Grab Holdings Limited (GRAB): Engineering an Economic Flywheel for Southeast Asia

Grab is Southeast Asia's leading "super-app," using its massive ride-hailing and delivery network to build out financial services and business solutions across the region.

Grab is Southeast Asia's leading "super-app," using its massive ride-hailing and delivery network to build out financial services and business solutions across the region.

I often think about how Peter Lynch would discover investment ideas from everyday life — simply by noticing what people actually use. During the pandemic, Grab was one of those things you couldn’t miss. It became a fixture in daily life — moving people, delivering meals, groceries, even essentials when most of Southeast Asia stood still. What’s remarkable is that, even after the pandemic faded, Grab didn’t lose relevance. It evolved — from transport and food delivery into a broader financial and lifestyle platform. That observation made me pause and take a closer look. If a company becomes this embedded in everyday behavior, ...perhaps it’s worth understanding why — and whether that presence can translate into enduring business value.

The First Principles Brief

What is the business?

Think of Grab as a digital middleman that connects everyday people with drivers and restaurants. It's a technology platform running three main businesses: Deliveries (food, groceries, packages), Mobility (ride-hailing like Uber), and Financial Services (digital wallet payments, loans, and insurance through GrabPay).

Why does it exist?

Southeast Asia used to be a mess of unreliable services—sketchy taxis, inconsistent delivery options, you name it. Grab saw an opportunity to create one trusted app that could handle all these daily needs. For customers, it's about convenience. For drivers and merchants, it's a way to make money and grow their business.

Here's a common misconception: People think Grab is just a delivery or ride-booking app. It's not—Grab is fundamentally a technology company. The real value isn't in the drivers or the deliveries themselves; it's in the sophisticated platform technology that powers everything behind the scenes. Grab builds the algorithms that match riders with drivers in real-time, the logistics systems that route deliveries efficiently, the payment infrastructure that processes millions of transactions, and the data analytics that optimize pricing and predict demand. The app you see is just the front end—underneath is a massive technology operation with cloud infrastructure, machine learning models, and APIs that businesses integrate with. That's why Grab can scale across multiple countries and services without owning a single vehicle or restaurant. That observation made me pause and take a closer look. If a company becomes this embedded in everyday behavior, perhaps it’s worth understanding why — and whether that presence can translate into enduring business value.

How does it make money?

Grab's strategy is built on what investors call a "flywheel effect":

More users signing up attracts more drivers and restaurants to the platform (because there's more business to capture)

More drivers and restaurants means better service for users—faster pickups, shorter delivery times, more food choices

Better service brings in even more users, and the cycle keeps spinning and accelerating

This creates a sticky platform where people keep coming back. Here's the key insight: Grab uses its popular (but low-profit) delivery and ride services to get millions of people hooked, then cross-sells their higher-margin financial products. If they can pull this off, that's where the real money is made.

What Exactly is the "Flywheel Effect"?: Think of it like a snowball rolling downhill—it gets bigger and faster as it goes. With Grab, when more people use the app, it attracts more drivers and restaurants (they want access to those customers). More drivers and restaurants means better service (faster rides, quicker deliveries, more options). Better service brings in even more users, which attracts more drivers and restaurants, and the cycle repeats. The beauty is that once this wheel starts turning, it becomes self-reinforcing and harder for competitors to stop. Each turn of the wheel makes Grab's platform more valuable to both users and service providers. That's why network effects are so powerful in platform businesses—the big gets bigger, almost automatically.

