This report synthesizes financial data and strategic analysis to present a consolidated view of Grab Holdings' transformation. The assessment is structured across three core pillars, an investment rubric, and an analysis of forward-looking trends and risks.

Image courtesy of Grab

This report is part of our Owner’s Analysis series, designed to cut through noise and help you see businesses the way long-term owners do — with clarity, perspective, and a framework for confidence.

Pillar I: Business Quality & Moat (The Fortress)

(Answers: Is this a fundamentally great business that can defend itself against competition?)

Grab’s moat is wide, but still maturing — strong network flywheel, not yet fortress-level.

Grab’s competitive moat is a multi-layered, self-reinforcing system—a "super-app flywheel"—built on network effects, data supremacy, and a hyperlocal technology stack. This ecosystem creates profound cost efficiencies and operational synergies that are inaccessible to single-purpose competitors, forming a durable defense against rivals.

The Super-App Flywheel: The core of Grab's moat is its powerful network effect. With over 46 million monthly transacting users, the platform attracts more drivers and merchants, which leads to better service, which in turn attracts more users, accelerating the cycle. This is an operational reality: in key markets, nearly four out of five of Grab's two-wheel driver-partners accept both ride-hailing and delivery jobs, allowing for optimized driver utilization by smoothing the distinct demand peaks of transport and food delivery.

Data Supremacy: By operating at the intersection of mobility, daily commerce, and financial transactions, Grab compiles a uniquely comprehensive dataset on consumer behavior.[^ How Grab's Localization Strategy Created a Unicorn Valued at $40 Billion | OneSky Blog, accessed on October 27, 2025, https://www.onesky.ai/blog/grabs-localization-strategy] This data is a core strategic asset, fueling machine learning models for personalization and logistics. Most strategically, this data is the bedrock of its financial services ambition; by leveraging its data and AI-driven credit scoring, Grab can offer accessible loans to underserved populations, including drivers and delivery partners who are often invisible to traditional banks.[^ Grab Holdings' Financial Services And Fintech Business Expands In Q2 2025, accessed on October 27, 2025, https://www.crowdfundinsider.com/2025/08/247207-grab-holdings-financial-services-and-fintech-business-expands-in-q2-2025/] This is crucial in a region where approximately 70% of adults lack formal credit histories—a segment traditional banks simply cannot serve profitably.

Hyperlocal Technology: Grab systematically out-executed global giants like Uber through a deeply ingrained hyperlocal strategy. While competitors relied on a standardized global playbook, Grab embraced local necessities from day one, such as accepting cash payments in a region with low credit card penetration and launching motorcycle taxis (GrabBike) to navigate congested city traffic. Its most compelling technological advantage is GrabMaps, a proprietary mapping solution built to navigate Southeast Asia's unique and often poorly documented addresses. This provides more accurate routing with a 4x lower error rate and 10x lower latency than leading third-party providers, creating a structural cost advantage.[^ What You Need to Know About Grab Holdings Limited's Q2 Earnings | AAII, accessed on October 26, 2025, https://www.aaii.com/investingideas/article/284747-what-you-need-to-know-about-grab-holdings-limiteds-q2-earnings]

