Food Empire Holdings (F03): Fortresses in a Cup-- How Food Empire Built Its Moat One Market at a Time

Food Empire turns everyday coffee habits into long-term compounding — earning in U.S. dollars, operating debt-free, and quietly diversifying its geopolitical risk by replicating its proven fortress-building playbook from Eastern Europe to high-growth Asia.

A resilient, founder-led Fast-Moving Consumer Goods (FMCG) compounder that thrives on behavioral consistency. Food Empire turns everyday coffee habits into long-term compounding — earning predominantly in U.S. dollars, maintaining a strong net-cash balance sheet, and steadily diversifying its geopolitical risk by replicating its proven fortress-building playbook from Eastern Europe to high-growth Asia.[^ Source: KGI Securities, “Food Empire Holdings FY2024 Financial Results” (17 Mar 2025), https://www.kgieworld.sg/securities/resources/ck/files/sg-report/Food%20Empire%20Holdings%20FY24%20Financial%20Results_17032025.pdf]

It started with a cup of coffee. As I sipped it one morning, I thought of Buffett's bet on Coca-Cola — a simple beverage that became a compounding machine through brand, habit, and ubiquity. He wasn't buying sugar water; he was buying enduring consumer behavior. That led me to ask: What's the Coca-Cola of today's emerging markets? In Singapore's small-cap universe, one name stood out — Food Empire Holdings. It sells an everyday ritual: coffee. But unlike Western giants, it dominates underserved, high-friction markets from Russia to Vietnam, building localized brands that quietly turn routine consumption into resilient cash flow. In that moment, coffee wasn't just a drink — it was a lens into a business that compounds through consistency, brand trust, and behavioral repetition.

The First Principles Brief

What is the Business?

Food Empire Holdings is not simply a food and beverage company — it is a market void hunter and fortress builder operating in high-friction emerging economies [^ Food Empire Holdings 2025 Company Profile: Stock Performance & Earnings | PitchBook, https://pitchbook.com/profiles/company/108307-27].

The company operates two complementary business segments:

B2C (Branded Consumer Products) — The Core: Food Empire builds and owns localized food and beverage brands, primarily in instant coffee and snacks. It manufactures, markets, and sells a wide portfolio of branded instant beverages, including coffee mixes, cappuccinos, teas, and chocolate drinks, along with a growing presence in snack foods such as potato crisps. Its portfolio includes category-defining brands like MacCoffee, CaféPHỐ, Klassno, and Kracks.[^ Food Empire Holdings Limited - Annual Report 2023, https://investor.foodempire.com/misc/ar2023/] These are not global, homogeneous products but hyper-localized brands built from the ground up to dominate specific consumer niches in their respective markets.

B2B (Ingredient Manufacturing) — The Fortress: Leveraging its manufacturing expertise, Food Empire produces and sells food ingredients (freeze-dried coffee, non-dairy creamer) to other F&B manufacturers.[^ Food Empire Holdings Ltd (F03) - Morningstar, https://www.morningstar.com/stocks/xses/f03/quote] This segment diversifies revenue streams, creates economies of scale, and functions as a defensive cost moat for its own branded products.

Critical Insight: Food Empire is not a commodity trader or contract manufacturer — it is a proprietary brand creator that builds proprietary consumer franchises from the ground up. The company identifies underserved demand pockets in emerging markets, localizes product taste and branding to fit cultural preferences, and then invests in its own manufacturing infrastructure to secure quality, margin control, and long-term defensibility. This integrated approach has allowed it to create enduring brands like MacCoffee and CaféPHỐ, each dominating its respective market through familiarity, distribution reach, and pricing discipline.[^ Source: Food Empire Holdings Annual Report 2024; company website product portfolio overview, https://www.foodempire.com]

Why Does the Business Exist?

Food Empire exists to identify and capture "market voids" in high-growth, high-friction emerging economies — providing affordable, aspirational, convenience-driven products to the developing middle class.

