The One-Liner

Centurion is a leading specialized accommodation provider that builds and operates mission-critical human infrastructure — regulated housing for the global workforce and international students — yielding high-margin recurring income through proprietary management and capital recycling.

In one of my past architecture projects, we worked on student hostels and worker dormitories. At the time, I thought about them the way any architect does — as a program to solve, a brief to meet, a structure to deliver. The idea that they could be an investable asset class didn't cross my mind. There was no avenue for the public to own them anyway.

Fast forward to late 2025. In the course of my usual reading, I came across the IPO announcement for Centurion Accommodation REIT. My default assumption about IPOs is a familiar one: prices spike on listing day, early sellers capture the pop, and long-term investors spend years waiting for price to catch up with value.

But this one gave me pause. The reception was unusually strong — 30.9 times subscribed at retail, 16 times at institutional. The initial data looked credible. And something about the asset class felt structurally familiar — not from finance, but from the drawing board.

I kept it in view. And eventually decided it deserved a proper analysis.

Fast forward to late 2025. In the course of my usual reading, I came across the IPO announcement for Centurion Accommodation REIT. My default assumption about IPOs is a familiar one: prices spike on listing day, early sellers capture the pop, and long-term investors spend years waiting for price to catch up with value.

But this one gave me pause. The reception was unusually strong — 30.9 times subscribed at retail, 16 times at institutional. The initial data looked credible. And something about the asset class felt structurally familiar — not from finance, but from the drawing board.

I kept it in view. And eventually decided it deserved a proper analysis.

A Brief IPO History

CAREIT listed on the SGX Mainboard on 25 September 2025 under stock code 8C8U — becoming Singapore's first pure-play purpose-built living accommodation REIT.6

The IPO was priced at S$0.88 per unit. Units opened at S$0.98 on listing day and rose 9.1% by close — making it Singapore's second-largest listing of 2025, raising S$771.1 million in total proceeds.6 The public offer tranche was 30.9 times subscribed, the strongest retail response in recent years. The placement tranche was approximately 16 times subscribed by international institutional investors, real estate specialist funds, and high net-worth individuals.7

The initial portfolio comprised 14 assets valued at approximately S$1.84 billion: five PBWA assets in Singapore, eight PBSA assets in the UK, and one PBSA asset in Australia. With the subsequent acquisition of Epiisod Macquarie Park, the enlarged portfolio grew to 15 properties valued at approximately S$2.12 billion.6

Centurion Asset Management Pte. Ltd. — a wholly-owned subsidiary of Centurion Corporation Limited — serves as the REIT manager. That sponsor relationship is central to understanding the investment case.

