Key Insight — Food Empire’s moat is earned, not inherited.

It is built on localized brand strength, disciplined vertical integration, and pricing power that consistently converts everyday consumption into durable economics — even under commodity and currency stress.

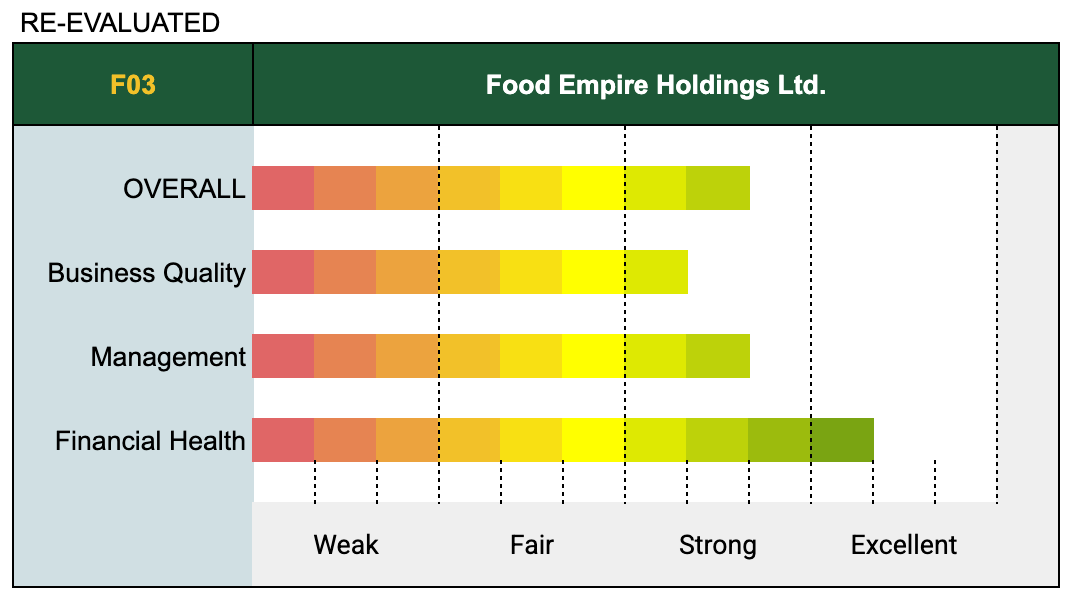

Rating: Strong

Key Insight — Food Empire’s moat is earned, not inherited.

It is built on localized brand strength, disciplined vertical integration, and pricing power that consistently converts everyday consumption into durable economics — even under commodity and currency stress.

Food Empire’s business quality rests on a simple but powerful proposition: turn habitual, low-ticket consumption into a high-return economic engine. The company wins in high-friction markets — where global multinationals struggle — by pairing localization with manufacturing control and granular distribution.

This section shows how the moat sustains itself — through localized brand dominance, granular execution, capital discipline, and pricing durability.

The Two-Engine Business Model

Food Empire’s resilience is driven by two complementary engines that create a self-reinforcing advantage:[^ KGI Securities, Food Empire FY 2024 Results (17 Mar 2025).]

Engine 1: Branded Consumer Products (B2C) — The profit driver.

Food Empire’s brands — MacCoffee in Russia/CIS and Café PHỞ in Vietnam — are category leaders built from the ground up for local tastes. These are not global templates: they are hyper-localized FMCG brands that convert daily coffee habits into recurring, high-margin cashflows.[^ Securities Investors Association (Singapore),

Balanced Brew,

” 2024.][^ PitchBook Company Profile – Food Empire Holdings (2025 accessed Nov 4).]

Engine 2: Ingredients Manufacturing (B2B) — The stabilizer.

The Group owns vertically integrated plants across Malaysia (creamer), India (coffee processing), and is building a new US$80m freeze-dried coffee plant in Vietnam (completion ~2028). This network creates:

cost control

supply security

consistent quality

external B2B revenue streams

Together, B2C profits fund B2B scale, and B2B scale reinforces B2C margins — forming a moat competitors struggle to replicate.[^ Morningstar Equity Report – F03 (SGX), 2025.]