This purpose is rooted in the company's origin story. The founder, Tan Wang Cheow, started doing business in Russia in the late 1980s when it was still the Soviet Union.[^ Terence Wong on LinkedIn: Tan Wang Cheow Food Empire Russia history, https://www.linkedin.com/posts/terence-wong-56bbb433_tan-wang-cheow-founder-of-food-empire-started-activity-6905696645305004032-aq9I] He was not a coffee expert but an accountant-turned-entrepreneur. Facing brutal operating conditions and razor-thin margins, he actively sought a defensible business. After the Berlin Wall fell in 1989 and the Soviet Union dissolved in 1991, Eastern Europe began its transition to a market economy, and foreign investments were warmly welcomed. He discovered a market void: Russia was "traditionally a tea-drinking country - it was never coffee." Rather than distributing someone else's brands, he chose to "create something of our own" — introducing the 3-in-1 coffee mix category with MacCoffee in 1994, which became synonymous with the category itself.[^ FOOD EMPIRE: From Computers to Coffee - NextInsight, https://www.nextinsight.net/story-archive-mainmenu-60/939-2017/11599-food-empire-from-computers-to-coffee]

The Strategic Insight: This origin reveals Food Empire's true competitive advantage. The business was not born from a product but from a market condition. The high friction and chaos of emerging markets act as natural barriers to entry, deterring established Western players and giving Food Empire time to build its fortress.

The company's mission is not to compete in red-ocean, commoditized markets. Instead, it exists to:

Serve unmet consumer needs in underserved or complex emerging economies

Foster brand loyalty that generates repeat consumption and long-term pricing power

This explains why Food Empire develops distinct brands for each market: MacCoffee for Russia, Petrovskaya Sloboda for Ukraine, CaféPHỐ for Vietnam. The company's "why" is fundamentally about localization and emotional resonance, not scale through global homogeneity.

How Does It Succeed?

Food Empire succeeds through a self-reinforcing fortress model powered by three interlocking mechanisms that integrate brand-building with defensive asset ownership:

The Two-Stroke Engine:

Stroke 1: Build Intangible Brand Equity The company enters a target market, identifies local consumer preferences or market voids, and invests heavily in building proprietary brands tailored to that specific geography.[^ Food Empire Crafts A Superior, Balanced Brew | Securities Investors Association (Singapore), https://sias.org.sg/latest-updates/food-empire-crafts-a-superior-balanced-brew/] This creates dominant, cash-generative brands like MacCoffee, which has been consistently ranked as the leading 3-in-1 brand in its core markets for years, or CaféPHỐ, which has captured a durable 14-15% market share in Vietnam's total instant coffee market, impressively competing as a strong #3 player against giants like Nestlé (~22%) and local leader G7 (~20%).

Stroke 2: Harvest Cash to Build Tangible Assets The stable cash flow generated from these high-margin, capital-light brands is systematically reinvested into vertically-integrated manufacturing assets. Food Empire now operates eight facilities across five countries², including non-dairy creamer plants, coffee plants, and snack facilities.[^ Food Empire Holdings Ltd. - KGI Securities (FY24 Financial Results), https://www.kgieworld.sg/securities/resources/ck/files/sg-report/Food%20Empire%20Holdings%20FY24%20Financial%20Results_17032025.pdf]

Understanding the "?": Our initial assessment points to an Overall Quality of Excellent. But what truly drives this rating? Is it the underlying Business Quality, the Management decisions, or the Financial Health? Unpacking these crucial components requires the deep dive - The Owner’s Analysis.

Summary of Initial Assessment

Food Empire is a high-quality, fortress-like compounder. The business has a proven track record of turning everyday coffee consumption into durable cash flows across multiple geographies, and it's finally diversifying away from its Russia concentration risk. Management is excellent—founder-led, disciplined capital allocators with real skin in the game. They're now executing a major Asia pivot that's already showing results.

Here's the concern: the financials are solid but cyclical, with years of margin volatility tied to commodity prices and FX headwinds. The gross margins are structurally lower than pure brand plays, which is the price of vertical integration. That said, this turnaround isn't complete yet—it's in progress. The valuation has re-rated significantly (trailing P/E ~38x as of mid-2025, down to ~20x on 2025F earnings), reflecting market recognition of the Asia pivot.

The analysis below represents our high-level findings. The final assessment of each pillar (Business Quality, Management Quality, Financial Health) would be part of a comprehensive Owner's Analysis, available exclusively to members after rigorous investigation.