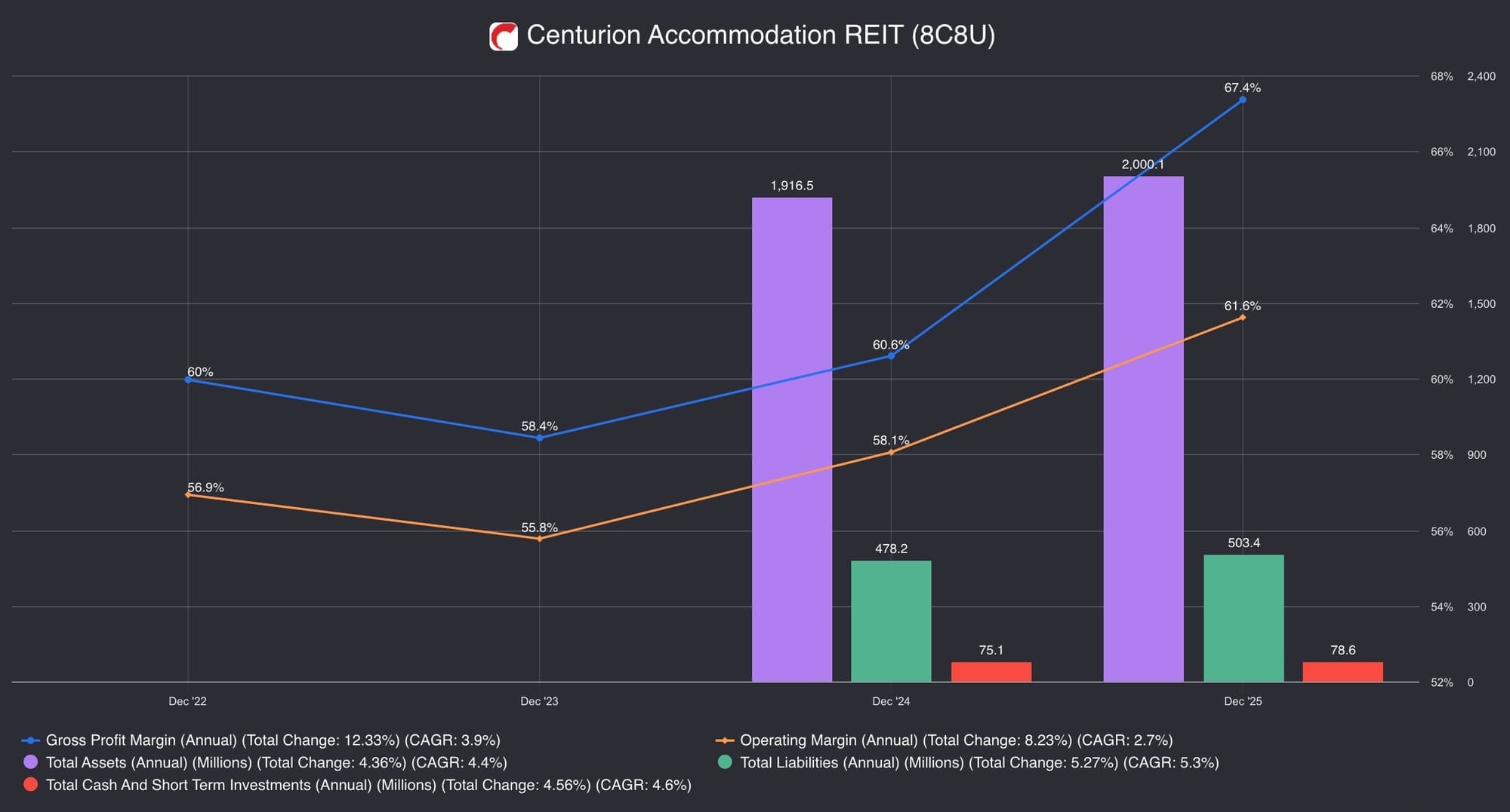

The chart below reflects CAREIT's financials since listing. Margin expansion and asset growth are visible. The dataset is early — two reporting periods — but the trajectory is consistent with the annuity engine thesis.

Why the Business Exists

Centurion was built on a single conviction: in a globalized economy, the physical presence of labor and students is non-discretionary, but the regulatory complexity of housing them creates a permanent supply bottleneck.1

The first principle of the business is the provision of essential, regulatory-compliant human infrastructure. As governments in Singapore and Malaysia aggressively elevate housing standards — through Singapore's FEDA regime and New Dormitory Standards — compliance becomes the ultimate barrier to entry. Centurion CEO Kong Chee Min built the business on a precise conviction: own the regulatory moat, and the market comes to you.4

The New Dormitory Standards mandate more space and better amenities by 2040, effectively rendering older, informal dormitories obsolete.4 As a pioneer of compliant assets, Centurion is positioned to capture premium rental revisions as non-compliant supply contracts elsewhere. Compliance is not a cost center here — it is the competitive engine.

The customer insight is precise: employers and students are not buying a bed. They are buying risk mitigation and accessibility. For a corporate client, a Centurion bed is a guarantee against labor unrest and regulatory violation. For a student, it is a guarantee of safety and academic proximity.1

There's a symbiotic logic here that's easy to miss. Construction firms can't move foreign labor at scale without compliant housing. Universities can't credibly recruit international students without guaranteed accommodation nearby. Centurion doesn't just serve those needs — in many ways, it enables them. Pull the accommodation out, and the businesses that depend on it face a harder existence. That co-dependency isn't accidental. It is the architecture of essentiality.

How the Business Succeeds

Centurion makes money by converting the structural undersupply of essential housing into recurring spending — and doing so at margins that outperform generalist real estate.5

The economics are driven by three compounding advantages

Switching costs and high barriers.

Approximately 62.8% of tenants have renewed leases for five years or longer.2 For corporate clients, the friction of moving a workforce to a non-compliant or unproven provider introduces catastrophic regulatory risk, making Centurion's assets sticky infrastructure rather than interchangeable commodity beds.

Regulatory leverage.

New Dormitory Standards make older, informal dormitories obsolete by 2040.4 As the pioneer of compliant assets, Centurion captures premium rental revisions as supply contracts elsewhere. The moat widens every time the regulatory bar rises.

Capital efficiency.

The 2025 REIT spin-off unlocked over S$700 million, allowing the group to deleverage — dropping net gearing to 12% — and pivot capital toward high-growth regions including the Middle East and China's Build-To-Rent sector.4

The result is a business generating S$139.2 million in core net profit, sustaining occupancy at 98–99%, and returning capital through a growing dividend — positioning it as a mission-critical utility for the 21st-century economy.5

What I'll Be Looking At

For accommodation, the broad answer feels obvious: workers will still build cities. students will still cross borders for education.