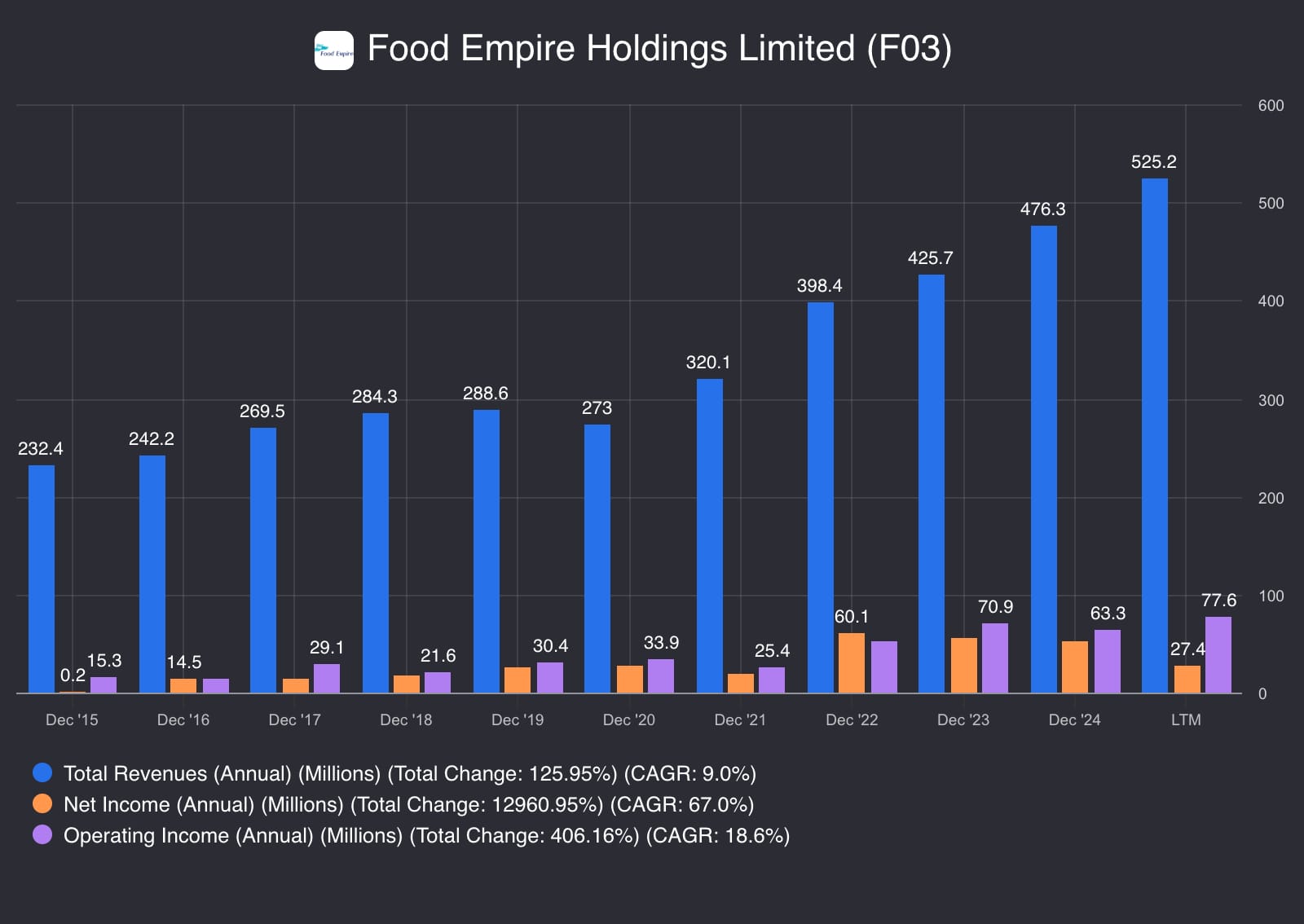

The Revenue–Net Income–Operating Income in Chart A shows Revenues nearly doubled from 2015 to LTM, while operating income grew 4× — evidence of operating leverage and structural moat strength.

Chart A

Think of it like a restaurant chain that owns its own farm. Food Empire sells instant coffee and creamer under recognizable local brands to everyday consumers — this is the high-margin "restaurant" where most profits come from. But they also own the factories that produce their own coffee extract and creamer — the "farm" that keeps costs predictable and quality consistent. Here's the moat: profits from branded sales fund bigger, better factories. Those factories then produce ingredients cheaper and more reliably than competitors who must buy from third parties. Lower costs strengthen margins. Stronger margins fund deeper distribution and brand-building. The loop compounds. Competitors can copy the "restaurant" (launch a coffee brand) or build a "farm" (open a factory). But replicating both simultaneously — and having them reinforce each other over 30 years across multiple geographies — is the hard part.

Localized Advantage in High-Friction Markets

Food Empire thrives where global brands often fail: traditional trade markets defined by fragmented retailers, local taste differences, and distribution complexity.[^ GlobalData Company Profile – Food Empire Holdings Ltd.]

Its advantages:

Localization: product flavour, pricing, and packaging tuned to local habits

Distribution depth: sales teams covering thousands of mom-and-pop shops

Cultural proximity: decades of presence in CIS and Vietnam

As Southeast Asia scales — especially Vietnam — this model is proving portable.

Chart A shows Revenue growth re-accelerated 6.9% → 11.9% → 10.3%, confirming Asia’s growing weight in Group performance.---

Vertical Integration as Competitive Advantage

Owning production and distribution converts scale into a defendable moat:[^ KGI FY 2024 Results, p. 3 – 4.]

mitigates commodity flows

preserves proprietary formulations

accelerates new product launches

supports cost discipline and pricing strategy

In Vietnam, Food Empire’s salesforce reaches tens of thousands of small retailers daily — a distribution depth global FMCGs rarely match. Integration + localization = sticky market share.[^ KGI FY 2024 Results, p. 2 (“price increases > 15 %”).]