The Proof: The Path to Profitability

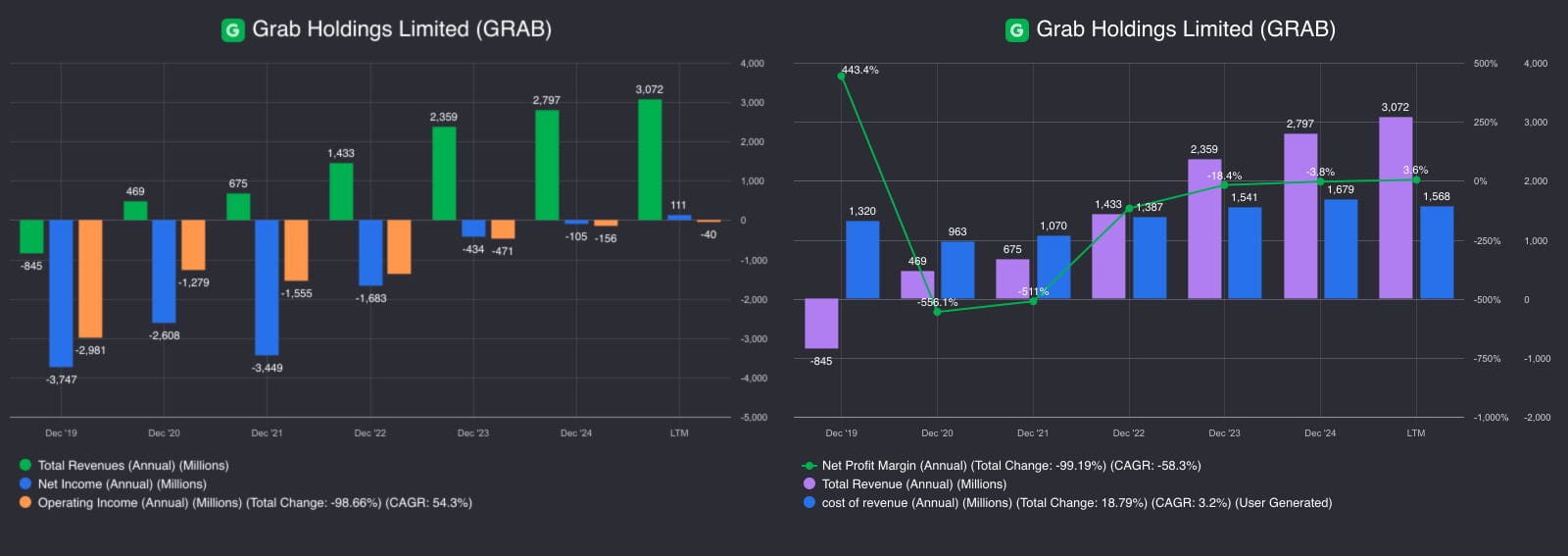

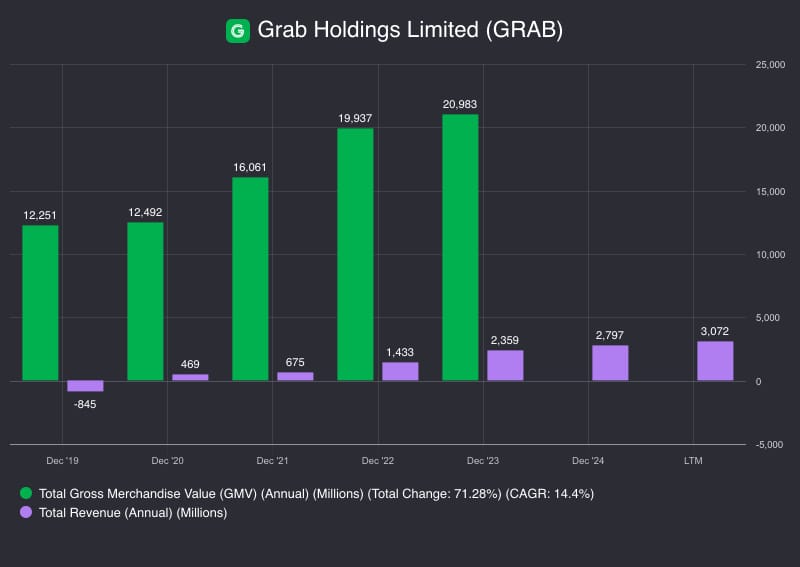

The effectiveness of this moat is not theoretical; it is demonstrated by Grab’s structural shift from a cash-burning startup to a self-sustaining enterprise. This pivot is best visualized in the company's financial trends.

