but self-developed content captures the full value chain.

The economics work because of three compounding advantages. First, switching costs: a player who has spent years building characters and guild relationships in Fantasy Westward Journey faces enormous friction leaving — which is why the franchise still tops revenue charts two decades on. Second, cost structure: Chinese developer compensation runs substantially below Western equivalents, meaning NetEase can produce titles competing head-to-head with global studios at a fraction of the cost. 7 Third, technological leverage: proprietary engines eliminate licensing fees (typically 5% of gross revenue on Unreal) and enable faster iteration across mobile, PC, and console simultaneously.

The result is a business that generates $23.4 billion in net cash, sustains free cash flow conversion above 100%, and returns capital through buybacks and a growing dividend — while trading at 15x earnings. The question isn't whether the machine works. The question is whether the risks surrounding it are permanent features or temporary discounts.

The Machine in Numbers — NetEase Financial Snapshot (2015–LTM)

What I'll Be Looking At

Warren Buffett's test for a great business is deceptively simple: can you describe — with confidence — what it will look like in ten years? For gaming, the broad answer is easy: people will still play. The harder question is who captures that spending, and whether NetEase is structurally positioned to be that company a decade from now.

Beyond the fundamentals covered in the three pillars, there are harder questions that don't show up cleanly in a spreadsheet. Content has to keep winning in an increasingly crowded market. IP and licensing arrangements can unwind quickly — the Blizzard breakup proved that. Distribution is shifting across mobile, PC, console, and platforms that don't exist yet. And the technology underneath it all is moving fast. Gaming may look simple from the outside, but the variables that determine who wins a decade from now tell a different story.

Then there's the China dimension — which deserves its own honest reckoning. Regulatory risk here isn't a tail event. It's a recurring operating condition. And beyond regulation itself, there's the question of how global markets perceive and price Chinese-listed companies — a discount that may or may not be rational, but is very much real.

This analysis works through each of these layers. The goal isn't a price target. It's to understand whether NetEase — as a business, under its current stewards, in its current structure — earns the confidence of a long-term owner.

Is NetEase structurally mispriced — or merely discounted appropriately?

~ This is the opening thesis. ~ The full Owner's Analysis publishes March 2026.

Footnotes

1. NetEase FY2025 Annual Results.

2. NetEase FY2025 Annual Results.

3. NetEase Q4 2024 Earnings Release, February 2025; PC Gamer, "Two days after laying off US-based developers, NetEase says Marvel Rivals has surpassed 40 million players," February 2025.

4. NetEase FY2025 Annual Results; NetEase corporate history, 1997–present.

5. China Audio-Video and Digital Publishing Association (CAADPA), 2024 China Gaming Industry Report, as reported by South China Morning Post, December 2024.

6. NetEase Q4 2024 Earnings Call, February 2025.

7. Naavik, "NetEase's Shifting Global Strategy," 2024.

8. Data and charts Source: Company Filings (Data aggregated using Fiscal.ai)

9. Disclosure: As of the date of publication, the author does not hold a position in the following securities mentioned. The author has no plans to initiate or alter a position in any of the securities mentioned within 72 hours of publication.

Where Clarity Meets Conviction

Glavcot Insights is now live. Join the free tier to get new research, updates, and future analysis directly in your inbox. (Check your spam folder if you don't see the confirmation email)

You might also like

Jan 05

Samudera Shipping Line Ltd. (S56): The Owner's Analysis

Samudera Shipping Line operates at the intersection of structural advantage and cyclical volatility. This analysis examines whether the company's Three-Layered Defense—cabotage protection, niche regional focus, and vertical integration—creates a sustainable moat

21 min read

Jan 01

TAYLOR SWIFT: THE ECONOMICS OF OVER-SERVING

"It is our job to make this look accidental, and it is our job to make this look effortless. I don't think of this as the pieces falling into place. You PUT the pieces where they are."

— Taylor Swift to her dancers and co-performers,The Eras Tour (Taylor's Version) documentary

That stopped me.

8 min read

Dec 07

The Hour Glass Limited (AGS.SI): Gatekeepers of Time — How a Family Retailer Built a Luxury Moat Piece by Piece

A family-owned gatekeeper to the world's most exclusive timepieces across Asia-Pacific — holding authorized dealer relationships with Swiss luxury brands that most retailers can't access...

15 min read

Nov 27

Samudera Shipping Line Ltd. (S56.SI): The shipping company that wins by not losing.

The shipping company that wins by not losing. Samudera Shipping Line compounds through survival—conservative leverage, Indonesian regulatory protection, and the discipline to capture share when overleveraged peers sink.

13 min read

Nov 23

Food Empire Holdings (F03): Fortresses in a Cup-- How Food Empire Built Its Moat One Market at a Time

Food Empire turns everyday coffee habits into long-term compounding — earning in U.S. dollars, operating debt-free, and quietly diversifying its geopolitical risk by replicating its proven fortress-building playbook from Eastern Europe to high-growth Asia.