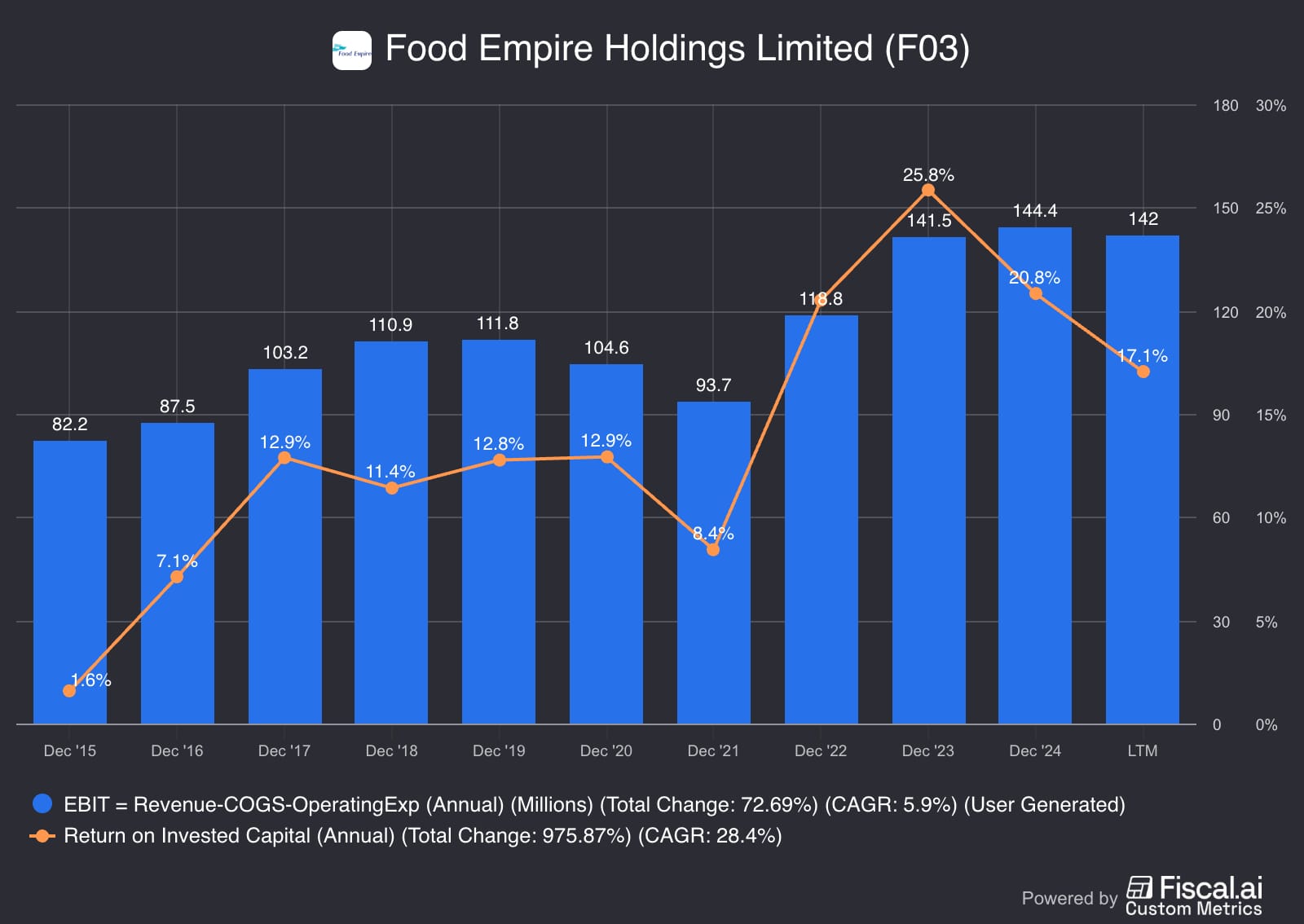

ROIC | EBIT

The ROIC Proof

Return on Invested Capital (ROIC) is the clearest indicator of business quality: it measures whether reinvested dollars create more value than they cost.

Food Empire’s ROIC tells a decade-long story of systematic improvement:

In the mid-2010s, ROIC sat in the low single digits during the business’s capacity-building phase.

As manufacturing scale and brand strength grew, ROIC climbed into the low-to-mid teens.

By 2023, ROIC reached its highest levels on record, reflecting the full expression of the moat.

Today, ROIC normalizes around ~17% LTM even while absorbing heavy capex for Vietnam’s new freeze-dried coffee facility.

This is not a cyclical spike — it is evidence of progressively better capital allocation over a decade.

Rising ROIC = rising proof the business model works.

Food Empire now reinvests capital at rates well above its cost of capital, validating the moat’s durability.

Period

ROIC Trend

Context

Mid-2010s

Low single digits

Capacity building; early-stage investment

2017–2021

Rising into mid-teens

Scaling manufacturing & distribution

2022–2023

Peak levels (mid-20s)

Moat fully expressed; strong pricing & efficiency

LTM (Q3 2025)

~17%

Normalized but strongly value-creating

As evident in Chart A, it shows ROIC remaining progressing to double digits, even through heavy CapEx cycles—proof of disciplined reinvestment.---