The harder question is who captures that demand — and on whose terms. Centurion's answer, so far, has been: the one who owns the compliance infrastructure. The three variables below test whether that answer holds.

Will Centurion remain the structural gatekeeper of that necessity — or merely a landlord operating inside a tightening regulatory box?

Beyond the three pillars outlined above, three deeper variables determine whether the answer is yes.

First, capital structure and alignment. The 2025 REIT spin-off unlocked capital and reduced gearing. But it also created a structure where Centurion develops assets, stabilizes them, and injects them into a vehicle it manages for fees — while retaining the growth pipeline outside it. Sponsor and unitholder interests can quietly diverge. The question is whether this machine compounds prudently — or drifts toward AUM growth that serves the manager more than the owner.

Second, regulatory evolution. New Dormitory Standards raise compliance thresholds — which today act as a barrier to entry. But if pricing power becomes politically sensitive as standards tighten, the moat may be real while margin expansion is not. That is the distinction between a barrier and a return ceiling.

Third, demand cyclicality versus structural necessity. Occupancy at 98–99% is compelling. The question is what it reflects. Construction cycles turn. Immigration policies shift faster than asset depreciation schedules. If resilience holds through a real downturn, the essential infrastructure thesis strengthens. If it cracks, the narrative compresses into a normal property cycle story.

First, capital structure and alignment. The 2025 REIT spin-off unlocked capital and reduced gearing. But it also created a structure where Centurion develops assets, stabilizes them, and injects them into a vehicle it manages for fees — while retaining the growth pipeline outside it. Sponsor and unitholder interests can quietly diverge. The question is whether this machine compounds prudently — or drifts toward AUM growth that serves the manager more than the owner.

Second, regulatory evolution. New Dormitory Standards raise compliance thresholds — which today act as a barrier to entry. But if pricing power becomes politically sensitive as standards tighten, the moat may be real while margin expansion is not. That is the distinction between a barrier and a return ceiling.

Third, demand cyclicality versus structural necessity. Occupancy at 98–99% is compelling. The question is what it reflects. Construction cycles turn. Immigration policies shift faster than asset depreciation schedules. If resilience holds through a real downturn, the essential infrastructure thesis strengthens. If it cracks, the narrative compresses into a normal property cycle story.

These three variables share a common thread: they determine not whether Centurion is a good business — on paper, it clearly is — but whether its economics durably belong to its owners.

Is this a compounding infrastructure platform —

or a yield vehicle shaped by policy and capital structure?

~ This is the opening thesis. ~

The full Owner's Analysis publishes April 2026

Footnotes:

- Centurion Corporation 3QFY2025 Business Updates Presentation, November 2025. Singapore Exchange. sgx.com

- Approximately 62.8% of tenants have renewed leases for five years or longer; near-full financial occupancy at 99%. Centurion Accommodation REIT — DBS Bank Initiation Report, November 2025. dbs.com

- PBSA assets in the UK and Australia positioned within walking distance of elite universities. Centurion REIT Stock Info (SGX:8C8U) — SGinvestors.io. sginvestors.io

- REIT spin-off unlocking over S$700 million; net gearing reduced to 12%; New Dormitory Standards and FEDA regime; Kong Chee Min's regulatory moat strategy. KGI Singapore — Centurion Corp 3Q25 Update Report, 2025; The Edge Singapore — Centurion Corp steps up growth plan with asset-light moves, 2025. theedgesingapore.com

- S$139.2 million core net profit; occupancy sustained at 98–99%; growing dividend. Centurion Corporation Limited FY2025 Results — Minichart, March 2026. minichart.com.sg

- CAREIT listed on SGX Mainboard on 25 September 2025; IPO priced at S$0.88 per unit; opened at S$0.98; rose 9.1% on listing day; Singapore's second-largest listing of 2025; raised S$771.1 million in total proceeds. Bloomberg — Centurion's REIT Spinoff Gains 11% in Singapore's Second-Largest Listing of 2025, September 2025. bloomberg.com

- Public offer 30.9 times subscribed; placement tranche approximately 16 times subscribed; initial portfolio of 14 assets valued at approximately S$1.84 billion; enlarged to 15 properties at S$2.12 billion post-acquisition of Epiisod Macquarie Park. Centurion Accommodation REIT IPO Completion Announcement, September 2025. investor.careit.com.sg

- Data source: Company filings. Data aggregated using Fiscal.ai. fiscal.ai

Disclosure: Glavcot Insights and its contributors may hold positions in securities discussed in this article. All content is provided for informational and educational purposes only. This is not investment advice — readers should perform independent research and consult financial professionals before making investment decisions.

Where Clarity Meets Conviction

Glavcot Insights is now live. Join the free tier to get new research, updates, and future analysis directly in your inbox. (Check your spam folder if you don't see the confirmation email)