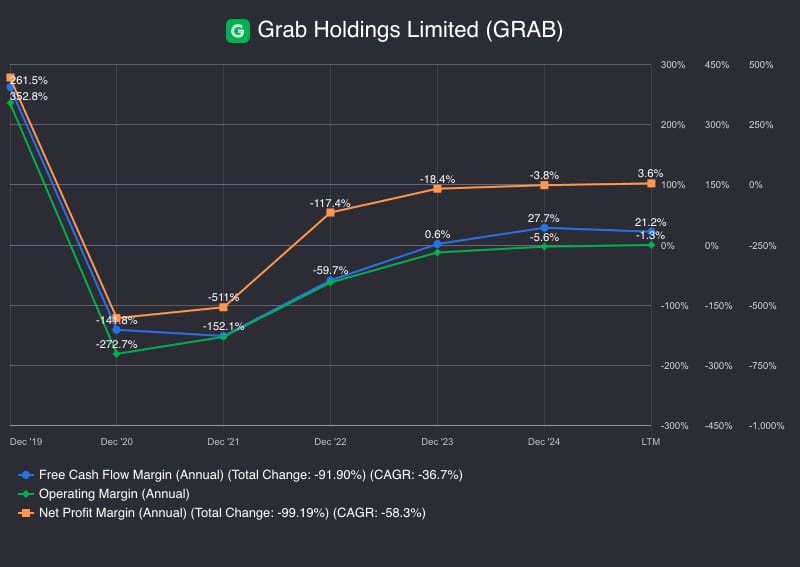

For years, as demonstrated by the financial trends, operating losses dwarfed revenues as the company spent heavily on subsidies to "buy" growth. However, beginning in FY2022, a clear inflection point was reached. The gap between revenue and the cost of revenue began to narrow, culminating in a positive Net Profit Margin of +3.6% in the last twelve months (LTM)—a dramatic reversal from a margin of -556% in 2020. This combination of scaling revenue while bringing losses under control is the classic signature of a business finally achieving operating leverage.

Furthermore, the underlying health of the business is even stronger than net profit suggests. As the next chart illustrates, the Free Cash Flow (FCF) Margin turned positive before the Net Profit Margin and now sits at a robust 21.2% (LTM). This divergence is a critical leading indicator, proving that the company is generating substantial real cash from its operations, well in excess of its accounting profit. This confirms the underlying unit economics are far healthier than the GAAP net income figure would suggest.

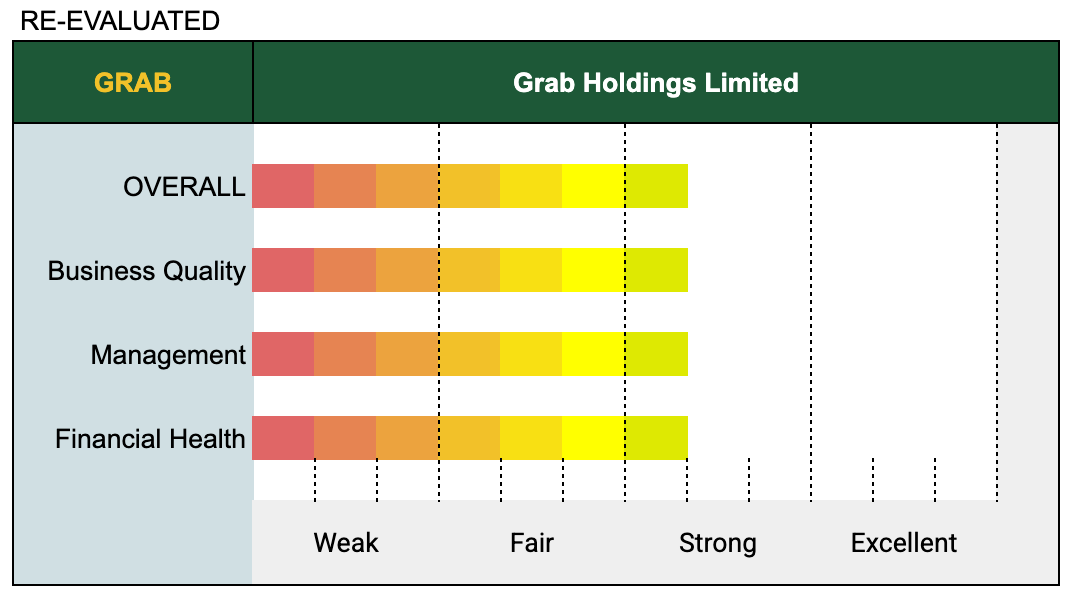

Final Assessment: Strong

Justification: Grab possesses a clear, durable competitive advantage through its powerful network effects, the hallmark of a "Strong" moat. It has demonstrated emerging pricing power by achieving profitability while reducing incentives. While its moat is formidable, it does not yet demonstrate the multiple, reinforcing advantages and dominant profitability metrics (>60% gross margins) of an "Excellent" business.