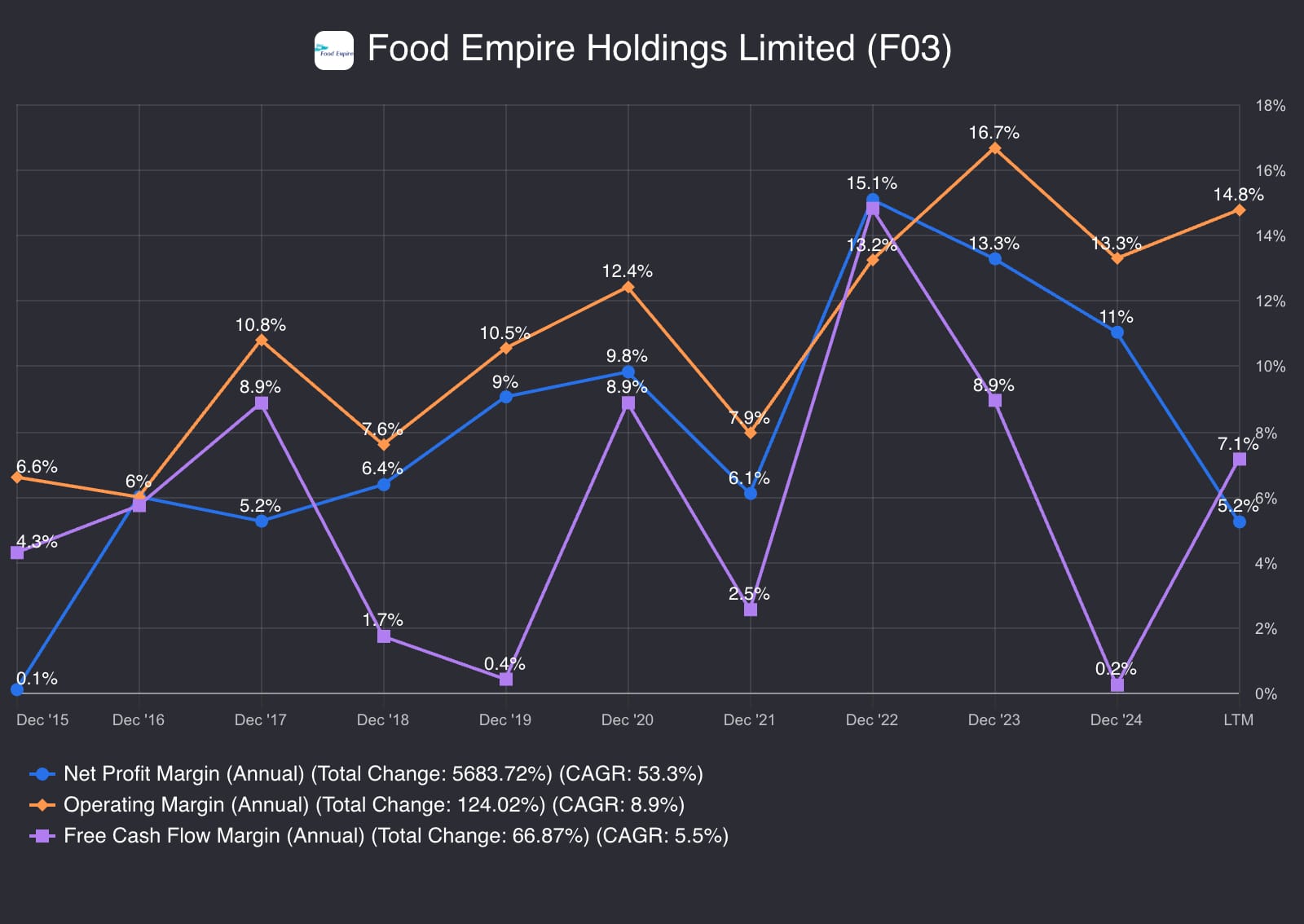

The Ultimate Moat Test: Pricing Power

Warren Buffett’s simplest moat test applies directly here: Can the company raise prices without losing customers?

In FY2024, global coffee bean prices surged ~70%, yet Food Empire successfully raised prices >15% in several markets — and management reported demand remained resilient.[^ KGI Securities (Singapore) Pte. Ltd. — Food Empire Holdings FY24 Financial Results (17 Mar 2025). Notes that “Brazil… droughts have driven prices up 70% since early 2024” and that demand for Food Empire’s products “remained resilient despite price hikes.”]

But the real insight comes from how margins behaved:

Net margin:

11.0% (2024) → 7.1% (LTM Q3 2025)

→ hit by FX losses and non-operating items, not customer resistance

This divergence is crucial:

Customers accepted price hikes.

Operating profit rebounded.

The moat held under pressure.

FX and accounting noise, not the business model, drove net margin decline.

The operating engine — where the moat lives — improved.

The net margin volatility reflects currency exposure, not erosion of brand power.

The chart Operating Margin vs. Net Margin vs. FCF Margin

Shows strengthening operating profitability despite severe cost inflation and currency headwinds.

Chart B

Margins in Chart B shows sustained profitability through the commodity cycle. Free cash flow narrowed to 0.2% (2024) due to temporary working-capital buildup for Vietnam growth—an investment choice, not deterioration.

This pricing durability completes the moat proof—tying brand dominance, vertical integration, and capital efficiency into a single, measurable competitive advantage.

Takeaway: Food Empire’s moat proves itself where it matters most: under stress. Even as commodity prices spiked and currencies swung, the operating engine strengthened — pricing held, margins expanded, and ROIC stayed well above value-creating levels. What wobbled was accounting noise, not the business model. The consistency of the core operations across cycles shows that Food Empire’s advantage isn’t situational; it’s structural. This is a company that turns everyday consumer habits into durable economics — a hallmark of a truly resilient Fast-Moving Consumer Goods (FMCG) compounder.

Final Assessment: Strong

Key Proof:

Structural moat evidenced by:

— High and rising operating margins (13.3% → 14.8% LTM)

— Resilient pricing power during a ~70% global coffee price spike

— Decade-long ROIC progression from low single digits to ~17% LTM

— Revenue + Operating Income scaling (2× and 4× respectively since 2015)

• Core operations strengthened even as net margin fell due to FX volatility, not business weakness.

Justification:

Food Empire’s moat passes every stress test. The combination of localized brands, granular distribution, vertical integration, and decade-long capital efficiency gains forms a structural advantage that competitors struggle to replicate. During one of the worst input-cost shocks in a decade, operating profitability improved — a rare signal of pricing durability and execution strength. Net margin volatility came from FX losses and accounting noise, not customer resistance or weakening demand. This separation between operating strength and below-the-line volatility reinforces the moat’s durability. Food Empire demonstrates the defining trait of a “Strong” business: its core economics get stronger under pressure, not weaker.

Pillar II: Management Quality

Rating: Strong Key Insight — Discipline over drama: A founder–operator culture that allocates capital with precision, patience, and a clear long-term compass.---

Food Empire’s moat—localized brands, vertical integration, and pricing power—creates the potential for durable value. But potential compounds only under disciplined leadership. A strong business in weak hands destroys value; a strong business in capable hands becomes a compounding engine.

Food Empire is led by a rare founding–operator structure. Executive Chairman Tan Wang Cheow, who began expanding the business in the late 1980s, still provides long-term strategic direction. Group CEO Sudeep Nair, with the company since 1993, drives operational execution with institutional rigor.[^ Food Empire Holdings Limited — Annual Report 2024; Board of Directors.][^ The Edge Singapore — leadership and expansion profile.] Together, they run one of the strongest-capitalized consumer-staples companies on SGX.

This pillar evaluates management through four lenses: execution quality, capital discipline, strategic adaptability, and alignment—based on the latest reported figures and the charts presented in this section.