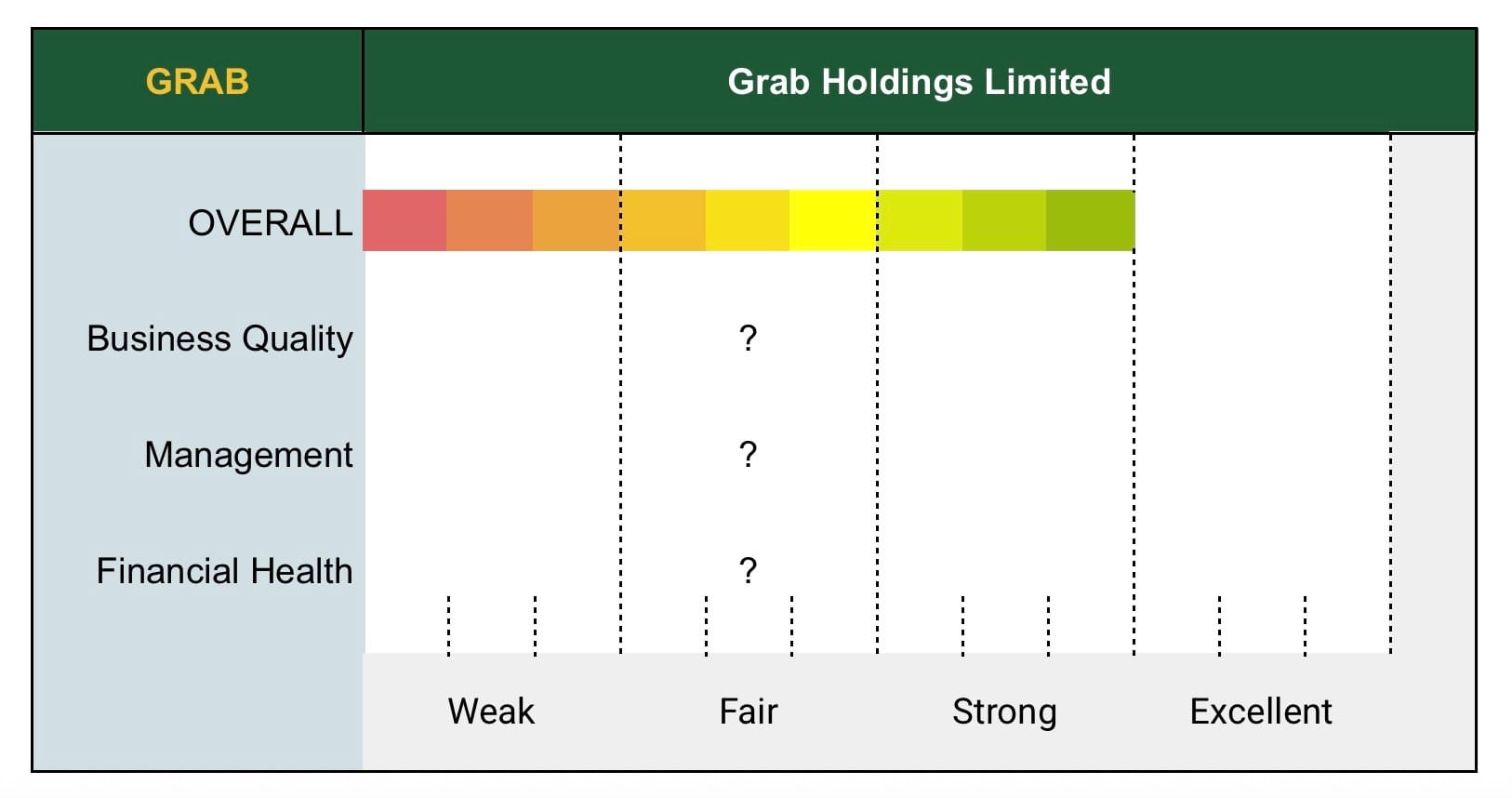

The Glavcot Business Quality Scorecard

Understanding the "?": Our initial assessment points to an Overall Quality of Strong. But what truly drives this rating? Is it the underlying Business Quality, the Management decisions, or the Financial Health? Unpacking these crucial components requires the deep dive - The Owner’s Analysis.

Summary of Initial Assessment

Grab is a high-risk, high-reward turnaround play. The business has a decent competitive moat thanks to its regional network, and it's finally showing real pricing power. Management deserves credit—they've successfully shifted from burning cash to chasing profitability. But here's the concern: the financials are still weak, with years of massive losses dragging down returns. The bright spot? Free cash flow has improved dramatically, which is the most encouraging sign for investors. That said, this turnaround isn't complete yet—it's still a speculative bet.

Note on Initial Assessment: This summary and Overall score reflect our high-level findings. The final assessment of each pillar (Business Quality, Management, Financial Health) is determined through our comprehensive Owner's Analysis, available exclusively to members after rigorous investigation.

Business Quality & Moat:

The Path to Profitability (Operating Leverage)