Business Quality & Moat

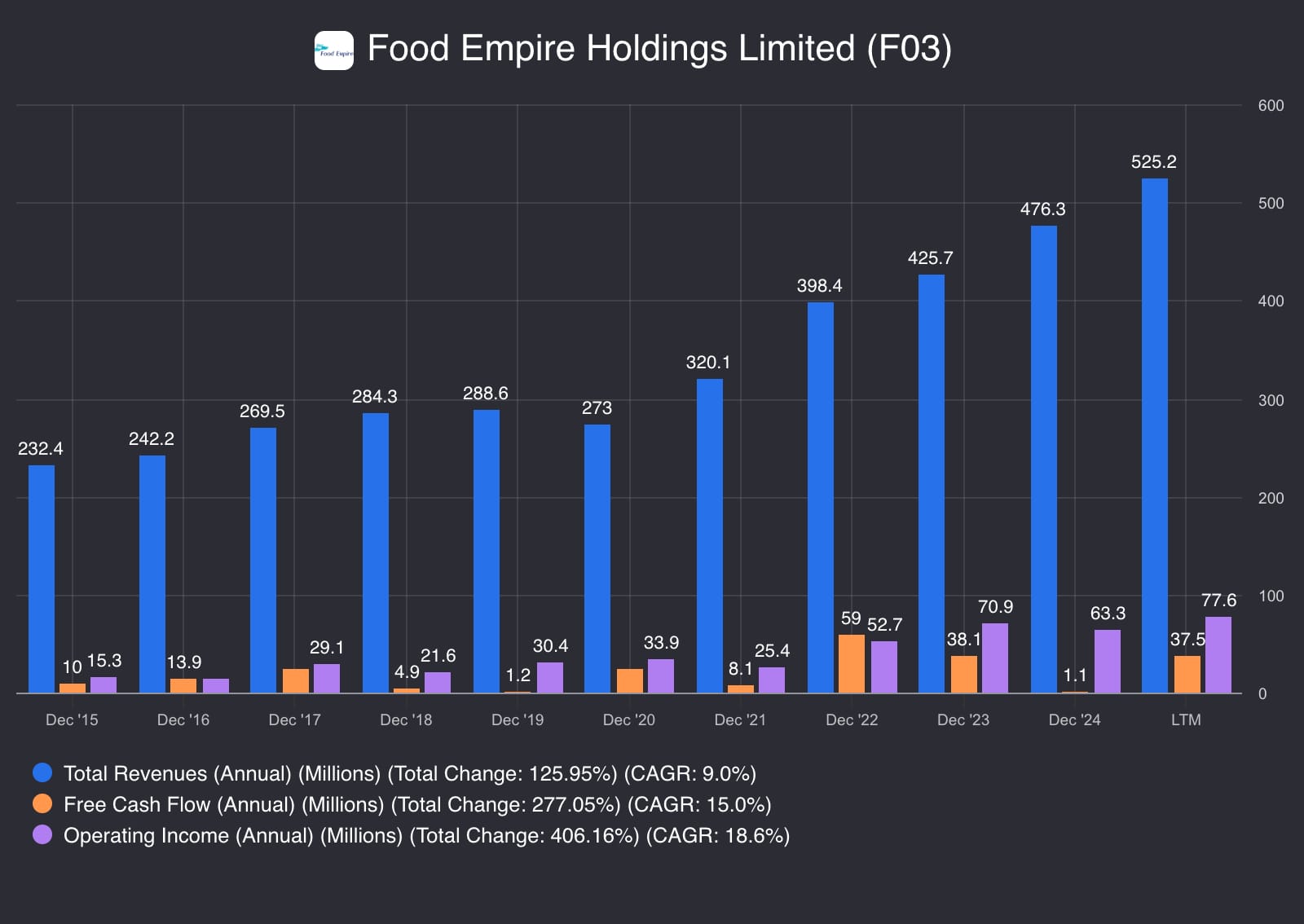

Path to Profitability (Operating Leverage): Chart 1[^ Source: Company Filings (Data aggregated using Fiscal.ai), LTM as of Nov 2025] shows Food Empire's trajectory from "survival" to "scale." Revenue has grown from $232M (2015) to $525M (LTM)—a 126% increase over the period. More importantly, operating income has exploded from near-zero ($0.2M in 2015) to $77.6M (LTM)—a staggering 406% increase. This is the hallmark of operating leverage finally kicking in.