1. Execution Quality: Performance Through Cycles

1.1 From marginal to scaled profitability

The long-term trend in the charts shows a business that has steadily moved from marginal profitability to scaled, repeatable cashflow:

Revenue has nearly doubled from 2015 to the latest reported 12-month period.

Operating income has grown more than 4× over the same timeframe.

Net income rose from roughly break-even in 2015 to its 2022–2023 peak, before normalising as below-the-line items fluctuated.

These outcomes reflect a management team that built scale patiently, tightened cost structures, and expanded intelligently into higher-return markets.

1.2 Margin behaviour during the commodity shock

Margin behaviour is the clearest test of execution quality.

Net margin: ~13.3% (2023) → ~11.0% (2024) → ~7.1% (latest 12 months)[^ Chart series included in this report — Operating Margin, Net Margin, Free Cash Flow Margin (2015–LTM).]

→ compressed due to FX and non-operating items, not operating weakness

This divergence matters:

Operating performance strengthened through the shock.

Net profit fell because of below-the-line volatility, not because customers resisted price increases.

For management quality, this distinction is critical:

execution improved; accounting noise fluctuated.

2. Capital Discipline: Returns, Cash, and Reinvestment

2.1 Returns on capital

Return on Invested Capital (ROIC) provides the clearest measure of disciplined stewardship.

Across the past decade:

ROIC climbed from low single digits during the capacity-building years

into the low-to-mid teens as manufacturing scale and brand depth increased

peaking in the mid-20% range during 2022–2023

and normalising around ~17% in the latest reported 12 months[^ ROIC trend based on EBIT–Invested Capital series in accompanying chart (2015–LTM)]

Even after absorbing capex for Vietnam’s new freeze-dried coffee facility, ROIC remains well above the cost of capital—confirmation of rational and effective reinvestment.

2.2 Balance sheet strength and payout discipline

Food Empire maintains a conservative financial posture:

Net cash gearing:–28.8% (FY2024)

(US$130.9m cash vs US$45.7m debt)[^ KGI Securities — Food Empire FY24 Financial Results (17 Mar 2025), including cash, debt, and net gearing.]

This balance sheet enables:

a multi-year US$80m investment in Vietnam manufacturing capacity[^ Asia Food & Beverage — Vietnam freeze-dried coffee plant investment announcement.][^ The Business Times — coverage of Vietnam facility and investment timeline.]

continued salesforce and brand expansion in Southeast Asia

low payout ratios that preserve capital for high-return projects

The business behaves like a disciplined owner–operator: conservative leverage, measured expansion, and reinvestment where returns are highest.

3. Strategic Adaptability: The Vietnam & SEA Pivot

If discipline shows up in margins and ROIC, adaptability shows up in geographic mix.

Company disclosures and independent research confirm:

Vietnam revenue grew +44.6% YoY in 1Q 2025

Southeast Asia became the Group’s largest regional contributor (~29% of Group sales)[^ KGI Daily Trading Ideas — 1Q25 regional performance (SEA overtaking CIS; Vietnam +44.6% YoY).]

Paired with the US$80m freeze-dried coffee plant (completion ~2028), this demonstrates:

Correct market selection

Capital deployed into rising-return regions

Execution strong enough to validate the pivot early

This is real-time evidence that management can replicate the CIS playbook—localisation + distribution + manufacturing scale—in new markets with better macro tailwinds.

4. Founder–Operator Alignment: Incentives That Match Owners

With over 34% insider ownership, management’s incentives mirror long-term shareholders. This alignment translates into:

consistently conservative leverage

avoidance of empire-building acquisitions

reinvestment into high-return projects rather than short-term EPS boosts

willingness to accept temporary FCF dips when long-term capacity is being built

This is why the company often behaves like a private business inside a public wrapper—focused on durability, not quarterly optics.

Takeaway: Food Empire’s management doesn’t win through theatrics — they win through discipline. Over a decade, they reinforced every load-bearing part of the business: deeper distribution, localized execution, better factories, stronger margins, and a successful pivot to Southeast Asia. They improved results not with big bets, but with thousands of quiet, rational decisions — the kind you only make when you own a meaningful stake yourself. This is leadership that compounds value steadily, protects the downside, and earns the trust of long-term owners.

Final Assessment: Strong

Key Proof:

• Operating margin expansion even during severe commodity inflation:

— 13.3% (2024) → 14.8% (LTM 2025)

• ROIC improved over a decade from low single digits → mid-20s peak → ~17% normalized (still well above cost of capital).

• Rational capital allocation: investment into Vietnam freeze-dried plant while maintaining profitability.

• Strategic pivot success: Southeast Asia surpassing CIS as largest revenue contributor; Vietnam +44.6%.

• Evidence of disciplined execution: stable cost control, deepened distribution, consistent operating leverage.

Justification:

Food Empire’s leadership embodies quiet, disciplined stewardship rather than dramatic turnarounds. Over ten years, management systematically strengthened every part of the business — expanding into safer, faster-growing markets, building manufacturing depth, lifting margins, and maintaining a fortress balance sheet. The ability to expand operating profitability during a commodity shock reflects operational excellence, while the long-term ROIC trend confirms superior capital allocation. The successful pivot toward Southeast Asia demonstrates strategic clarity, not luck. Founder alignment ensures decisions prioritize durability over optics. This is the behavior of a team that has earned long-term owners’ trust — consistent, rational, and compounding value through disciplined execution.