Pillar II: Management Quality

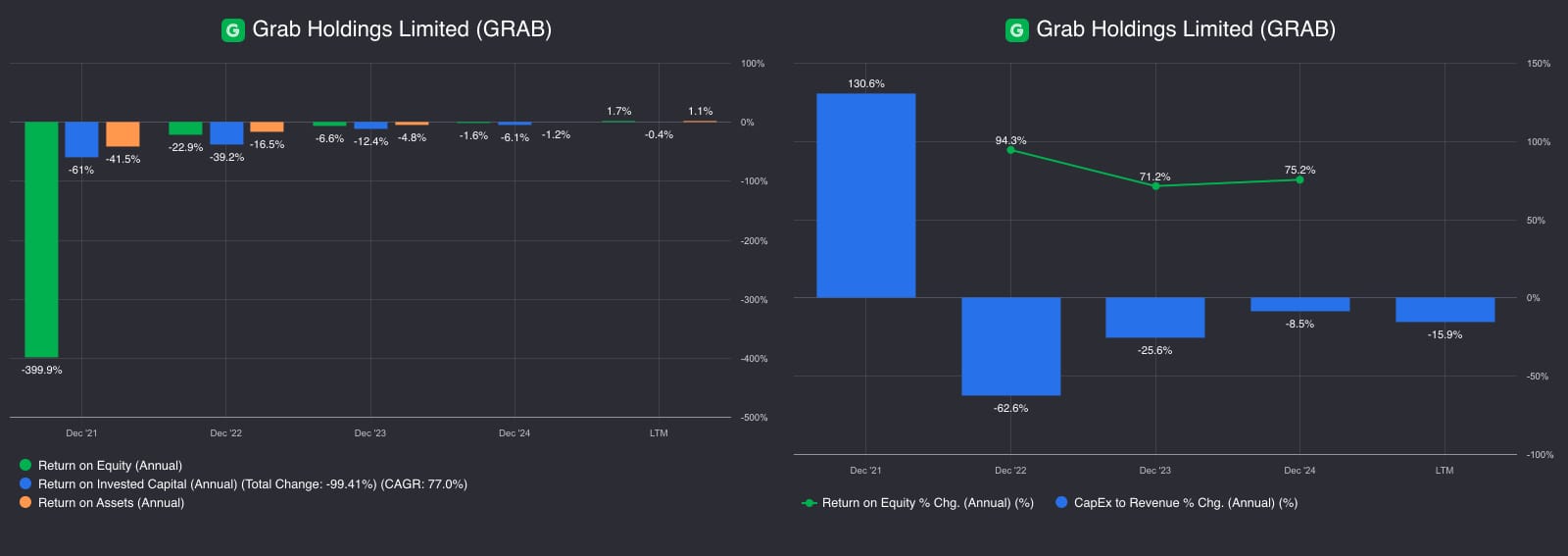

Capital allocation improving; buybacks confirm confidence.

Management quality is best reflected in the company's improving return ratios—a quantitative proxy for decision-making efficiency. During its high-growth expansion phase, returns were heavily negative, with a Return on Invested Capital (ROIC) of -61% in 2021. Since then, the trend shows a steep and decisive normalization toward breakeven and positivity.

This trajectory underscores management’s successful pivot from a "growth-at-all-costs" mindset to disciplined capital allocation and stewardship. This is further evidenced by a declining CapEx-to-Revenue ratio and an active share repurchase program, which signals leadership's confidence that the company's stock is undervalued. As of December 31, 2024, Grab had repurchased $226 million of its shares, followed by another $274 million in the second quarter of 2025 alone.[^ Grab Reports Fourth Quarter and Full Year 2024 Results - Public now, accessed on October 27, 2025]

Takeaway: Grab’s management, under the steady leadership of co-founder and CEO Anthony Tan, has shifted from pursuing growth at any cost to emphasizing disciplined capital stewardship.[^ Tan, Anthony. Profile: Group CEO & Co-Founder of Grab Holdings Ltd. World Economic Forum, 2025. https://www.weforum.org/people/anthony-tan] The rising ROIC trend signals not only stronger reinvestment decisions but also a maturing leadership mindset focused on long-term sustainability and shareholder value.

Justification: The team's performance aligns with the "Good" criteria. The ROIC trend is sharply improving, signaling better capital allocation. The active and significant share repurchase program is a clear, shareholder-friendly action. While a long-term track record of high returns is not yet established (preventing an "Excellent" rating), the strategic pivot and recent actions are rational, credible, and clearly communicated.

Pillar III: Financial Health

A once cash-burning startup now stands on solid footing, with liquidity and leverage ratios signaling genuine financial resilience.