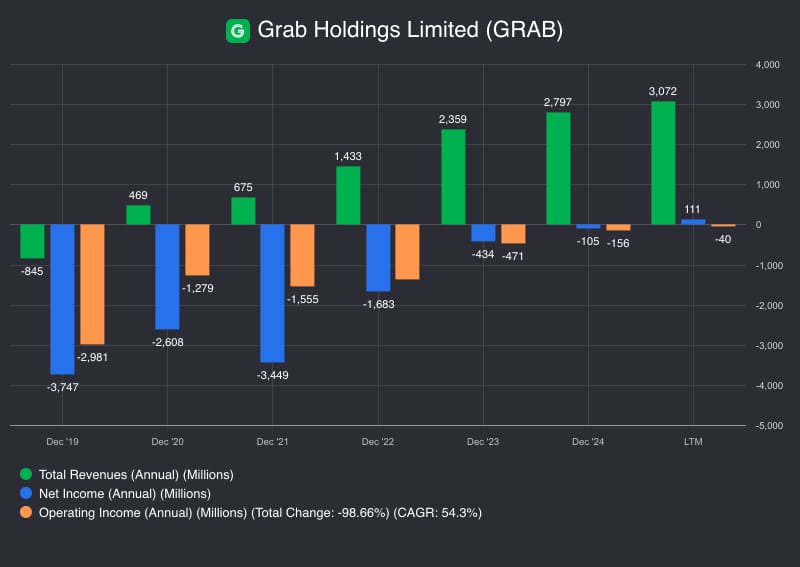

Chart A (below) shows Grab's pivot from "growth-at-all-costs" to "profitable growth." For years, the company's losses were staggering. In December 2021, for example, Operating Losses (orange bar) were a massive -$3,449 million, dwarfing its Revenue (green bar) of just $675 million. This was the cost of "buying" growth with heavy subsidies.[^ Source: Company Filings (Data aggregated using Fiscal.ai)]

While this chart doesn't show the margin percentage, the explosive growth of the green Revenue bars is the direct result of new-found pricing power. It proves that as Grab cut back on incentives, its revenue still scaled rapidly. Simultaneously, the chart clearly shows the blue (Net Loss) and orange (Operating Loss) bars shrinking towards zero. This combination—revenue scaling up from pricing power, while losses are controlled—is the classic visual of a business finally achieving operating leverage.

Chart A

Management Quality:

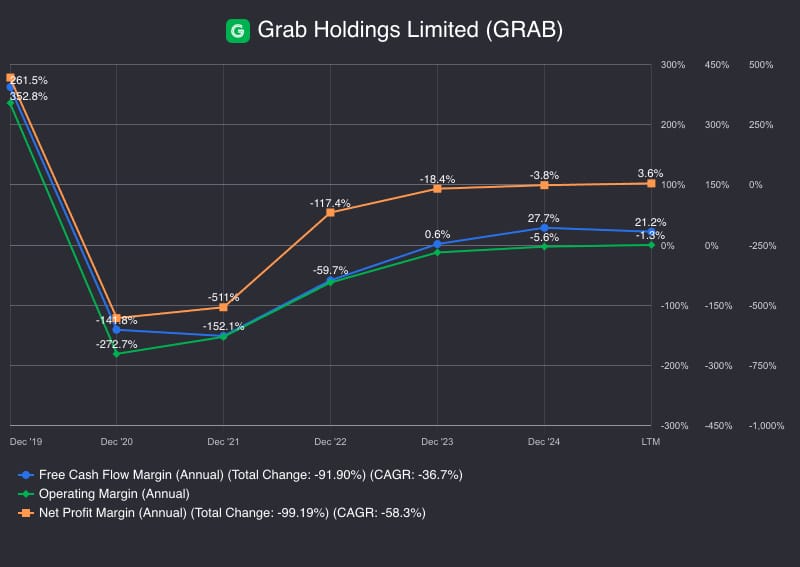

Cost Discipline: Management is executing on their profitability plan, and you can see it directly on Chart B (below). The aqua line (Operating Margin) represents profitability after all corporate and overhead costs. For years, this was disastrously negative (e.g., -272.7% in Dec '20). The fact that management has driven this line all the way up to near-breakeven at -1.3% (LTM) is a massive improvement and the clearest evidence of company-wide cost discipline.

Operating Leverage: The chart below shows they are finally getting the cost structure right. The business is now scaling (as shown by rising FCF and profits) without the massive, out-of-control losses of the past.

Financial Health:

Profitability Ratios: Let's be honest—the engine is still being rebuilt. As this chart shows, the LTM (Last Twelve Months) net profit margin is 3.6% (orange line), and the operating margin is still slightly negative at -1.3% (aqua line). These are nowhere near the 20%+ margins you'd want to see in a truly healthy business.

The Cash Flow Story: But here's the game-changer—the blue line. Free cash flow turned positive before net income did. The free cash flow margin today sits at a strong 21.2%, way better than that tiny 3.6% net profit margin. This tells you the profits are real and backed by actual cash generation, not just accounting tricks. This is the most important piece of evidence that the turnaround might actually work.

Chart B

Latest Updates (as of Q3 2025)

Grab’s latest financials reinforce the structural improvements highlighted in this First Principles Brief.

1. Profitability continues to normalize

Operating Margin has climbed from deeply negative levels in 2020–2021 to 0.8% LTM, with Net Profit Margin at 3.8% LTM. While still modest, the consistency of improvement shows that Grab’s cost discipline and take-rate optimization are sticking.

2. Revenue growth remains steady despite a softer macro backdrop

LTM revenue stands at US$3.23B, maintaining a multi-year uptrend even as GMV growth stabilizes. This shows that Grab’s shift toward quality of GMV—rather than chasing sheer volume—is translating into healthier monetization.