Pillar 3: Financial Health

Rating: Strong

Food Empire’s 2025 financial profile reflects a company that remains cash-rich, lightly levered, and structurally profitable, even after a deliberate multi-year reinvestment cycle across Asia. The Fiscal.ai charts confirm three things: profitability remains healthy even after normalisation, cash conversion is recovering as working capital stabilises, and liquidity stays well above industry norms — reinforcing a Strong rating under Glavcot’s Financial Health rubric.[^FY2024 Unaudited Condensed Financial Statements][^1H2025 Interim Financial Statements][^1H2025 Press Release]

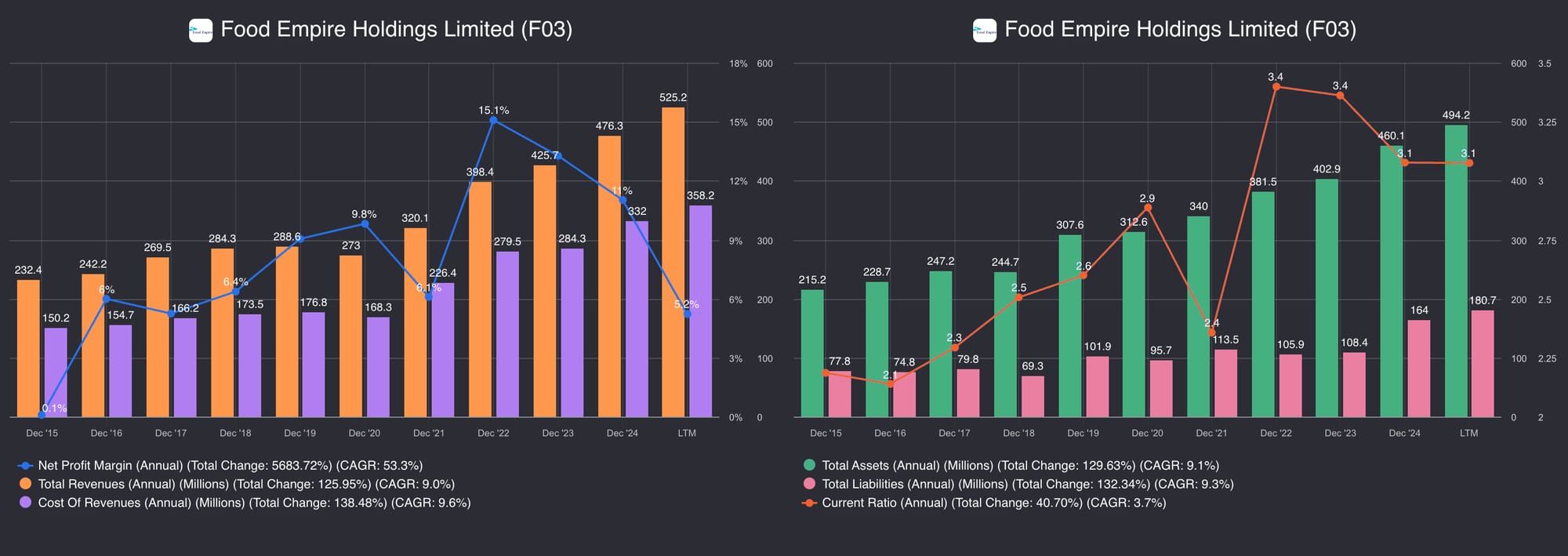

The following chart below shows Food Empire sustaining 3.0×+ liquidity through FY2022–2025. This aligns with official filings where the Group reported current assets of US$333.6m and current liabilities of US$108.5m in 1H2025, producing a 3.1× current ratio.[^1H2025 Interim Financial Statements]

Referring to Chart C — Current Ratio (Annual & LTM):

Liquidity consistently above 3× highlights a structurally conservative balance sheet.

Even after including the debt component of the 2024–2025 Redeemable Exchangeable Notes (REN), Food Empire remains a net-cash operator:

FY2024: US$130.9m cash vs ~US$39m loans → ~US$90m net cash

1H2025: US$135.3m cash vs ~US$54.9m loans → ~US$80m net cash[^FY2024 Unaudited Condensed Financial Statements][^1H2025 Interim Financial Statements]

The balance sheet still resembles a conservative operator funding expansion — not a levered company chasing growth.

Chart C

2. Profitability — Normalisation With Underlying Strength

This aligns with FY2024, where inventory and receivables rose significantly while capex was elevated — a deliberate squeeze, not a structural issue.[^FY2024 Unaudited Condensed Financial Statements]

This is a classic “investment dip” pattern: FCF compresses during expansion, then recovers as assets earn out.

The 1H2025 cash flow rebound confirms the cycle is turning:

Operating Cash Flow: +US$32.4m (vs –US$8.0m in 1H2024)

Capex: easing as projects progress

Cash: up to US$135.3m despite dividends + loan servicing[^1H2025 Interim Financial Statements]

This improvement is fully consistent with a reinvestment cycle that is now transitioning into payoff.

Both FY2024 and 1H2025 statutory profits contain large non-cash items arising from fair-value changes in the Redeemable Exchangeable Notes (REN):

FY2024 recorded a US$2.8m non-cash gain

1H2025 recorded a US$32.6m non-cash loss due to share-price movement[^FY2024 Unaudited Condensed Financial Statements][^1H2025 Press Release]

These swings do not affect margins, cash flow, or operating performance — which is why management also reports normalised profit figures. This accounting volatility is now eliminated after the REN’s reclassification as a “fixed-for-fixed” compound instrument.

Referring back to the Net Profit Margin (Annual & LTM):

The margin charts provide a cleaner view of true economics — unaffected by non-cash REN remeasurements.

Chart D

5. Capital Allocation — Higher Dividends, Same Discipline

The Payout Ratio in Chart D shows a stable trend:

2022: ~30%

2023: ~40%

2024: ~40%

FY2024 included a meaningful special dividend, and in 1H2025 the Board declared the first-ever interim dividend of 3.0 cents, signalling confidence in forward earnings.[^1H2025 Press Release]

The trend tells the story: dividends are rising while reinvestment continues. Management isn't choosing one over the other—they're funding both from organic cash flow.