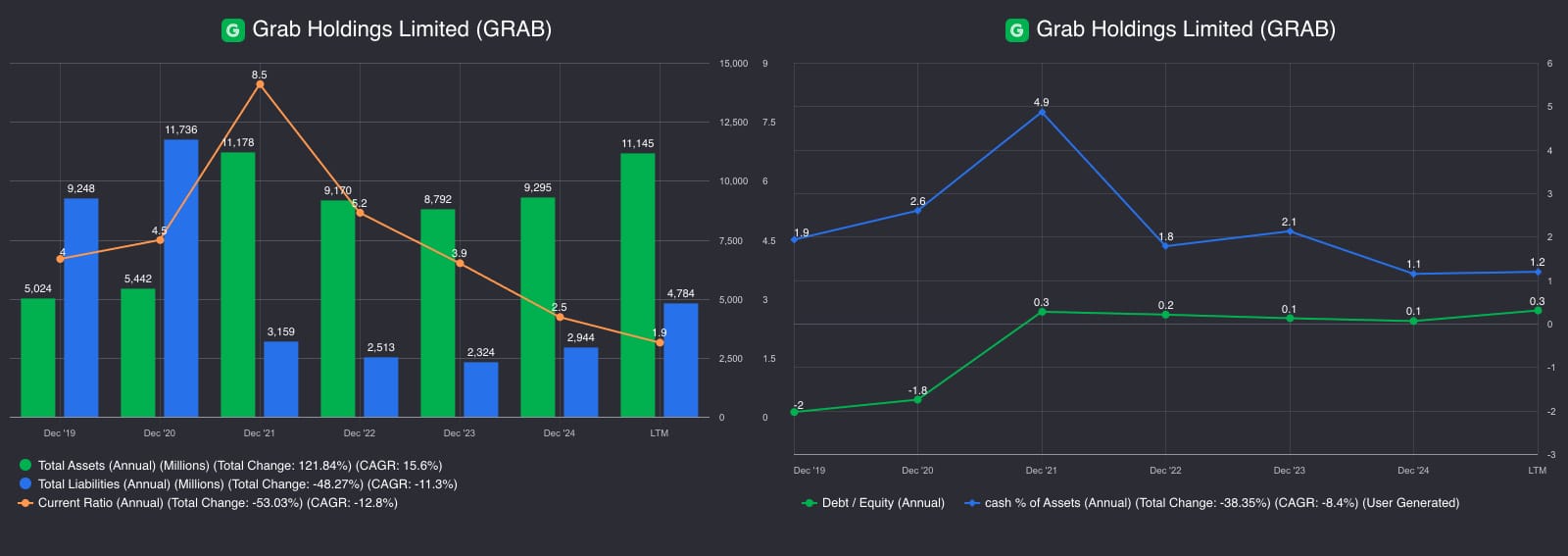

Grab’s balance sheet has undergone a fundamental strengthening, moving from a position of high-risk liquidity dependence to one of financial stability. Since 2019, total assets have more than doubled (+121.8%), while total liabilities have contracted by nearly half (-48.3%).

The company's financial foundation is now stable and characterized by low leverage and strong liquidity. The Current Ratio remains comfortably above the 1.5x threshold at approximately 2.0x, and the Debt-to-Equity ratio has improved to a healthy 0.3x.

Takeaway: The company has moved from being 'funding-dependent' to 'self-financed.' Its financial foundation is now characterized by low leverage, adequate liquidity, and growing asset strength.

Final Assessment: Strong

Key Proof: Assets +121.8% | Liabilities -48.3% | Current Ratio ~2.0× | Debt/Equity: 0.3×

Justification: Grab’s key financial health ratios squarely meet the quantitative criteria for a "Strong" rating. Its liquidity and low leverage demonstrate a robust balance sheet capable of withstanding economic challenges. The "Weak" rating from the earlier report was a backward-looking assessment focused on profitability scars. Today, the forward-looking resilience of the balance sheet is the dominant factor, making the "Strong" rating the correct assessment. It is held back from "Excellent" only by the large accumulated deficit from its history of losses.

Growth Efficiency

Though closely linked to Business Quality, is treated here as its own dimension — it measures how effectively the company’s competitive advantages and management decisions translate into profitable, capital-light growth. This reflects the conversion power of the moat — how well scale turns into shareholder value.

Growth efficiency—how effectively Grab converts platform activity into profitable revenue—is improving markedly. While Gross Merchandise Value (GMV) has grown at a strong 14.4% CAGR since 2019, revenue has grown at a much faster 54.3% CAGR over the same period.

This divergence demonstrates significantly stronger monetization per transaction. Grab’s take rate (Revenue as a percentage of GMV) has expanded from roughly 3.7% to 9.9%, proving that the platform can generate more value from its existing scale. This is complemented by a 22% increase in Revenue per Employee, reflecting greater scaling efficiency.

Takeaway: Grab's growth is now driven by efficiency rather than just scale. Rising take rates and improved revenue per user show that each incremental user or order adds to profitability—a hallmark of a mature, monetizing platform.

Revenue is growing significantly faster than transaction volume (GMV), while take rates continue to strengthen. This demonstrates that Grab is effectively converting its scale into profitable revenue, creating a highly efficient and sustainable growth model.