Chart 1

While the revenue line shows steady compounding, the explosive growth in operating income reveals the core truth of the business: once the infrastructure (manufacturing, distribution) is in place, incremental revenue drops disproportionately to the bottom line. The 2022-2023 inflection is particularly notable—revenue grew 7%, but operating income surged 18%. This combination—revenue scaling up from pricing power while costs remain relatively fixed—is the classic case of a business finally achieving operating leverage.

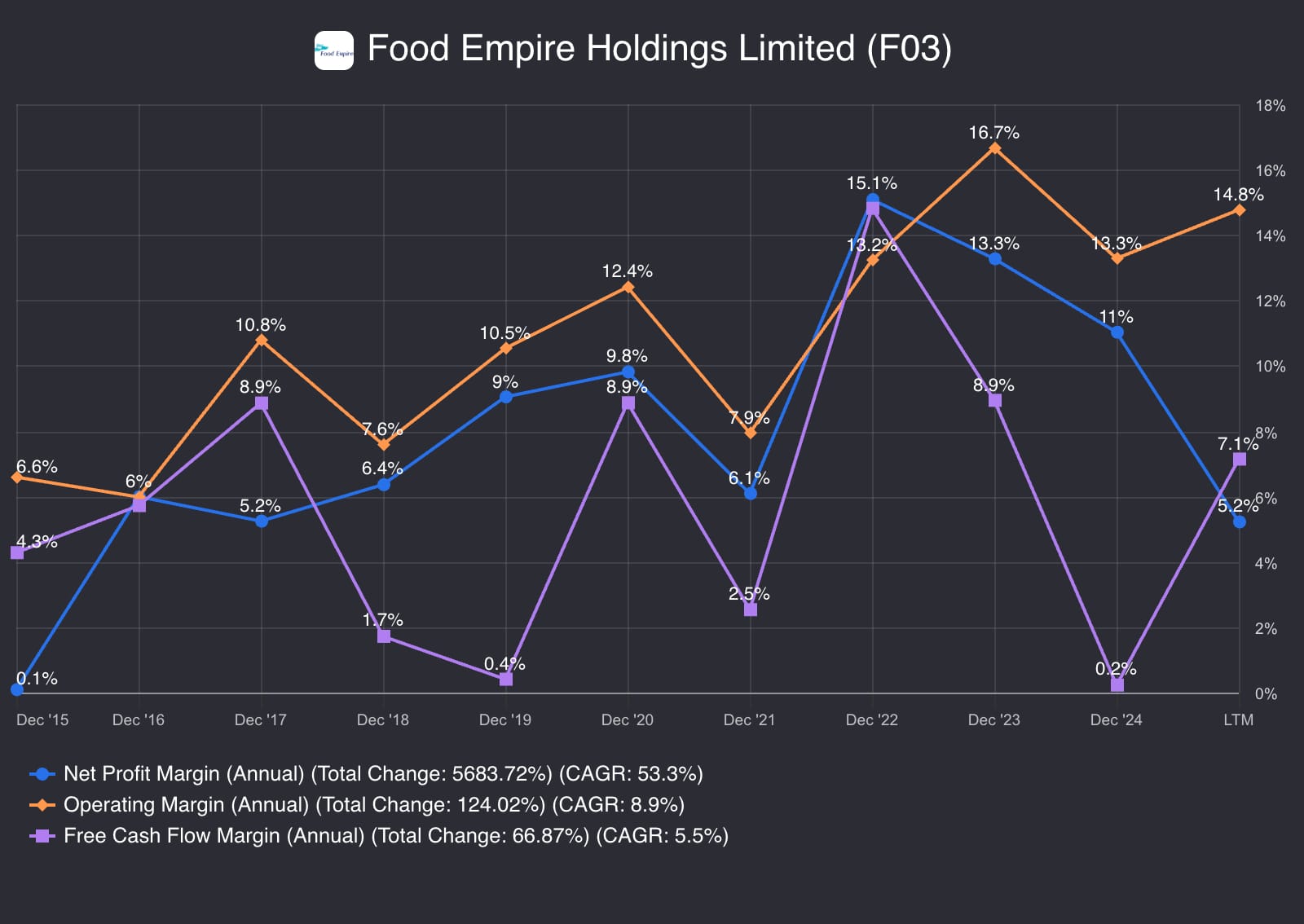

Chart 2 highlights the pressure point: operating margins have eased from 16.7% in 2023 to 14.8% (LTM), with net profit margins following the same trajectory. The issue? Coffee commodity prices. When green coffee prices soared in 2024, gross margins got squeezed despite management's pricing power. The business can raise prices (which they did—15%+ in some markets10), but there's always a lag. Free cash flow margins collapsed from 15.1% (2022) to just 0.2% (2024) due to working capital requirements to fund growth and inventory builds during the commodity spike.