Despite growing dividends, Food Empire continues to fund:

Vietnam & Kazakhstan manufacturing expansion

Southeast Asia & South Asia brand-building

Working-capital support for high-growth markets[^Segmental Data 1H2025]

This reflects a management team confident enough to raise distributions but still prioritising long-term ROIC.

Final Assessment: Strong

Viewed across the financial data, the conclusion is consistent:

Liquidity remains structurally high

Margins remain healthy and are rising in 2025

Free cash flow has bottomed and is recovering

Dividends are rising without leverage stress

Cash still exceeds borrowings despite major expansion

Food Empire’s financial architecture is resilient, flexible, and conservatively constructed, supporting multi-year growth without compromising protection.

Justification

Food Empire’s 2025 financial footprint shows a company that can absorb heavy working-capital and capex cycles while maintaining high liquidity, strong margins, and the ability to distribute more cash to shareholders. Under Glavcot’s rubric, this combination — high liquidity, mid-teens profitability, stabilising FCF, and prudent capital allocation — easily earns a Strong rating.

Takeaway: Food Empire’s financial strength isn’t about being debt-free; it’s about having optionality. The charts show a company that stays liquid, stays profitable, and stays net-cash — even while investing aggressively for the long run. This optionality lets management compound through volatility.

The Investment Rubric presented here is designed as a structured guide for evaluating business fundamentals using idealized benchmarks across liquidity, profitability, efficiency, and shareholder alignment.

Important caveat: These “ideal ranges” reflect benchmarks commonly associated with mature, brand-driven FMCG companies — businesses characterized by stable margins, habitual consumer demand, and recurring cash flows. While Food Empire now exhibits many of these traits, it is also in the midst of a strategic transition from a legacy CIS-centric exporter to a diversified regional compounder in high-growth Asian markets. As a result, several metrics (such as SG&A leverage, P/FCF, or forward P/E) may temporarily deviate from classical FMCG norms as the company reinvests aggressively into Vietnam, Southeast Asia, and new category expansion.

Therefore, the rubric should be viewed as a framework for perspective rather than a rigid scoring system. The goal is not to force a fast-evolving company into static molds, but to benchmark the directional strength, consistency, and economic discipline underlying its financial performance.

Ultimately, this rubric helps investors think like owners — emphasizing trajectory over snapshots, structural advantages over temporary noise, and long-term capital efficiency over short-term fluctuations. Each business evolves along its own S-curve of reinvestment and maturity; the ranges provided here serve as guideposts for evaluating whether Food Empire is compounding in a durable, repeatable way.

Balance Sheet

Ratio / Metric

Ideal Range (FMCG)

Food Empire Value (LTM)

Assessment & Notes

Current Ratio

1.5 – 3.0

3.4×

✓ PASS — Strong liquidity; well above FMCG norms.

Debt-to-Equity

<0.7

Net Cash

✓ PASS — Conservative capital structure; enhances resilience.

Retained Earnings Growth

Consistent upward trend (>10%)

Multi-year upward trend

✓ PASS — Sustained profitability and reinvestment capacity.

Treasury Stock / Buybacks

Stable or increasing

Active buyback program (S$25.2M / 2021–2024; 3.7M shares by Dec 2024)

~ Moderate — Primarily dividend-based; acceptable for net-cash FMCG.

Valuation Metrics

Ratio / Metric

Ideal Range (FMCG)

Food Empire Value (2025)

Assessment & Notes

P/E Ratio (Trailing 12M)

<18–20×

~36.9× (GuruFocus)

✗ FAIL — Well above FMCG norms; reflects premium expectations.

P/E Ratio (Other sources)

—

~39.3× (SimplyWall St)

— Confirms high trailing valuation vs peers (~13.8×).

Forward P/E (2025 / 2026)

<18–20×

20.6× (2025F) / 15.5× (2026F)

~ Improving — Premium compresses if earnings expand in Asia.

Price-to-Free-Cash-Flow (P/FCF)

<18×

~29× (StockAnalysis)

✗ FAIL — High relative to cash generation.

EV/Sales

<2×

1.70× (2025F) / 1.51× (2026F)

✓ PASS — Acceptable for a growing FMCG brand portfolio.

Acquirer’s Multiple (EV/Operating Earnings)

<10× (value) or 10–14× (quality FMCG)

EV/EBITDA ~11.7×

~ Borderline — Within quality FMCG band.

Dividend Yield Forecast

2–4%

3.9% (2025F) / 4.2% (2026F)

✓ PASS — Attractive payout for a net-cash compounding business.

Takeaway: Food Empire trades at a premium to traditional consumer staples — expensive by historical standards. But the market appears to be pricing in a structural shift: the company is transitioning from a Russia-weighted exporter to a diversified Asian growth story, while maintaining strong returns on capital. Forward valuations moderate quickly, suggesting the current premium reflects timing rather than overvaluation. Not a "deep value" entry, but the valuation looks justified if management delivers on its Asia expansion thesis. In short: expensive on trailing metrics, reasonable on forward economics.

Capital Allocation, Positioning & Risks

1. Capital Allocation Quality

Food Empire has evolved from a low-return operator into a high-return, self-funding growth engine. ROIC rose from 1.6% in 2015 to a 2023 peak of 25.8%, normalizing to 17.1% LTM. ROE similarly reached 19.2% in 2023.

This shift enabled an aggressive reinvestment phase fully funded by internal cash generation:

FCF Margin compressed from 15.1% (2022) to 0.2% (2024) — driven by deliberate reinvestment, not operational weakness

Cash from Operations remained strong at $50.6M in 2023

Major CapEx commitments: US$80M Vietnam freeze-dried plant (target 2028) and US$37M India expansion (target 2027)

Net gearing healthy at (28.8%) in FY2024

Dividend payout ratio steady at 30–40%

Together, these indicate disciplined capital allocation: high returns, self-funded growth, and balance sheet strength.