Notable Trends & Forward-Looking Risks

While the three pillars provide a snapshot of Grab's current health, a forward-looking perspective requires identifying key trends that could accelerate growth and risks that could impede it.

Notable Trends

Market Share Consolidation: The competitive landscape in Southeast Asia is consolidating. In 2023, Grab's food delivery GMV grew by 6.8% while its closest competitors, Foodpanda and Gojek, saw declines of 12.9% and 10% respectively.[^ Food delivery platforms in Southeast Asia 2024 - Momentum Works, accessed on October 27, 2025, https://momentum.asia/product/food-delivery-platforms-in-sea-2024/] With Foodpanda's parent company, Delivery Hero, having explored an exit from the region, Grab has been actively gaining market share.[^ Just Grab It: Grab Holdings | River Valley Asset Management, accessed on October 27, 2025, https://www.rivervalleyasset.com/just-grab-it-grab-holdings/]

Strategic Push into Affordability: Management has explicitly stated a focus on making products more affordable to drive user growth and increase order frequency.[^ Grab raises full-year 2024 core profit forecast as Q1 net loss narrows - The Straits Times, accessed on October 26, 2025, https://www.straitstimes.com/business/grab-raises-full-year-2024-core-profit-forecast-as-q1-net-loss-narrows-to-1546-million] Initiatives like "Saver" deliveries, which offer lower fees for longer wait times, have seen adoption grow to 32% of delivery transactions in Q3 2024.

Investment in Autonomous Technology: Grab is making strategic, long-term investments in autonomous vehicle (AV) technology. The company has partnered with WeRide to deploy robotaxis and is also piloting an autonomous shuttle bus with A2Z in Singapore.[^ Why is Grab exploring autonomous vehicles? - Singapore, accessed on October 27, 2025, https://www.grab.com/sg/inside-grab/stories/autonomous-vehicle-self-driving-southeast-asia-transport/]

Forward-Looking Risks

Persistent Competition and Margin Pressure: Intense competition persists, particularly from GoTo in the critical Indonesian market and low-cost competitors like InDrive and Maxim. A renewed battle for market share could force a return to higher incentive spending, which would directly compress margins.

Execution Risk in Financial Services: The Financial Services segment is a key pillar of the long-term "super-app" strategy but remains a drag on group profitability, posting a Segment Adjusted EBITDA loss of $26 million in Q2 2025. The digital banking operations face a long road to breaking even (forecasted for 2026) and must navigate complex, country-specific regulations and strict capital requirements set by authorities like the Monetary Authority of Singapore (MAS).[^ ANNEX A DIGITAL FULL BANK FRAMEWORK Eligibility Criteria Application for a digital full bank licence is open to companies headq - Monetary Authority of Singapore, accessed on October 27, 2025, https://www.mas.gov.sg/-/media/Annex-A-Digital-Full-Bank-Framework.pdf]

High Valuation and Market Expectations: The market has already priced in much of the successful turnaround. After the Q2 2025 earnings release, the stock dropped over 9% in after-hours trading despite meeting EPS expectations and beating revenue forecasts, signaling that investors demand substantial growth to justify the current premium valuation.[^ Earnings call transcript: GRAB Q2 2025 sees steady EPS, revenue surprise - Investing.com, accessed on October 27, 2025, https://www.investing.com/news/transcripts/earnings-call-transcript-grab-q2-2025-sees-steady-eps-revenue-surprise-93CH-4205128]

2025 Investment Rubric Analysis

The Investment Rubric presented here is designed as a structured guide for evaluating business fundamentals using idealized benchmarks across liquidity, profitability, efficiency, and shareholder alignment.

Important caveat: These "ideal ranges" reflect mature business benchmarks and may not fully apply to growth-stage companies like Grab that prioritize reinvestment over near-term returns. For companies still in early profitability stages, several metrics (such as sustained ROIC >15% or Net Profit Margin >20%) may not yet be applicable. Young or recently public firms often reinvest heavily into scaling operations, technology, and user growth, which can temporarily suppress return ratios or shareholder yield. [^ Source: Company Filings (Data aggregated using Fiscal.ai)]

Readers are therefore encouraged to use this rubric as a framework for perspective, rather than a rigid scoring system. The ranges serve to benchmark directional strength and financial discipline, while recognizing that each business evolves along its own timeline of capital efficiency and maturity.

Ultimately, the goal is to help investors think like owners — to observe trajectory over static scores, and to decide their own comfort levels for what constitutes “ideal” in the context of a company’s stage, risk appetite, and sector dynamics.