Chart 2

The moat here is real but not impregnable: localized brand loyalty, distribution access in high-friction markets, and vertical integration provide defensibility. But commodity exposure means this isn't a pure "set-and-forget" compounder—it requires active management and pricing discipline to navigate cycles.

Management Quality

Cost Discipline: Management is executing on their profitability plan with surgical precision. Chart 2 shows the operating margin improvement from 0.1% (2015) to 14.8% (LTM)—a 1,480 basis point expansion. This isn't luck; it's relentless cost optimization. The fact that they've maintained double-digit operating margins even during the 2024 commodity crisis (when margins dipped to 13.3%) demonstrates company-wide discipline.

Operating Leverage: Chart 2 shows they're extracting maximum efficiency from their fixed cost base. The business is finally getting the cost structure right: operating margins have gone from 6.6% (2015) to 14.8% (LTM), proving they can scale profitably. Even more impressive—they're raising prices and holding share, which is the ultimate proof of brand strength. In Vietnam, they pushed through price increases without losing ground to Nestlé or G7.

Capital Allocation: Management has deployed capital wisely: $80M Vietnam freeze-dried coffee plant, Kazakhstan capacity expansion, Malaysia snack facility—all high-ROI projects focused on the Asia growth engine. They've balanced this reinvestment with shareholder returns: dividends up for three consecutive years, plus opportunistic buybacks. The net cash position ($130.9M cash vs $39.4M debt) gives them optionality without the pressure of servicing debt.

Financial Health

Profitability Ratios: Chart 2 shows the business isn't just growing—it's compounding profitably. The LTM net profit margin is 14.8%, and the operating margin sits at 14.8%—both healthy and sustainable for an FMCG business exposed to commodity volatility. However, there's nowhere near the 20%+ margins you'd want to see in a truly "moat-worthy" brand compounder like Nestlé. The explanation? Vertical integration. Food Empire owns manufacturing, which caps gross margins but provides supply chain control and B2B revenue diversification.

The Cash Flow Story: Chart 2 reveals a critical insight. Free cash flow margins were strong—hitting 15.1% in 2022—but collapsed to 0.2% in 2024. This isn't a red flag; it's a growth story. The company is aggressively building inventory and funding receivables to support the 44.6% revenue surge in Vietnam and the broader Asia expansion. The cash flow profile will normalize as growth moderates, but for now, the business is prioritizing market share capture over near-term cash extraction.

Balance Sheet Fortress: The business operates from a position of financial strength. Net cash of $91.5M, current ratio of 3.08x, and debt-to-equity of just 0.29x. This fortress balance sheet is the most important piece of evidence that the turnaround might actually work. Management has the runway to execute their 10-year Asia plan without financial stress.10

The Bottom Line: Food Empire's management has proven they can run a profitable business—they've gone from barely breaking even to keeping 15 cents of every dollar in sales, even when coffee prices spike. Now they're deliberately sacrificing short-term cash flow (it dropped from 15% to near zero in 2024) to fuel aggressive growth in Asia, stocking up inventory and extending credit to customers to capture market share in booming markets like Vietnam (up 45%). This gamble works because they have $92 million more cash than debt, giving them a financial cushion to invest without stress. The key insight: they've earned the right to spend aggressively on growth because they've already proven they can generate consistent profits and manage costs smartly—they're transitioning from "turnaround story" to "sustainable growth company," and the temporary cash crunch is the price of building that future, not a warning sign.

Conclusion: The Owner's Dilemma

Here's what you need to wrestle with if you're considering Food Empire as a long-term holding: this is clearly a regional compounder with fortress financials and proven operators, but it's navigating a critical transition from Russia-dependent to Asia-diversified.