2. Market Structure & Competitive Positioning

Food Empire’s market strength is anchored by brand leadership in core markets, vertical integration, and a superior balance sheet.

The company is shifting from its legacy Eastern Europe/CIS base — where MacCoffee remains a market leader [^AR2024-MacCoffee] — toward emerging Asian markets. In 1Q 2025, Southeast Asia became the largest revenue contributor at 29.2%, driven by 44.6% YoY Vietnam growth [^KGI-2025Q1].

Two pillars define its moat:

Brand Power

Sustained LTM Operating Margin of 14.8% (vs. 16.7% peak in 2023) reflects durable pricing power and loyalty.

Financial Strength

A persistent net cash position enables self-funded expansion and cushions volatility, unlike peers carrying heavy leverage — e.g., Japfa at 80.1% debt-to-equity [^SimplyWallSt-Japfa].

3. Notable Trends & Forward-looking Risks

Notable Trends

Asia-led growth: 1Q 2025 confirms Vietnam and India as primary engines [^KGI-2025Q1]

Vertical integration: Over US$117M committed to Vietnam + India [^AFB-Capex]

Margin normalization: ROIC and operating margins have normalized from 2023 peaks to sustainable levels

Forward-Looking Risks

Execution Risk

The largest investment cycle in company history brings risks of delays, cost inflation, and demand mis-forecasting .

Geopolitical & FX Risk

Russia/CIS remains volatile: FY2024 Russia sales grew 7.3% local currency, but declined 1.1% in USD due to FX pressures [^KGI-FY24].

Commodity Input Risk

Exposure to global coffee prices remains high; Operating Margin fell from 16.7% → 11.0% in 2024 during the commodity spike .

Conclusion: The Owner's Perspective

Food Empire today is a rare blend of boring staple and quiet compounder. What began as a low-margin CIS exporter has evolved into a higher-return FMCG platform with localized brands, disciplined vertical integration, and a deliberate pivot toward faster-growing Asian markets. Pillar I and II showed this moat is earned through execution — not inherited through category advantages — and that founder-led management has mostly reinvested rising returns into deeper market penetration and capacity upgrades rather than financial engineering.

Pillar III reveals a business that feels unusually resilient for an emerging-market consumer name: net-cash balance sheet, conservative liquidity, and profitability that normalized after commodity spikes yet remains robust for mass-market beverages. The current investment cycle — Vietnam's freeze-dried plant, India's scale-up, heavier working capital — reflects confidence in durable demand, funded internally without leverage.

The risks are real but contained. Heavy regional exposure, currency volatility, regulatory uncertainties, and the operational challenge of scaling two major markets simultaneously don't erase the moat — they shape the pace and consistency of future returns.

Valuation reflects this progress. Analyst consensus views Food Empire as a quality compounder with a long reinvestment runway and improving capital efficiency. The market isn't assuming frictionless success — execution risks around Asia expansion and commodity cost management remain embedded in current sentiment — but expectations are constructive for a business that has demonstrated discipline over speculation.[^Glavcot Insights does not offer buy or sell signals. Our goal is to provide the Clarity (understanding the business mechanics), Perspective (seeing the trends and risks), and analytical Framework (the 3-Pillar and Rubric analysis) needed for you to build your own Confidence. The final decision—whether the current market price offers a sufficient Margin of Safety for the risks involved—rests, as always, with the individual investor acting as a thoughtful owner.][^ Disclosure: As of the date of publication, the author holds a long position in the following securities mentioned: Food Empire Holdings Ltd. (F03). The author has no plans to initiate or alter a position in any of the securities mentioned within 72 hours of publication.]

Glavcot Take: The proof is in the compounding. Over the past decade, Food Empire delivered a 24.4% annualized return, significantly outpacing gold's ~12–14% over the same period.[^ Food Empire 10-year CAGR of 24.4% from Smart Investor (June 2025). Gold 10-year CAGR ~12–14% from Gullak Money and Financial Express estimates.] A mass-market coffee brand selling affordable sachets quietly outperformed one of the world's most popular risk-off assets.

Food Empire is what many "defensive" assets aspire to be: resilient in downturns, relevant in everyday consumption, capable of compounding when conditions improve. If you believe management can continue scaling Asia without losing discipline, this is the sort of business that anchors a portfolio not through promises — but through persistent, observable execution.

Glavcot Scorecard

Food Empire Holdings Ltd. - Q3 2025

Where Clarity Meets Conviction

Glavcot Insights is now live. Join the free tier to get new research, updates, and future analysis directly in your inbox. (Check your spam folder if you don't see the confirmation email)

You might also like

Nov 27

Samudera Shipping Line Ltd. (S56.SI): The shipping company that wins by not losing.

The shipping company that wins by not losing. Samudera Shipping Line compounds through survival—conservative leverage, Indonesian regulatory protection, and the discipline to capture share when overleveraged peers sink.

13 min read

Nov 23

Food Empire Holdings (F03): Fortresses in a Cup-- How Food Empire Built Its Moat One Market at a Time

Food Empire turns everyday coffee habits into long-term compounding — earning in U.S. dollars, operating debt-free, and quietly diversifying its geopolitical risk by replicating its proven fortress-building playbook from Eastern Europe to high-growth Asia.

12 min read

Nov 23

Grab Holdings Limited (GRAB): Engineering an Economic Flywheel for Southeast Asia

Grab is Southeast Asia's leading "super-app," using its massive ride-hailing and delivery network to build out financial services and business solutions across the region.

8 min read

Nov 23

Grab Holdings (GRAB): The Owner's Analysis

This report synthesizes financial data and strategic analysis to present a consolidated view of Grab Holdings' transformation. The assessment is structured across three core pillars, an investment rubric, and an analysis of forward-looking trends and risks.