Balance Sheet

Ratio/Metric

Ideal Range

GRAB Value (LTM)

Assessment & Notes

Current Ratio

>1.5

~2.0x

✓ PASS. Strong ability to cover short-term obligations.

Debt-to-Equity Ratio

<0.8

0.3x

✓ PASS. Low reliance on debt financing.

Retained Earnings Growth

Upward Trend

Negative

✗ FAIL. History of losses has led to a large accumulated deficit.

Treasury Stock (Buybacks)

Increasing

Yes

✓ PASS. Actively returning capital via share repurchases.

Income Statement

Ratio/Metric

Ideal Range

GRAB Value (LTM)

Assessment & Notes

Gross Profit Margin

>40%

42.0%

✓ PASS. Indicates strong pricing power in core segments.

Net Profit Margin

>20%

3.6%

✗ FAIL (Improving). Recently turned profitable, but well below the ideal range.

SG&A Margin vs. Gross Profit

30%-80%

71.2%

✓ PASS. SG&A expenses are within a reasonable range relative to gross profit.

R&D Margin vs. Gross Profit

<30%

34.9%

✗ FAIL. Heavy, ongoing investment in technology to maintain its moat.

Capital Efficiency

Ratio/Metric

Ideal Range

GRAB Value (LTM)

Assessment & Notes

Return on Equity (ROE)

>15%

1.7%

✗ FAIL. Profitability is not yet sufficient to generate adequate returns on equity.

Return on Invested Capital (ROIC)

>15%

1.1%

✗ FAIL. Returns are positive but still well below the ideal threshold for value creation.

Shareholder Return

Ratio/Metric

Ideal Range

GRAB Value (LTM)

Assessment & Notes

Dividend Yield

>2%

0%

✗ FAIL. Company does not pay a dividend.

Shareholder Yield

>3%

~1.0%

✗ FAIL. Buyback yield is modest and below the ideal threshold.

Latest Updates & Structural Signals (as of Q3 2025)

The most recent financial data further supports the long-term owner’s perspective outlined in this The Owner's Analysis. The story is one of structural normalization, disciplined reinvestment, and gradual strengthening of unit economics.

1. Profitability: The inflection is now durable, not cyclical

Grab’s three core profitability metrics continue a multi-year recovery:

Operating Margin: –95% (2022) → 0.8% LTM

Net Profit Margin: –117% (2022) → 3.8% LTM

Free Cash Flow Margin: –59.7% (2022) → 5.6% LTM

Referring to the latest Q3 2025 figures[^Fiscal.ai latest GRAB figures], the figures indicate an upward trend, showing that the improvements are structurally sustained rather than temporary.

2. Revenue & GMV: Growth is now driven by monetization, not subsidies

Revenue is up to US$3.23B LTM, while GMV has risen to ~US$21B before stabilizing. The pattern is clear:

GMV growth is no longer driven by discounting.

Revenue is growing faster than GMV due to take-rate improvements, better merchant mix, and higher-margin services.

This reinforces Grab’s strategic shift from volume-driven growth to quality-driven monetization.

3. Returns on Capital: Long-term value creation is finally possible

For the first time since listing, returns have turned positive:

ROE: +1.9% LTM

ROA: +1.2% LTM

ROIC: +0.2% LTM

The move from deeply negative ROIC levels (–61% in 2021) to positive territory signals improving capital efficiency and reduced dilution risk.

4. Balance Sheet & Liquidity: Still one of Grab’s strongest advantages

Key improvements include:

Liabilities falling from ~US$11.7B → ~US$4.8B LTM

Current Ratio holding above 1.8

High cash levels relative to assets

Very low Debt/Equity (~0.3 LTM)

Grab’s liquidity position provides management with significant flexibility—reinvesting, acquiring, or navigating downturns without external capital.

5. CapEx Discipline: From build-out to harvest phase

The CapEx data distinguishes two clear eras:

Phase 1 — Build-out (2020–2021)

CapEx-to-Revenue climbed to ~11% in 2021 during ecosystem expansion.

YoY CapEx intensity surged (+130.6% in 2021).

Phase 2 — Normalization (2022 onward)

CapEx-to-Revenue declined to ~3% from 2023 onward and remains at ~2.8% LTM.

YoY CapEx intensity has been negative for three consecutive years.

Together, these figures confirm that Grab is now operating on a stable, asset-light base with predictable reinvestment needs.