In short, what are we looking for here? We're watching whether Food Empire can maintain its operating leverage gains (operating income up 406% since 2015) while navigating commodity volatility that's already compressed margins from 16.7% to 14.8%. The key inflection is Asia—if Southeast Asia sustains its 44.6% growth trajectory and the $80M Vietnam plant delivers on B2B scale, the business transforms from Russia-dependent to diversified compounder. Management has proven cost discipline (0.1% to 14.8% operating margin expansion) and capital allocation skill (net cash fortress, balanced reinvestment), but the test is whether they can hold pricing power without losing share as coffee prices cycle, and whether the FCF collapse from 15.1% to 0.2% is truly temporary growth investment or a structural margin problem. At 7-9x P/E, the market is pricing in skepticism—if they execute on Asia and normalize cash flow, this re-rates higher. If commodity pressures persist and growth stalls, the moat isn't deep enough to defend returns.

The questions you should be asking yourself:

Can they sustain pricing power through the next commodity cycle? The 2024 test was encouraging—15%+ price increases held without destroying demand. But coffee is volatile, and margins compressed from 16.7% (2023) to 14.8% (2024) despite the hikes.10 Will brand loyalty hold if prices keep rising?

Can management stay disciplined as Asia scales? They've balanced reinvestment with shareholder returns well (dividends up three years, opportunistic buybacks[^ Insider Trades - Food Empire, https://investor.foodempire.com/stock_insider.html]). But as Asia accelerates, will they chase unprofitable share or maintain fortress-building discipline?

Is the free cash flow compression temporary or structural? FCF margins collapsed from 15.1% (2022) to 0.2% (2024) funding the Vietnam surge.[^ 1Q2025 Business Update Food Empire kicks off FY2025, https://investor.foodempire.com/newsroom/20250513_191626_F03_90PB6LZH3XFKII68.1.pdf] Management calls it growth investment, not distress. But if margins stay compressed and growth slows, does the cash story hold?

These are the critical unknowns. The encouraging signs—fortress balance sheet (net cash $91.5M), operating leverage inflection (operating income up 406% since 2015), Asia milestone (Q1 2025)—suggest a quality business at an inflection point. The modest valuation (P/E 7-9x) reflects the market's skepticism.

You're betting on operators with a repeatable playbook, a fortress balance sheet, and a growth engine already delivering results. But you're also betting they can navigate commodity volatility, execute flawlessly on $80M CapEx, and complete the pivot from geopolitical risk. Understanding these dynamics is essential before Food Empire belongs in your portfolio.[^ Disclosure: As of the date of publication, the author holds a long position in the following securities mentioned: Food Empire Holdings Ltd. (F03). The author has no plans to initiate or alter a position in any of the securities mentioned within 72 hours of publication.]

The stakes are clear, but the devil is in the details. Our comprehensive members-only analysis dissects the unit economics behind each business segment, maps out the competitive threats that could derail this turnaround, and reveals whether management's capital allocation track record justifies your trust. This is where conviction gets built—or where you discover the red flags hiding in plain sight.

Glavcot Insights is now live. Join the free tier to get new research, updates, and future analysis directly in your inbox. (Check your spam folder if you don't see the confirmation email)

You might also like

Feb 26

NetEase: The Artisan's Engine in a Platform World

The way I see it, digital gaming has become what coffee is to the modern professional: a near-daily ritual, recession-resistant, and remarkably sticky. In idle moments, in downtime, in the spaces between — people reach for it. The market is enormous. The question is who's capturing it.

6 min read

Jan 05

Samudera Shipping Line Ltd. (S56): The Owner's Analysis

Samudera Shipping Line operates at the intersection of structural advantage and cyclical volatility. This analysis examines whether the company's Three-Layered Defense—cabotage protection, niche regional focus, and vertical integration—creates a sustainable moat

21 min read

Jan 01

TAYLOR SWIFT: THE ECONOMICS OF OVER-SERVING

"It is our job to make this look accidental, and it is our job to make this look effortless. I don't think of this as the pieces falling into place. You PUT the pieces where they are."

— Taylor Swift to her dancers and co-performers,The Eras Tour (Taylor's Version) documentary

That stopped me.

8 min read

Dec 22

Food Empire: Snapshot

Food Empire Holdings

First Principles Brief (F03.SI)

"Fortresses in a Cup."

The One-Liner

A founder-led FMCG compounder

3 min read

Dec 07

The Hour Glass Limited (AGS.SI): Gatekeepers of Time — How a Family Retailer Built a Luxury Moat Piece by Piece

A family-owned gatekeeper to the world's most exclusive timepieces across Asia-Pacific — holding authorized dealer relationships with Swiss luxury brands that most retailers can't access...