3. Free Cash Flow has turned sustainably positive

After years of heavy burn, FCF Margin is now 5.6% LTM. This signals that Grab’s unit economics have genuinely crossed the inflection point.

4. Balance sheet remains strong

Grab’s liquidity remains one of its underappreciated advantages. Total liabilities have fallen meaningfully since 2021, the current ratio is a still-healthy 1.8, and debt remains low relative to cash.

5. CapEx intensity has normalised

CapEx-to-Revenue peaked at about 11% in 2021 and has steadily declined to roughly 3% since 2023, while the year-over-year change in CapEx intensity has been negative for three consecutive years. This confirms that Grab has exited the heavy build-out phase and is operating on a more mature, asset-light base.

Overall:

The Q3 2025 data strengthens the FPB’s conclusion: Grab is transitioning from a growth-at-all-costs platform into a structurally improving, cash-generating ecosystem.

Conclusion: The Owner's Dilemma

Here's what you need to wrestle with if you're thinking about buying Grab: it's clearly a regional powerhouse with big ambitions, but it's still fighting off competitors and dealing with financial challenges.

The questions you should be asking yourself:

Are the unit economics sustainable now that they've cut the subsidies? [^ Management confirmed this in their earnings reports. In their 2023 full-year results, Grab reported that On-Demand incentives as a percentage of GMV (their key metric) improved by 230 basis points for the year, falling from 10.5% in 2022 to 8.2% in 2023. This proves they are spending significantly less on subsidies for every dollar of transactions on their platform.]Will customers stick around?

Can the financial services business actually become the profit machine they need it to be? That's supposed to be where the big margins come from.

Will management stay disciplined? Or will they get sucked back into expensive battles for market share, burning cash again?

These are the critical unknowns. The recent cash flow improvement is encouraging, but this is still a show-me story. You're betting on execution, not proven results. Understanding these risks is essential before you decide whether Grab belongs in your portfolio.[^ Disclosure: As of the date of publication, the author holds a long position in the following securities mentioned: Grab Holdings (GRAB). The author has no plans to initiate or alter a position in any of the securities mentioned within 72 hours of publication.]

In short: Grab is a recovering patient showing strong vital signs—cash flow has surged to 21.2% of revenue while overhead costs plummeted from 116% to just 27%. They've stopped paying customers to use them (gross margins swung from -105% to +41%), proving real pricing power. But here's the tension: they're barely profitable on paper at 1.4% margins, and years of losses have left them weak. You're not buying what Grab is today—you're betting on what it's becoming. If this trajectory holds, it's a potential home run. If they backslide into cash-burning growth battles, you could lose. Understanding these risks is essential before you decide whether Grab belongs in your portfolio.

The stakes are clear, but the devil is in the details. Our comprehensive members-only analysis dissects the unit economics behind each business segment, maps out the competitive threats that could derail this turnaround, and reveals whether management's capital allocation track record justifies your trust. This is where conviction gets built—or where you discover the red flags hiding in plain sight.

Glavcot Insights is now live. Join the free tier to get new research, updates, and future analysis directly in your inbox. (Check your spam folder if you don't see the confirmation email)

You might also like

Feb 26

NetEase: The Artisan's Engine in a Platform World

The way I see it, digital gaming has become what coffee is to the modern professional: a near-daily ritual, recession-resistant, and remarkably sticky. In idle moments, in downtime, in the spaces between — people reach for it. The market is enormous. The question is who's capturing it.

6 min read

Jan 05

Samudera Shipping Line Ltd. (S56): The Owner's Analysis

Samudera Shipping Line operates at the intersection of structural advantage and cyclical volatility. This analysis examines whether the company's Three-Layered Defense—cabotage protection, niche regional focus, and vertical integration—creates a sustainable moat

21 min read

Jan 01

TAYLOR SWIFT: THE ECONOMICS OF OVER-SERVING

"It is our job to make this look accidental, and it is our job to make this look effortless. I don't think of this as the pieces falling into place. You PUT the pieces where they are."

— Taylor Swift to her dancers and co-performers,The Eras Tour (Taylor's Version) documentary

That stopped me.

8 min read

Dec 22

Grab Holdings: Snapshot

Grab Holdings Limited

First Principles Brief (GRAB)

"Engineering an Economic Flywheel."

The One-Liner

Southeast Asia's leading

3 min read

Dec 07

The Hour Glass Limited (AGS.SI): Gatekeepers of Time — How a Family Retailer Built a Luxury Moat Piece by Piece

A family-owned gatekeeper to the world's most exclusive timepieces across Asia-Pacific — holding authorized dealer relationships with Swiss luxury brands that most retailers can't access...