Overall Owner’s View

The Q3 2025 financials reinforce the TOA thesis:

Grab is structurally more profitable

Less capital-intensive

Disciplined in reinvestment

More efficient per dollar of GMV

And finally generating positive returns on capital

The long-term owner’s question—“Can Grab sustain profitability once it gets there?”—is increasingly answered by the data:

Yes. The fundamentals now support durable, self-reinforcing profitability.

Conclusion: The Owner's Perspective

Our analysis reveals Grab Holdings at a pivotal moment. The business has built a strong competitive moat, and its super-app flywheel is now translating into a clear and decisive turn towards profitability and strong free cash flow generation. Management has shown commendable discipline in rationalizing costs and allocating capital toward shareholder returns, while the balance sheet has been fortified with low leverage.

However, the journey is not complete. As the investment rubric highlights, while operational metrics impress, true economic value creation hinges on achieving a Return on Invested Capital (ROIC) that consistently exceeds the cost of capital—a threshold Grab is only now approaching. Significant risks persist, notably the intense competition in key markets, regulatory hurdles, and the crucial execution required to transform the Financial Services segment into a high-margin contributor.[^ Commentary: Has Grab hit a turning point in its quest to become profitable? - CNA, accessed on October 26, 2025, https://www.channelnewsasia.com/commentary/grab-profit-growth-merger-goto-ai-southeast-asia-5030266]

The current market sentiment, reflected in a strong consensus of "Buy" ratings from analysts (as of this writing), appears to be pricing in the continued success of this turnaround narrative. Analyst price targets, on average, suggest the stock is trading near its fair value, indicating that much of this optimism is already reflected in the current price.

As a potential owner, you must weigh the bullish consensus against these tangible risks. The question isn't whether Grab has turned around—it has. The question is whether the current price already reflects that success, and whether management can maintain discipline while navigating the competitive pressures and execution challenges ahead.[^Glavcot Insights does not offer buy or sell signals. Our goal is to provide the Clarity (understanding the business mechanics), Perspective (seeing the trends and risks), and analytical Framework (the 4-Pillar and Rubric analysis) needed for you to build your own Confidence. The final decision—whether the current market price offers a sufficient Margin of Safety for the risks involved—rests, as always, with the individual investor acting as a thoughtful owner.][^ Disclosure: As of the date of publication, the author holds a long position in the following securities mentioned: Grab Holdings (GRAB). The author has no plans to initiate or alter a position in any of the securities mentioned within 72 hours of publication.]

Glavcot Take: A rare case of a super-app turning profitable without losing its network edge — strong foundations, but not yet a fortress. Amidst all the financial metrics and strategic layers, if the analysis still feels dense or uncertain, there’s a simpler lens to view it through: even Uber — once Grab’s fiercest rival — now owns about 13.2% of Grab’s shares as of February 2025 [^ https://finance.yahoo.com/news/grab-jumps-48-hold-fold-171200754.html ]. If the company that once fought to dominate this market chose instead to stay invested, perhaps that alone says enough.

Glavcot Business Scorecard

GRAB - Q3 2025

Where Clarity Meets Conviction

Glavcot Insights is now live. Join the free tier to get new research, updates, and future analysis directly in your inbox. (Check your spam folder if you don't see the confirmation email)

You might also like

Feb 26

NetEase: The Artisan's Engine in a Platform World

The way I see it, digital gaming has become what coffee is to the modern professional: a near-daily ritual, recession-resistant, and remarkably sticky. In idle moments, in downtime, in the spaces between — people reach for it. The market is enormous. The question is who's capturing it.

6 min read

Feb 04

The Hour Glass (AGS): The Owner's Analysis

As of February 4, 2026, The Hour Glass share price has risen from approximately S$1.55 to S$2.24—over 40% in twelve months. For a family-controlled business with a 37-year dividend track record operating in a niche corner of luxury retail, this re-rating demands investigation:

35 min read

Jan 05

Samudera Shipping Line Ltd. (S56): The Owner's Analysis

Samudera Shipping Line operates at the intersection of structural advantage and cyclical volatility. This analysis examines whether the company's Three-Layered Defense—cabotage protection, niche regional focus, and vertical integration—creates a sustainable moat

21 min read

Dec 22

Grab Holdings: Snapshot

Grab Holdings Limited

First Principles Brief (GRAB)

"Engineering an Economic Flywheel."

The One-Liner

Southeast Asia's leading

3 min read

Dec 22

What's Coming in 2026: The Owner's Analysis

When we launched in November 2025, First Principles Briefs (FPBs) established our analytical approach.

Two months later, we kept hearing: "This tells me what the company does. Now tell me: what's the case for ownership—and when does it break?"